Not Just Oil, Fall in Prices of Other Key Input Commodities – A Relief for the Indian Economy!

Last Updated On: 30 Jun 2026

5 min read

What’s the Point?

- Broad-Based Relief beyond Oil: India relies on imports not just for crude oil, but also for Liquified Natural Gas (LNG), Liquified Petroleum Gas (LPG), fertilizers (Urea and DAP*) and certain base metals, leaving multiple sectors exposed to West Asia Conflict-led price swings. A correction in the prices of LNG, Urea and Base metals could lower input costs across energy, agriculture and manufacturing, thereby trimming India’s import bill, easing the fertilizer subsidy burden, and helping soften inflation.

- Inflation and Rates in Focus: With the US–Iran ceasefire largely holding, softer input costs could cool inflation ahead and reduce the likelihood of an RBI repo rate hike, though the truce remains a key watch-point.

Softening in Prices of Key Commodities on account of the West Asia Truce

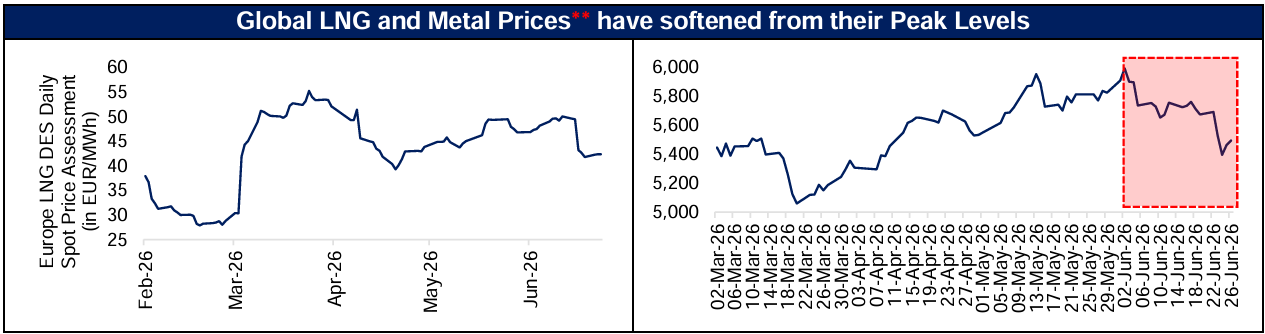

Global Metal Prices have softened, with London Metals Exchange Index (Index based on the closing prices of 6 primary metals: copper, aluminum, lead, tin, zinc and nickel) falling by 8.2% from its peak (Index Level of 5,990.5 on 02-Jun-26 to Index Level of 5,494.1 on 26-Jun-26). Base metals are critical raw materials across construction, power transmission, automobiles, capital goods and manufacturing. With India being a net importer of metals like iron & steel, copper, aluminium, etc., softer metal prices help lower input costs for domestic manufacturers, support margins in metal-intensive sectors, and ease imported input-cost pressures that feed into the Wholesale Price Index (WPI).

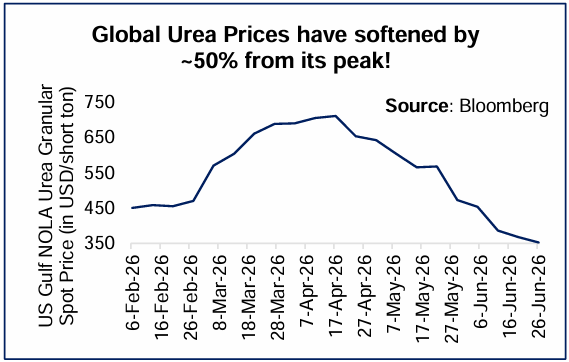

Furthermore, global LNG prices, Brent Crude Oil and global Urea prices have corrected from their peaks by 38.9% (US$118.35 per barrel [/bbl] on 31-Mar-26 to US$72.63/bbl on 29-Jun-26), 23.3% (EUR55.21 per Mega Watt-hour [/MWh] on 25-Mar-26 to EUR42.35/MWh on 24-Jun-26) and 50.4% (US$710/short ton on 17-Apr-26 to 352.5/short ton on 26-Jun-26). This correction comes as major relief as it eases input costs for multiple segments of the economy, thereby reducing India’s import bill, thus lending support to Current Account, and supporting the fiscal health.

Source: Bloomberg; Left Chart: Data as of June 24, 2026, Right Chart: Data as of June 26, 2026; **LMEX Index

Lower Fertilizer Cost – A Relief for India’s Rural Economy

Fertilizers are classified by which nutrient they deliver.

- Urea is a straight nitrogen fertilizer, which supplies only Nitrogen (46%) – the driver of vegetative growth.

- *Di-Ammonium Phosphate (DAP) is a complex / phosphatic fertilizer, which supplies two nutrients: Phosphorus (46%) and a bit of Nitrogen (18%).

LNG is the imported ship-able form of natural gas, which serves as the feedstock for producing hydrogen, which becomes ammonia, which in turn becomes urea.

India – the world's second-largest fertilizer consumer and largest importer of DAP and Urea – imports 25.8% of its fertilizers from the Middle East (2026). To shield farmers from global price volatility and supply disruptions, the Union Budget FY2027 earmarked a net allocation of an estimated ₹1.71 lakh crore to the Department of Fertilizers. But the West Asia conflict's surge in Urea and LNG prices, compounded by tighter supply chains, threatened to double this subsidy bill from its budgeted level to an estimated ₹3.4 lakh crore in FY27. However, the softening of the prices of these commodities would ease pressure on India's fiscal deficit and lend support to the Current Account.

Wholesale Price Index – A Key Inflation Metric that could soften in the upcoming months

Driven by the West Asia Conflict, India’s WPI rose from its pre-conflict average of 0.7% YoY between February 2025 and February 2026 to 9.7% YoY in May 2026. This rise was driven by the following sub-groups:

- Crude Petroleum and Natural Gas (Group – Primary Articles): WPI increased from -8.2% YoY [average between February 2025 to February 2026] to 61.5% YoY in May 2026.

- Mineral Oil (Group – Fuel and Power): The item-level indices of Mineral Oil – LPG, Petrol, Kerosene, Aviation Turbine Fuel, High Speed Diesel, Naphtha, Bitumen, Furnace Oil – saw its respective WPI YoY increase across the board from -4.2% YoY (average between February 2025 and February 2026) to 49.8% YoY in May 2026.

- Basic Metals (Group – Manufactured Products): WPI increased from 0.48% YoY [average between February 2025 to February 2026] to 12.3% YoY in May 2026.

Conclusion: RBI, in its Monetary Policy Review held in June 2026, mentioned that the increase in prices of several inputs such as commercial LPG, industrial raw materials, chemicals, base metals, rubber, and plastic products, among others, could exert upward pressure on CPI inflation in the coming months as firms pass on higher input costs to consumers. Hence, it increased the Consumer Price Index (CPI) inflation projection for FY2027 to 5.1% compared to the projection of 4.6% in the April 2026 Monetary Policy Review. Despite this increase in projection, inflation remains well within the RBI's CPI target of 4% with a tolerance band of +/- 2%.

That said, RBI's June 2026 projection largely reflected the input-price surge seen due to the conflict. On June 17, 2026, US and Iran signed a Memorandum of Understanding to formally end the war, and despite renewed tensions over the weekend, the agreement remains in place. As the conflict-driven price spike fades, a softer inflation print could also lower the likelihood of an RBI repo rate hike. Together, this broad-based easing supports the Current Account, the fiscal position and the inflation outlook, lending India's growth story a firmer footing.

Sources: Bloomberg, CMIE, RBI, PIB, and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.