Inside Stage 2's fast breeder, Thorium sits in a blanket around the plutonium core, which aids the conversion of Thorium into U-233. This U 233 is critical for Stage 3, which remains a long term objective. While a commercially proven design is still years away, the math is compelling: The Uranium used in a Stage 1 reactor, when passed through the breeder cycle, can yield between 60 and 130 times more energy in Stage 3.

India Steps into Stage 2 of its Nuclear Power Programme – A Defining Moment for Energy Security

Last Updated On: 21 Apr 2026

5 min read

Whats the Point?

- On April 06, 2026, India's Prototype Fast Breeder Reactor (PFBR) at Kalpakkam (Tamil Nadu) attained first criticality – self-sustaining nature of the nuclear chain reaction – formally ushering India into Stage 2 of its 3-stage Nuclear Power Programme. Stage 2 is the crucial bridge that unlocks India's vast Thorium reserves, multiplying the energy extractable from the same fuel base many times over.

- Crossing into Stage 2 strengthens energy security through lower import dependence, round-the-clock clean power, and dramatically higher fuel efficiency. Scaling to the 100 GW by 2047 target now hinges on a sharp step up in build rate, backed by enabling policy and legislative reforms.

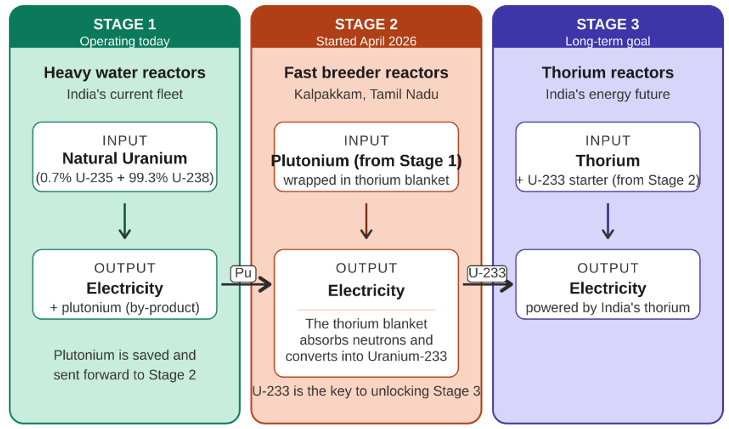

The Three Stages, Simply Explained

Currently, India does not have enough Uranium to power its economy for long, but it has roughly 25% of the world reserves of Thorium – an atomic mineral found along India’s southern coast. However, Thorium cannot be used as reactor fuel on its own. At first, it has to be converted inside a reactor into a usable form of Uranium called the Uranium 233 (233rd Isotope of Uranium / U-233). This 3-stage programme is essentially a production line to generate electricity at every step along the way.

| Stage 1: Pressurized Heavy Water Reactors (PWHRs) | Stage 2: Fast Breeder Reactors (FBRs) | Stage 3: Thorium Reactors |

|---|---|---|

| These are the reactors that make up India’s current nuclear fleet. They burn Natural Uranium to produce electricity, and as a by product, they also create a small amount of Plutonium, which is recovered and saved for the next stage. | This is the stage India just entered at Kalpakkam. Plutonium from Stage 1 is used as fuel. The FBRs are unique because that the Plutonium core is surrounded by a blanket of Thorium. As the FBR runs, it generates electricity, and neutrons from the chain reaction are absorbed by the Thorium blanket, converting it into U 233. In other words, a breeder reactor produces more fuel than it consumes. This is the crucial link that unlocks India’s Thorium reserves. | Using the U-233 bred in Stage 2 as the starter fuel and Thorium as the main feed, Thorium reactors will eventually anchor India’s long-term energy independence. |

Source: Department of Atomic Energy, Press Information Bureau (April 2026)

Thorium – “Th”e Critical Element for Stage 3

Source: Department of Atomic Energy, PIB

Entering Stage 2 implies India could increasingly become Energy Secure

India currently has about 8.78 Giga Watt (GW) of installed nuclear capacity, as of February 2026, across 24 operational reactors, contributing 3.79% of India’s electricity generation. The Government’s stated targets, reaffirmed in the Union Budget 2025-26 and the Nuclear Energy Mission, are 22.5 GW by 2032 and 100 GW by 2047. NITI Aayog’s Energy Security Scenarios project that by 2047, over 80% of installed electricity capacity and nearly two thirds of generation will need to come from non-fossil sources, against a demand backdrop of crude-steel output rising from 144 MT* in 2024 to 530 MT by 2047, and cement production from 426 MT to 910 MT during the same period.

Against that demand curve, crossing into Stage 2 delivers the following 3 structural benefits:

- Input Self-Reliance: India has imported over 5,972 tonnes of Uranium between 2020 and 2024, primarily from Uzbekistan and Canada. Hence, a working Breeder-Thorium chain progressively reduces that dependency.

- Round-the-Clock Clean Power: Indian PHWRs can be refuelled while running, allowing continuous operation for over 2 years at a stretch. This makes nuclear a natural complement to solar and wind, providing steady, always-on power to balance their intermittency as renewables scale. On a full lifecycle basis, CO2 emissions from nuclear are comparable to hydro and wind.

- Fuel-Efficiency Multiplier: The same Uranium atoms are worked harder through multiple cycles, dramatically stretching domestic reserves.

The Road Ahead – From 8.78 GW to 100 GW by 2047

As per the Central Electricity Authority's roadmap ("Target of 100 GW Nuclear Capacity by 2047", June 2025), India must commission 3.5-4 GW of nuclear capacity every year – nearly 10x the current build rate. Roughly half is expected from indigenous 700 MWe# PHWRs, with the balance across imported large reactors, Bharat Small Modular Reactors (BSMR-200), BARC's SMR-55, and BHAVINI's (Bharatiya Nabhikiya Vidyut Nigam Limited) fast-breeder build-out.

India took over 2 decades to build its current PFBR, whereas China delivered a comparable Plutonium Fast Breeder in 5-6 years. Closing this gap demands parallel progress on Uranium mining, reprocessing throughput, heavy engineering capacity, and financing suited to the long tenor nuclear assets. Hence, the recent shifts like the SHANTI** Act (2025), the Union Budget 2025-26's Nuclear Energy Mission, and proposed amendments to the Atomic Energy Act (1962) and the Civil Liability for Nuclear Damage Act (2010) remain critical.

Stage 2 was the programme’s longest engineering bridge. With it crossed – and legal, financial and institutional scaffolding taking shape – nuclear is moving from a small component in India's energy mix to a strategic pillar of its net-zero-by-2070 pathway.

Sources: Press Information Bureau, Department of Atomic Energy, UN Comtrade Database, Centre for Monitoring Indian Economy, and other publicly available information. [*MT: Million Tonnes, #MWe: Mega Watt electric **SHANTI: Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India]

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian and Global economy, financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.