India’s Resilient Macros Amidst Challenging Global Environment

Last Updated On: 12 May 2026

5 min read

What's the Point?

- Amidst challenging global economic conditions, India is structurally on a sound footing with fiscal consolidation on track and both, growth and consumption, holding up well in FY26.

- The revenue base has broadened structurally with GST collections reaching an all-time monthly high in April’26 despite rate rationalisation and corporate tax growing at a healthy pace. Healthy forex reserves and structural support from services exports reinforce India's external resilience.

- Outlook for FY27 depends on global commodity prices and their pass-through to corporate margins, the June’26 RBI MPC meeting, El Niño's progression and its implications for the Kharif season and Q1 FY27 corporate earnings.

The escalation of the Middle East conflict from late February 2026 has added a new dimension to an uncertain global environment. In this context, it is worth taking a closer look at where India's domestic economy stands. India has entered FY27 from a position of reasonable domestic strength. Fiscal consolidation was on track in FY26, the tax base broadened, public investment executed ahead of target and early consumption indicators held firm.

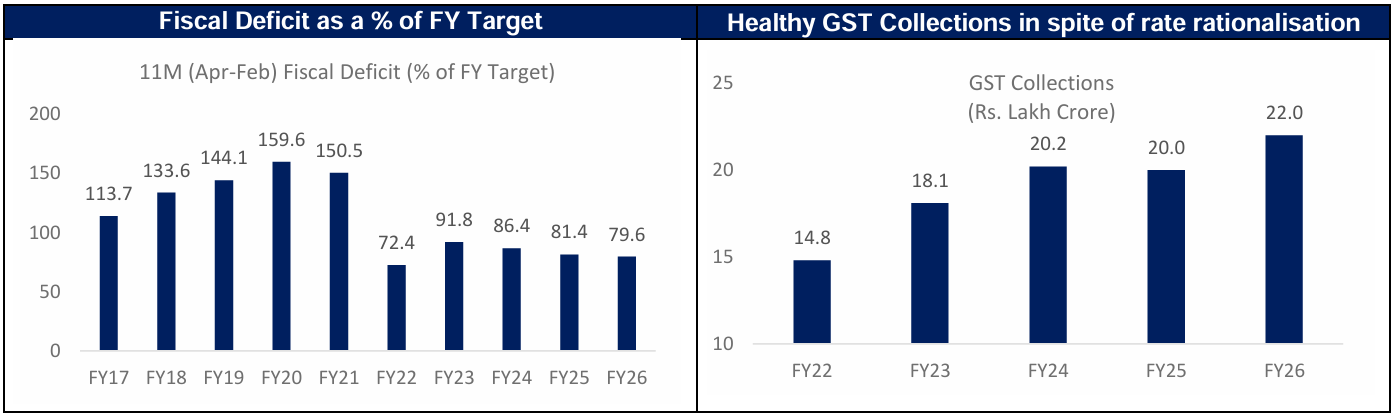

Fiscal Consolidation on Track: Composition as Important as the Number

Fiscal deficit for 11M FY26 (Apr-Feb) stood at 80% of the full-year estimate, lower than last few years. Central Government’s Revenue expenditure grew 1.1% YoY in April-February against capital expenditure growth of 14.5% YoY. Total Public capex (Across Centre, State and Public Sector Enterprises) reached Rs.22.2 trillion in April February FY26, up 8.7% YoY. Public sector enterprises achieved 115.7% of their annual budget target, the highest execution rate in six years.

Tax Revenues: A Structurally Broader Base

Annual GST collections reached approximately Rs.22 trillion in FY26, up 8.3% YoY, with April 2026 recording an all-time monthly high of Rs.2.43 Trillion. Corporate tax collections for April-February grew 12.4% YoY. Sustained GST buoyancy, achieved despite rate rationalization by the GST Council, and strong corporate tax growth, point to a revenue base that is widening through formalisation and earnings growth.

