Strai(gh)t to the market – What do high global bond yields mean for Indian fixed income investors?

Last Updated On: 27 May 2026

5 min read

What’s the Point?

- The impact of the oil price spike caused due to the West Asia conflict is becoming visible via higher inflation

- Concerns around the duration of inflationary pressures have led to a rise in bond yields globally

- Despite global uncertainties, the medium-term outlook for Indian fixed income remains optimistic, considering that the markets have priced in most of the negatives

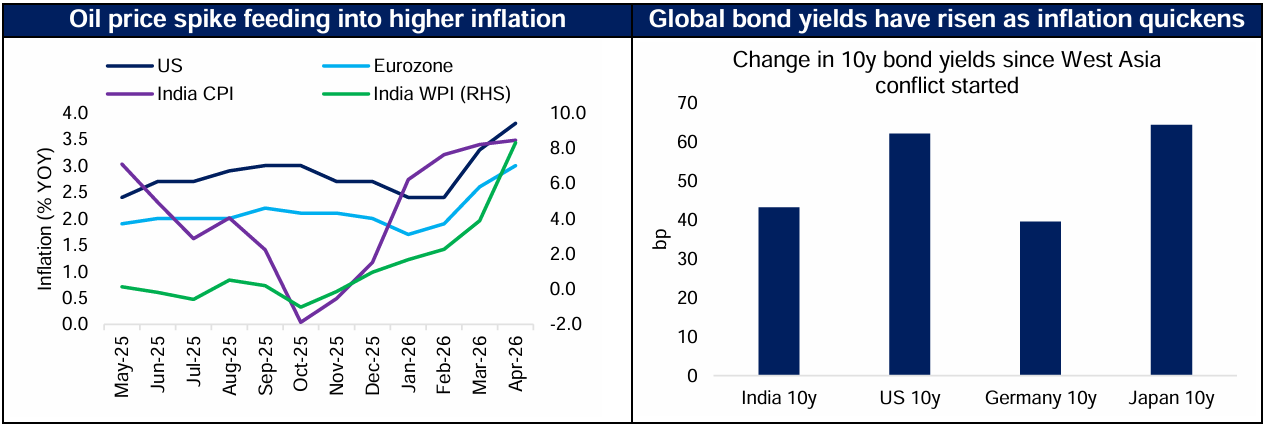

Oil and energy prices have risen considerably since the West Asia conflict started. Along with the rise in energy prices, there have been other disruptions in across other areas of global supply chains as well. Fertiliser is one of the most directly affected commodities: natural gas is essential to its production, and Persian Gulf nations account for one-third of global urea exports and half of global sulphur exports. Before the disruption, the Gulf also accounted for 33% of global helium production — a gas which is used extensively in smartphone and chip manufacturing. The effects of higher energy prices and other supply chain disruptions are filtering through to higher inflation across major economies. Consequently, inflationary fears have caused bond yields to move higher across the globe since the conflict started. These dynamics are visible in the charts below.

Source: Bloomberg, internal calculations. Change in 10y government bond yields considered over the period Feb 27, 2026 to May 22, 2026

Central banks across major economies are expected to hike rates to tame inflation

Before the West Asia conflict started in February 2026, markets were expecting central banks to cut rates in several large economies. However, rate cut expectations have unwound sharply and the market is now expecting central banks to hike rates in several countries. For example, before the conflict started the market expected the US Federal Reserve (Fed) to implement approx. -60bp of rate cuts by Dec 2026 (implied from Overnight Index Swap markets). However, with inflationary pressures rising and lack of clarity as to when the Strait of Hormuz will be fully re-open to global trade, the market now expects the Fed to hike rates by ~25bp by Dec 2026. In India too, pre-conflict expectations of the RBI being on hold for an extended period of time have given way to market expectations of ~100bp of hikes over the next 1 year (implied from Overnight Index Swap markets. Source: Bloomberg, Reuters, internal calculations. Data as of May 22, 2026).

Outlook for Indian fixed income markets

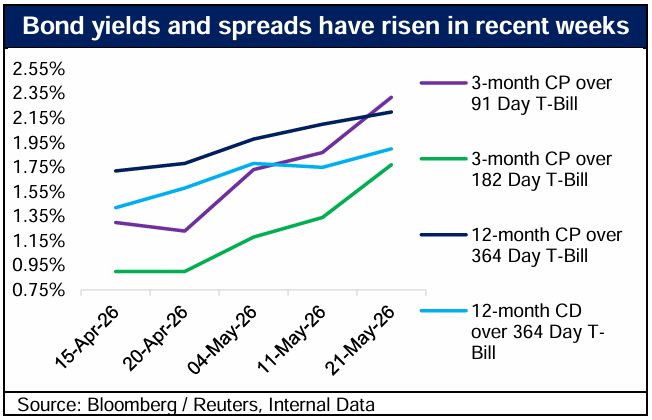

RBI’s decision to keep the policy rate and stance unchanged in its latest monetary policy with inflation forecast for FY27 up only marginally was considered dovish by the markets. RBI governor’s comment on real rates still being high and probability of rates being lower for longer has moderated the rate hike expectations in near future. Also, RBI’s assurance that it will continue to be proactive and pre-emptive in liquidity management and ensure sufficient liquidity also went well from yields perspective

Looking ahead, despite heightened global uncertainty, in our view, the medium-term outlook for Indian fixed income remains optimistic, considering that the markets have priced in most of the negatives. Expectation of a truce between US and Iran and lower oil prices, ample systemic liquidity and balanced supply-demand dynamics for government securities provide meaningful support. With growth risks tilted modestly to the downside and inflation expected to remain broadly well behaved, the likelihood of aggressive rate hikes appears limited. Key risks to monitor include any escalation in conflict or adverse food price movement due to weak monsoon.

Conclusion

The West Asia conflict and the near-closure of the Strait of Hormuz have delivered a significant supply shock to the global economy. Inflationary pressures are becoming increasingly visible, resulting in a sharp repricing of global rate expectations — from cuts to potential hikes across major economies. In India, however, the monetary policy response has been measured and calibrated: the RBI's recent dovish hold and subsequent commentary suggests that aggressive rate hikes remain an unlikely scenario. With markets having already priced in much of the downside, in our view, the medium-term outlook for Indian fixed income appears reasonably constructive — provided the conflict does not escalate further and the monsoon is adequate.

Source: Bloomberg, Reuters, publicly available information

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.