(L)Igniting India’s Energy Independence!

Last Updated On: 21 May 2026

5 min read

What’s the Point?

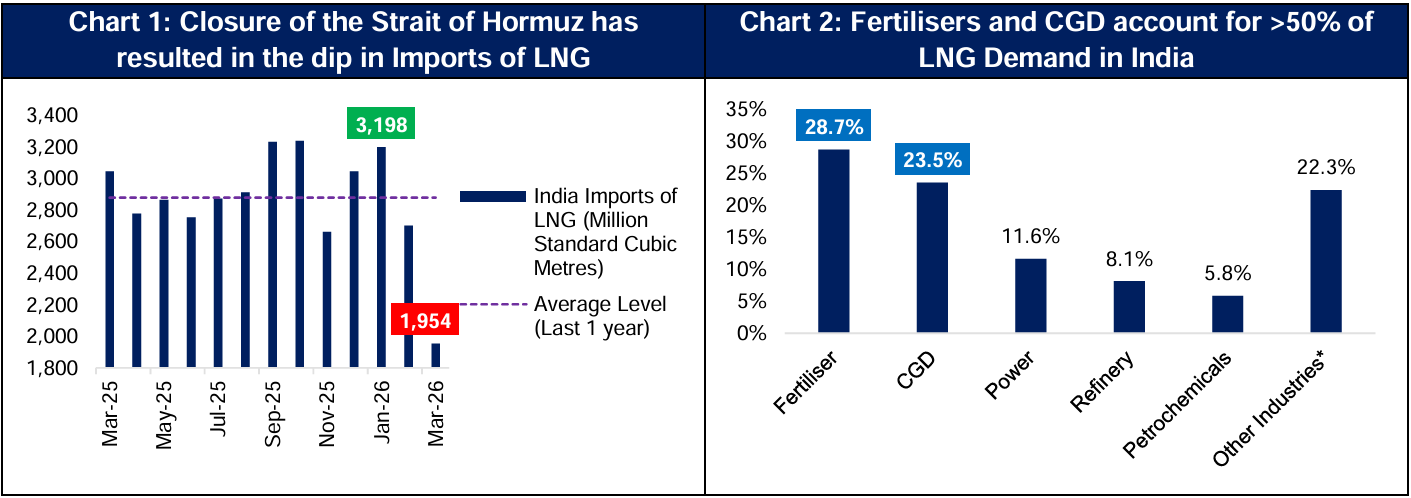

- Liquified Natural Gas (LNG) imports have accounted for ~50% of India’s domestic Natural Gas consumption as of February 2026, signalling to the criticality of this commodity. Historically, India has had a higher import dependency – especially from the Middle East – for its LNG consumption. However, challenges around its availability have emerged since the start of the US/Israel-Iran conflict and the closure of the Strait of Hormuz.

- With India being the world’s fourth-largest LNG importer, there is a need to manage both the demand and the routing sides of India’s gas-import problem. Hence, the Government has decided to take 2 distinct, but complementary measures: 1) a ₹37,500 crore (announced in May-26) Cabinet-approved Coal/Lignite Gasification Scheme to substitute imported gas-derived products at source, and 2) a proposed ₹40,000 crore deep-sea Oman Gujarat pipeline – the Middle East-India Deepwater Pipeline (MEIDP) – to bypass the Hormuz chokepoint.

End-Uses of Natural Gas – A Cross-Sectoral Workhorse

Natural Gas is commodity that sits at the heart of multiple critical sectors of the Indian economy. While Power, Refineries, Petrochemicals and other industries are major end-users of LNG, the top 2 critical end-users are:

- Fertilisers: This sector is the single largest user of LNG, accounting for 28.7% of total LNG consumption as of FY26 [till Feb-26]. Gas is the feedstock for Urea and Ammonia. India's reassessed indigenous Urea capacity rose to ~28.4 MMTPA in FY24 from 207.54 LMTPA in FY15, supporting record production of 31.4 MMT and 30.7 MMT in FY24 and FY25 respectively. Hence, any supply or price disruption therefore flows directly into the Urea subsidy bill and food-security calculus.