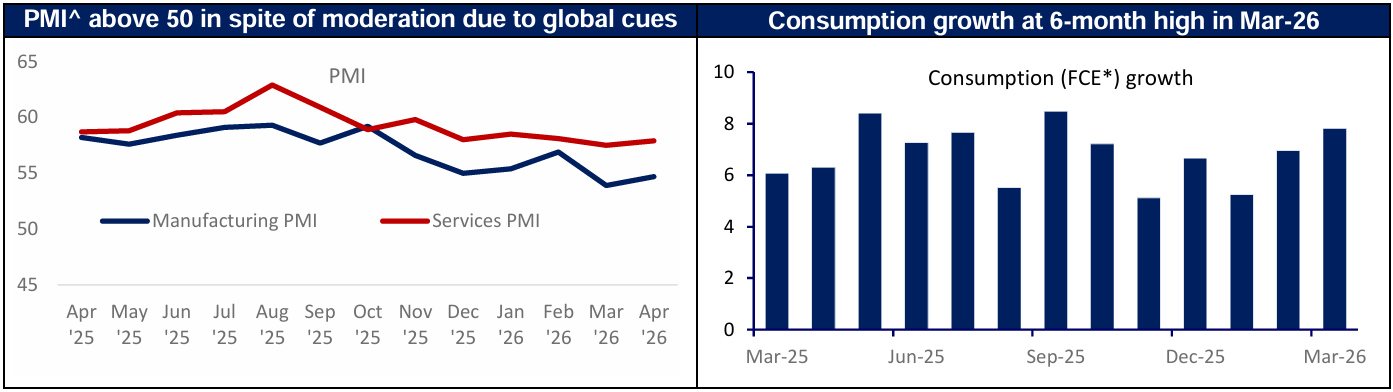

Economic Growth: Firm Through FY26

India's economic output (Real GDP) is estimated to have grown 7.6% YoY# in 4QFY26, stepping down from 7.8% YoY in 3Q but firm in absolute terms. Both PMIs (Manufacturing and Services) remained in expansion territory (above 50) through April’26, though manufacturing momentum has moderated from the elevated readings of mid FY26, reflecting a combination of global demand softness and base effect from a strong H1FY26.

External Sector: Manageable Pressures, Adequate Buffers

India enters the current period of global uncertainty from a position of external strength. Forex reserves stand at $690.7 billion (As of 01-May-26), covering over eleven months of imports, providing a substantial buffer against external shocks. The current account deficit, while requiring careful monitoring given elevated crude oil prices and their impact on the import bill, starts from a low base, an important advantage as global conditions become more challenging. Structural offsets in the form of a growing services export surplus continue to cushion the goods trade deficit.

Consumption: Broad-Based and Holding well

Demand held across income segments through 4QFY26 and into April’26. Auto sales grew 13.2% YoY in 4QFY26 and two-wheeler sales grew 26.4% YoY in 4QFY26, reflecting firm urban and middle-income demand. Tractor sales grew 30.9% YoY in 4QFY26, pointing to resilient rural demand. Personal credit growth sustained above 12% YoY through the quarter, a signal of both household confidence and lender appetite.

Conclusion

The domestic fundamentals that India has carried into FY27 are reasonably healthy. Over the next few months, certain key variables could influence the economy and the markets viz. the trajectory of global commodity prices and their pass-through to domestic corporate margins; the June’26 RBI MPC meeting, which will signal the direction of the monetary policy; El Niño's progression and its bearing on Kharif output and rural incomes; and Q1 FY27 corporate earnings, which will be the first substantive read on how input cost pressures are flowing through to profitability. For long-term investors, periods of externally driven volatility are best viewed through the lens of domestic fundamentals, which remain on a reasonably sound footing. Historically, corrections stemming from global rather than structural domestic factors have provided viable opportunities for investors with a long-term horizon.

Sources: #NSO, CLSA, RBI, GSTN, MoSPI, Avendus Spark, Bloomberg and other publicly available information. ^ Purchasing Managers’ Index, * Final Consumption Expenditure.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.