El Niño is the periodic warming of surface waters in the central and eastern equatorial Pacific Ocean, which weakens the southwest monsoon winds that deliver over 70% of India’s annual rainfall. With almost half of India’s cultivated area still rain

Beyond the Headlines: Putting El Niño in Perspective

Last Updated On: 28 Apr 2026

5 min read

Whats the Point?

- IMD has forecast a below-normal monsoon in 2026 at 92% of Long-Period Average, with El Niño conditions expected to develop through the peak Kharif season

- The forecasted shortfall of 8% remains modest relative to the severe episodes of 2002 and 2009, and the relationship between El Niño and economic outcomes is relatively nuanced

- Reservoir levels well above historical norms, better irrigation coverage, dynamic policy management and a structurally changed (Services-led) economy mean India is well placed to navigate this episode

After two consecutive years of above-normal rainfall, IMD issued its first-stage monsoon forecast for the upcoming monsoon season, projecting cumulative rainfall at 92% of the LPA of 869 mm i.e. classified as ‘below normal.’ El Niño is expected to develop between June and September this year, coinciding with the peak Kharif season. With the event drawing attention across markets and policy circles, we take a closer look at what history and ground realities suggest and why the picture may be more nuanced than the headlines imply.

What is El Niño and Why Does it matter?

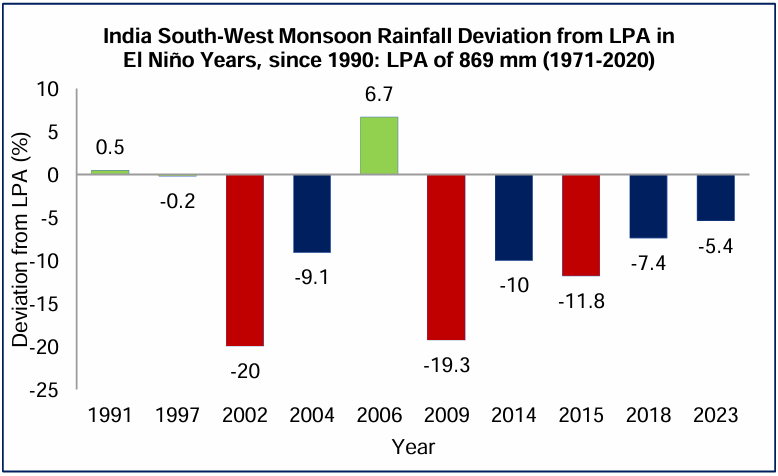

dependent, a weak monsoon directly threatens Kharif crop output and rural incomes. The chart alongside shows monsoon rainfall deviation from LPA across past El Niño episodes, since 1990. Critically, 1991, 1997 and 2006 saw near-normal rainfall despite El Niño and 2023, the most recent episode, recorded a 5.4% deficit yet total food grain production broadly matched the prior year.

Implications for the Indian Economy

Rural Economy: A below-normal monsoon could moderate Kharif output, with rice, pulses and oilseeds most sensitive to rainfall distribution. With ~46% of India’s workforce employed in agriculture, impact on farm income affects rural spending on two-wheelers, tractors and FMCG. What makes 2026 somewhat different from a typical El Niño year is the Middle East overlay: elevated freight costs and fertiliser supply disruptions have already pushed input prices higher, meaning farmers could face a simultaneous hit to both output and margins.

Food Prices: A monsoon-driven supply shortfall tends to reflect in prices of rice, pulses and vegetables, felt by urban and rural households alike. Historically, however, this transmission has been increasingly well-managed.

Buffer stocking, targeted imports and calibrated import duty adjustments have repeatedly arrested food price spikes before they become entrenched, as demonstrated in 2023 when duty cuts on pulses and edible oils helped contain the pass-through despite a below-normal monsoon.

The Policy Tightrope: The RBI has projected FY27 CPI inflation at 4.6%, above its 4% comfort level, with El Niño flagged as a specific upside risk alongside elevated crude oil prices stemming from the ongoing Middle East conflict, leaving the central bank navigating inflation pressure on two fronts simultaneously. That said, India's new CPI series (base year 2024), released in February 2026, reduces food and beverages weight from ~46% to 37%, making headline inflation structurally less sensitive to seasonal agricultural shocks and giving the RBI somewhat more room to look through transient food-driven spikes than it once had.