- City Gas Distribution (CGD): This sector accounts for 23.5% of total LNG consumption as of FY26 [till Feb 26]. As per Ministry of Petroleum & Natural Gas (MoPNG) Year-End Review (2025), CGD coverage expanded to 307 geographical areas. As on September 2025, PNG domestic connections reached about 1.57 crore and CNG stations increased to over 8,400, thereby signalling the significance for Indian households and mobility.

As per World Integrated Trade Solution, in CY24, Qatar accounted for ~40.7% of India’s 27.7 MMT of LNG imports, with cargo transiting the Strait of Hormuz. Adding UAE, Oman and other Gulf suppliers take the Middle East share to 57.3% of the LNG basket. Given India’s aggregate import bill for substitutable hydrocarbon products (LNG, Urea, Ammonia, Methanol, Ammonium Nitrate, Dimethyl Ether and Coking Coal) stood at ₹2.77 lakh crore in FY25, and domestic production currently meets only ~50% of demand, reducing this structural dependence is critical.

Source: Bloomberg, PPAC, Emkay Global; Other Industries include ceramics, glass, steel/sponge iron, tea, food processing and a long tail of MSMEs

Measures by the Indian Government to increase Energy Security

1) Gasification of Coal – Utilizing India’s Large Reserves

India holds nearly 400.7 billion tonnes of coal reserves – among the largest globally – with coal accounting for ~55% of the energy mix and ~74% of electricity as of April 2025. On May 13, 2026, the Union Cabinet, chaired by the Hon'ble Prime Minister, approved the Scheme for Promotion of Surface Coal/Lignite Gasification Projects to accelerate utilisation of these reserves. Gasification converts coal/lignite into synthesis gas ("syngas") – a versatile feedstock for fuels and chemicals – allowing India to substitute high-value imports of LNG, Urea, Ammonia and Methanol, while insulating itself from global supply disruptions and price volatility.

With a financial outlay of ₹37,500 crore, this Scheme builds on the National Coal Gasification Mission (2021) and the ₹8,500 crore Gasification Scheme of January 2024. This advances the national target of gasification of 100 MT of coal by 2030 and strengthens energy security. Some of the key parameters of this Scheme are as follows:

- Incentive: Up to 20% of plant & machinery cost, disbursed in four milestone-linked instalments

- Caps: ₹5,000 crore per project; ₹9,000 crore per product (except Substitute Natural Gas and urea); ₹12,000 crore per entity-group across all projects

- Expected Impact: ₹2.5-3.0 lakh crore investment across ~25 projects; ~50,000 direct and indirect jobs in coal bearing regions; ₹6,300 crore annual Government revenue from coal/lignite utilisation, plus downstream GST and other levies

- Coal Linkage: Tenure extended to 30 years under the Non-Regulated Sector sub-sector for syngas production

2) ₹40,000 crore Middle East-India Deepwater Pipeline

The MEIDP is a ~2,000 km deep-sea pipeline from Oman to the Gujarat coast via the Arabian Sea – bypassing the Strait of Hormuz – with a designed throughput of ~31 MMSCMD over a 20-year term. The MoPNG is currently preparing a detailed feasibility study, with GAIL, Engineers India Ltd. and Indian Oil anchoring the Design For Reliability (DFR). A positive DFR will initiate formal talks with Oman on gas supply, financing and execution.

Conclusion: India's LNG import dependency on the Middle East remains a near-term vulnerability, and the gasification and MEIDP projects could take time to shift the import mix materially. However, this dual-pronged approach – substituting demand at source and de-risking routing via a Hormuz-bypass pipeline – could be structurally sound response to a structural problem. At a broader level, while geopolitical flux might drive short-term volatility, domestic-oriented economies with strong internal demand have historically shown resilience through external shocks.

Sources: PPAC, WITS, PIB, Bloomberg, Emkay Global, and other publicly available information.

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.