Despite a Hawkish Fed, India's Balance of Payments (BoP) Could Turn a Corner

Last Updated On: 24 Jun 2026

5 min read

What’s the Point?

- The US Federal Reserve held rates but turned hawkish, lifting its 2026 interest rate projection and raising its inflation forecasts as the West Asia oil spike feeds through

- What matters more for India are two other key variables: the price of oil, which has fallen since the West Asia truce, and the monsoon, where a below-normal season is the main risk.

- The RBI and government's June measures target external financing through the Foreign Currency Non-Resident Bank i.e. FCNR(B) and offshore routes, and at a cumulative USD 60–80 Billion of inflows they could turn what could have been a third straight year of balance-of-payments deficit into a small surplus, thereby taking pressure off the rupee.

The US Federal Reserve held rates last week but raised its inflation forecasts in what could be construed as a hawkish hold. For India though this does not necessarily have major implications. Two variables closer to home will do more to shape the macro outcome this year: the price of oil, which has shown signs of softening since the West Asia truce, and the extent and distribution of monsoon. The RBI’s June’26 measures, meanwhile, directly address the external pressure that a higher-for-longer Fed represents. RBI’s slew of measures could help put India’s Balance of Payments on a firmer footing than it has been over the past few years.

US Fed: A Hawkish hold

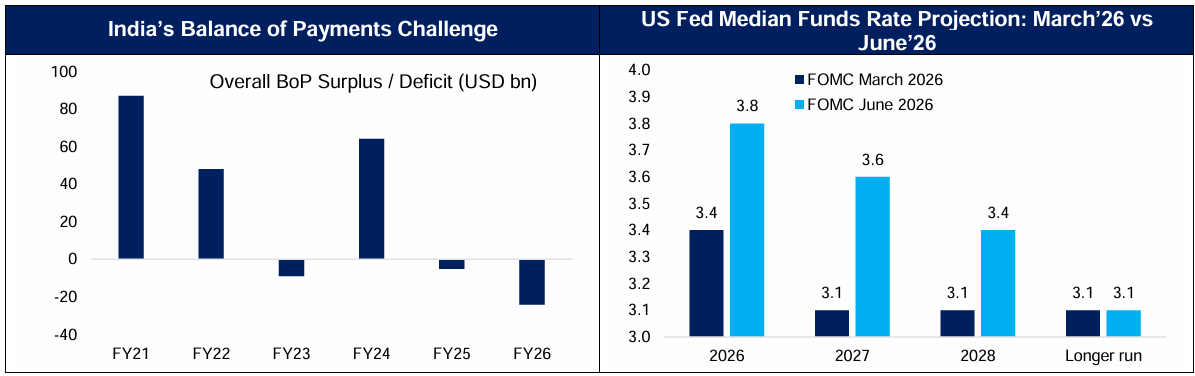

US Federal Reserve held the funds rate at 3.50–3.75% for a fourth straight meeting, but the projections turned hawkish. The median policymaker now sees the rate at 3.8% by December 2026, against 3.4% projected in March’26 meeting, Inflation forecasts rose too, headline PCE inflation for 2026 rose to 3.6% (from 2.7% projected in March’26) and core PCE Inflation to 3.3% (vs 2.7% in March’26).

For India, Oil and the Monsoon matter more

The Fed’s stance is a mild headwind as higher for longer interest rates in US result in lower interest rate differentials between India and US. However, two other variables will do more to shape India’s macro outcome this year.

The first is Oil. India imports most of the Crude it uses, so any surge in price runs straight through to the current account, the rupee and imported inflation. Few variables matter more to India’s external account. The West Asia conflict pushed Brent above USD 100 at its peak, but the truce has since brought it back toward USD 80. Past conflict driven spikes have typically reversed within two to three quarters, with crude correcting 30 to 40 per cent from the peak as supply fears fade. A durable resolution would ease the import bill further.

The second is the Monsoon. Owing to the effect of El-Nino, the 2026 southwest monsoon is likely to come in below normal, around 90–95% of the long-period average, and deficient rainfall could weigh on farm incomes and rural demand. Healthy reservoir levels and large foodgrain buffer stocks provide a cushion for at least one crop season, and strong rural wage growth and non-farm income offer some offset. But a weak monsoon is the domestic risk to watch, mainly through food prices-led inflation and impact on rural demand.

RBI’s Slew of Measures to counter Global Headwinds and address Balance of Payments challenge

While higher for longer US rates create some headwind for flows into India, the domestic response has been proactive. Foreign portfolio outflows and weak net FDI had left India on course for a balance-of-payments deficit for a third year in FY27, with the gap potentially widening to USD 60–70bn. April and May 2026 were among the worst months for outflows in recent memory. The recent measures announced by RBI could provide respite here.

- FCNR(B) and the offshore route: The key measure announced is the RBI bearing the full hedging cost on fresh 3–5 year FCNR(B) deposits until September 30, which can pull in USD 40–60bn.The comparable 2013 window drew USD 34bn. Further, A concessional forex swap for PSU borrowers at a fixed 1.5% makes offshore borrowing competitive with the domestic bond market and can add USD 15–25bn.

- Opening up government bonds: The removal of capital-gains and withholding tax on G-Secs for Overseas Investors, alongside a wider Fully Accessible Route covering all new 15, 30 and 40-year issuances, raises the odds of Bloomberg index inclusion at the next review, with a potential of adding a further USD 10–20bn over 12-18 months.

Together the above measures are expected to bring USD 60–80bn into FY27, enough to move the Balance of Payments from deficit to neutral or a small surplus and take pressure off the rupee. The benefits run wider than the headline BoP number. As dollars arrive, the RBI buys them and releases rupee liquidity, which can lift system liquidity above Rs 4–5tn by September’26. FCNR(B) deposits give banks durable funding at a point where credit growth, near 17% in May’26, has run well ahead of deposits.

Bottom line

The Fed’s hawkish hold is a backdrop for India’s macros and not a key determinant. The outcome rests on other key variables like Oil, which is now showing signs of easing; the Monsoon, which is the risk to watch; and the RBI’s June measures, which directly answer the flow pressure that a higher-for-longer Fed represents. On balance, the external position is set to improve, the balance of payments looks likely to turn from deficit to surplus, and a steadier rupee with ample liquidity gives Indian macros a manageable footing in the near future.

Sources: RBI, CMIE, Bloomberg

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.