The Crude Reality – Understanding the Risks for India

Last Updated On: 18 Mar 2026

5 min read

Whats the Point?

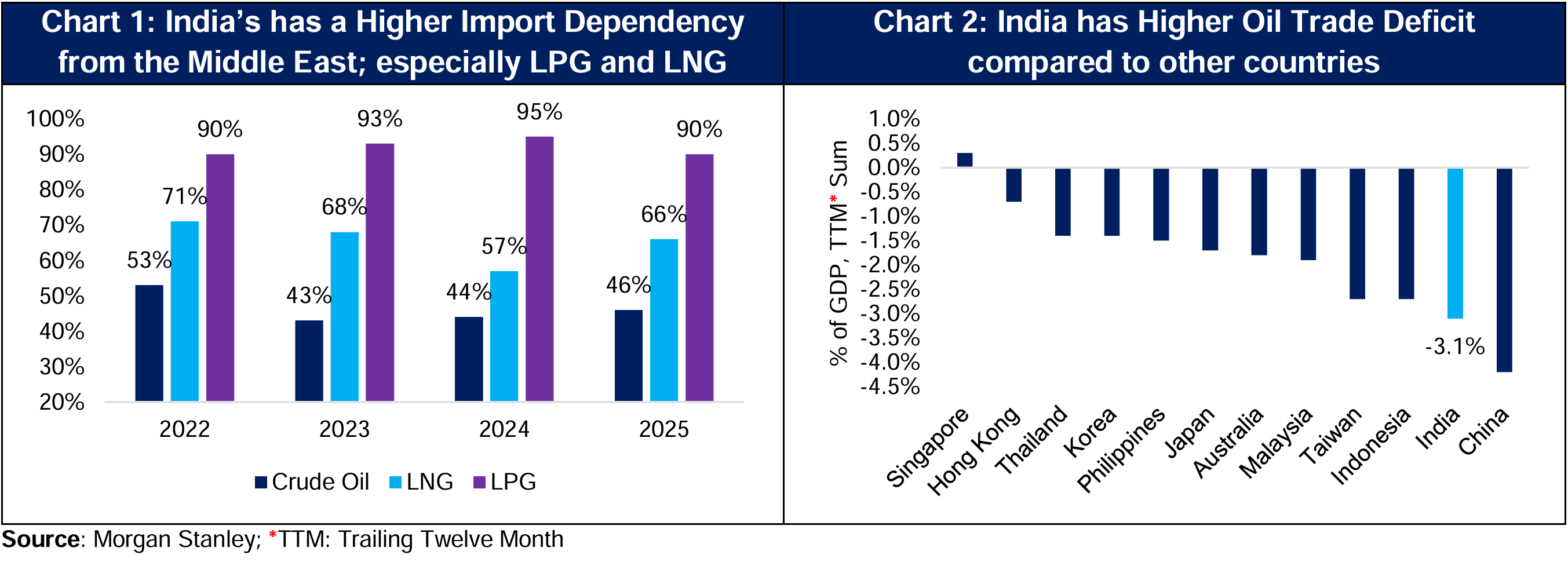

- The recent escalation of conflict between US / Israel and Iran has heightened geopolitical uncertainty and has created supply disruptions of key commodities. Since the start of the conflict on 28-Feb-26, Brent Crude Oil prices have increased by 38.3% to ~US$100 per bbl* (16-Mar-26). India is majorly dependent on imports for its domestic consumption of crude oil (~85%), LPG (~60%) and LNG (~50%), with Middle East being a key contributor.

- India’s reducing crude oil imports and consumption as a share of GDP along with its healthy services exports could help India demonstrate resilience during such turbulent times.

Implications of Rise in Crude Oil and Related Energy Prices

The total crude oil, Liquified Petroleum Gas (LPG) Liquified Natural Gas (LNG) flows through the Strait of Hormuz stood at nearly 20.8 million barrels* per day, 1.5 million barrels per day and 11.4 billion cubic feet per day in H12025 respectively. Such Middle East flashpoints typically generate a risk premium in crude markets, due to concerns around supply disruptions through the Strait of Hormuz, which has remained a key route for ~20% of global oil flows.

- Higher Crude Oil Trade Deficit: With India’s crude oil trade deficit for the last 12 months standing at 3.1% (2024) – higher than other nations – the rise in prices could put a further downward pressure on this metric.

- Higher Current Account Deficit (CAD): Based on a baseline Bent Crude Oil price of US$65 per bbl, the estimated of CAD as a percentage of GDP is 1% in FY27. A US$10 per bbl higher crude oil price and an equivalent change in gas price versus the baseline estimate could add nearly US$20 billion to India’s CAD (0.5% of GDP) between higher oil and gas prices. A secondary impact could be felt via remittances, given that Middle East accounts for 38% of the India’s total remittances.