Why It Need Not Be Alarming

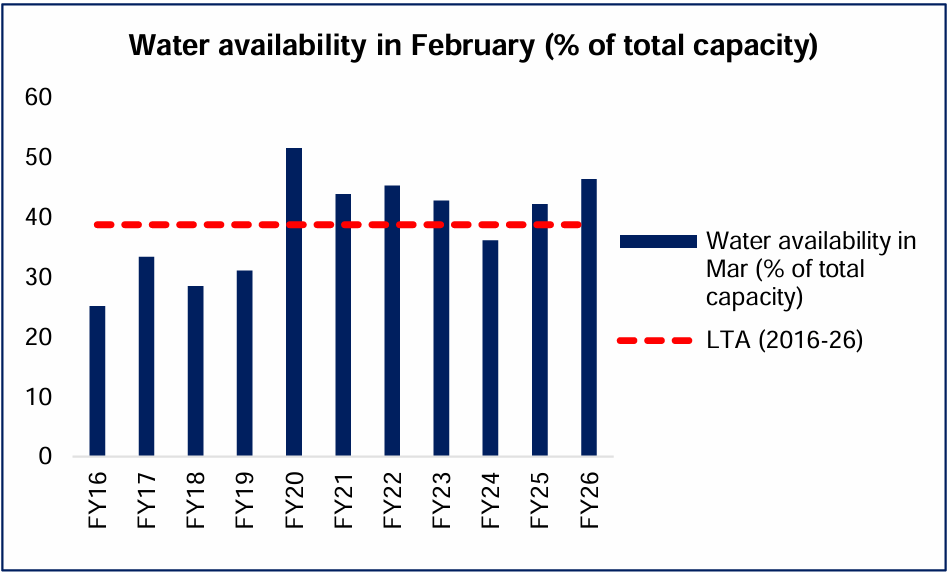

Reservoirs Enter the Season Well-Stocked: India could enter the 2026 monsoon season with reservoir storage running well above historical norms. Water availability across major reservoirs stood at 46.3% of total capacity in March 2026, 8.3 percentage points above the 10-year average of ~38% and the highest level since FY20.

The 2023 Episode Offers a Reassuring Precedent: Despite a ~5 % monsoon deficit in 2023, total food grain production held firm at ~332 million tonnes, broadly matching the prior year (329 million tonnes). CPI inflation, while elevated, remained within manageable bounds and did not derail broader monetary policy or economic momentum. All things said and done, the binary of “El Niño equalling drought” could quite often be overstated.

Irrigation Coverage Has Structurally Improved: Irrigation coverage across Gross Cropped Area has risen from 34% in 1990 to 45% in 2010 and 60% in FY24, reducing the share of purely rain-dependent output. Crops in irrigated districts tend to hold up considerably better even when monsoon distribution is uneven or delayed.

India’s Economy Is Far Less Agri-Dependent: Agriculture’s share in India’s GDP has declined from 50% in 1970 to 35% in 1990 and 14% in 2025. Services now account for 56% of Gross Value Added (GVA) of the Indian economy. The economy’s structural sensitivity to an agrarian weather shock is considerably lower than it once was, and declining further with each passing year.

Conclusion

Historically, seasonal weather risks tend to create more anxiety than lasting economic damage and market outcomes have typically reflected this. Importantly, the forecasted shortfall this year (8%) remains modest relative to the more severe El Niño episodes of 2002 and 2009. Coupled with reservoir levels well above historical norms, record irrigation coverage and more dynamic policy management, spanning buffer stocks, duty adjustments and targeted imports, India is well placed to navigate this episode. The nature of the Indian economy has also changed fundamentally. With services now the dominant component of economy, the economy's sensitivity to an agrarian weather shock is structurally lower than other points in history.

Sources: Bloomberg, RBI, CMIE and other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.