- Potential Impact on Inflation and Economic Growth: RBI, in its October 2025 Monetary Policy Report, estimated that if crude oil prices rose 10% from its base case, inflation could turn out to be higher by 30 bps and GDP growth may be lower by around 15 bps (assuming full pass-through to domestic product prices).

Key Positives for India amidst the Escalating Conflict

- Falling Imports as a share of GDP a positive, but Length of Disruption a key variable

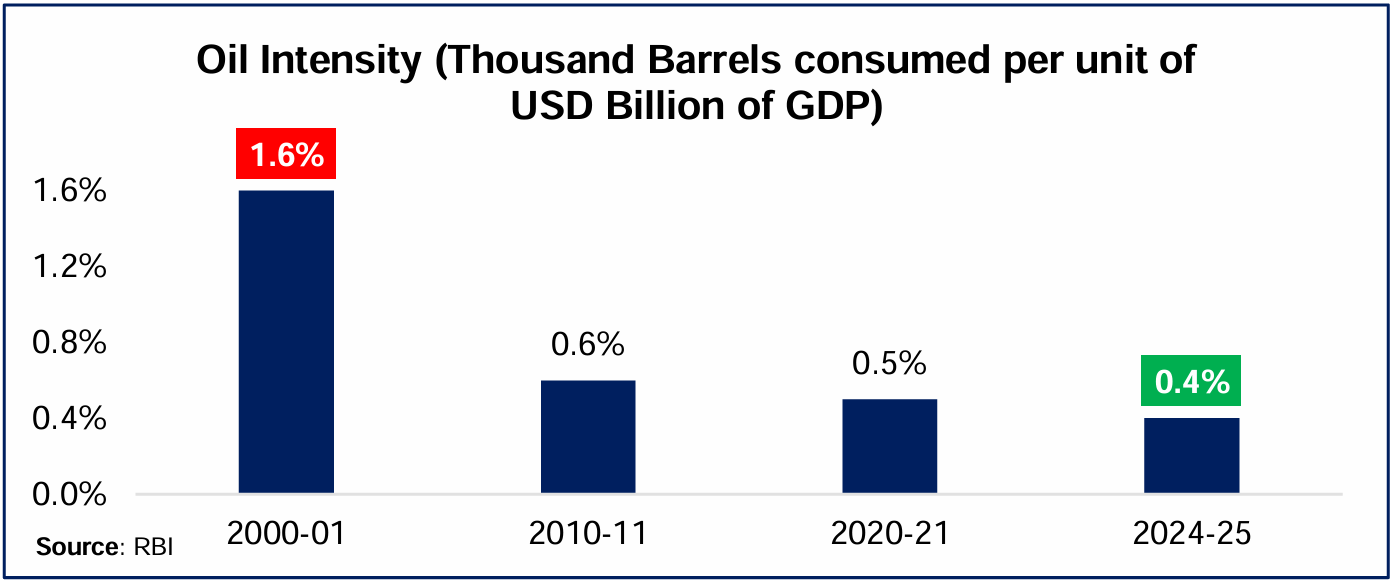

As discussed in a previous edition of Tuesday’s Talking Point titled India’s Resilience Amid Evolving Geopolitical Scenario, India’s crude oil imports as a share of GDP has declined from ~8.5% in 2012 to ~4.8% in 2025, reflecting healthy economic growth, improved energy efficiency and the gradual shift toward cleaner fuels and alternative energy sources. More importantly, the direction of oil prices will depend on duration of the conflict, extent of disruption to physical flows and signals from major producers on spare capacity. Past episodes indicate that price spikes fade if physical flows remain largely uninterrupted and major producers signal spare capacity readiness. Hence, the impact on headline inflation and economic growth could remain more contained than in earlier cycles.

- India’s Services Exports remain healthy

The supply disruptions through the Strait of Hormuz could deepen the impact on the India’s Goods trade deficit. However, India’s economy is largely dependent on Services exports, which remain robust at US$348.4 billion 10MFY26 (~9% YoY higher than 10MFY25).

Conclusion

Despite the above, India’s economy is exposed to crude oil and energy related price fluctuations, given the higher dependency of Indian households, restaurants, hotels, automotive vehicles and other segments on LPG and LNG. However, the risk could be higher if there is a supply constraint of LPG. As of CY25, while 35% of India’s LPG consumption is domestically produced and 65% is imported, nearly 80% of the 35% of the domestic production comes from processed imported crude oil. Hence, the duration of the conflict, extent of disruption to physical flows and signals from major producers on spare capacity remain key. While geopolitical developments could contribute to near-term uncertainties and short-term price corrections, historical experience suggests that domestic oriented economies with strong internal demand tend to demonstrate relative resilience during external shocks.

Sources: RBI, Bloomberg, Morgan Stanley, UBS, CMIE, and other publicly available information.

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.