An Undervalued Rupee- Putting it in Perspective

Last Updated On: 2 Jun 2026

5 min read

What’s the Point?

- Recently, the INR has depreciated more than most Emerging Market peers. This has been driven by a decline in capital flows, rather than weak fundamentals.

- In real trade-weighted terms, the INR is at its most undervalued level since the 2013 Taper Tantrum, indicating the extent of INR’s undervaluation.

- Several catalysts like resolution of West Asia conflict, reduced repatriation by foreign investors owing to weakness in equity markets and a potential rotation of global capital back to India once interest in AI and commodity themes moderates could lead to a recovery in the Rupee.

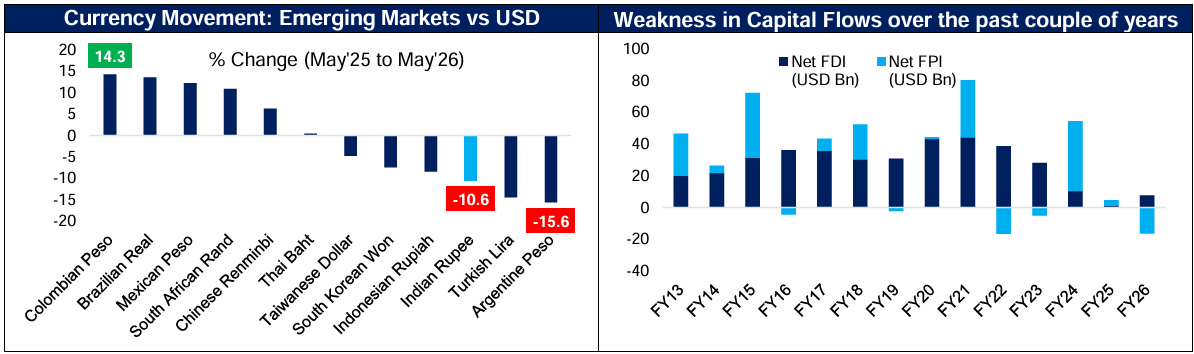

The Indian rupee has depreciated ~11% against the US Dollar since May 2025, which is more than most EM peers and in stark contrast to India's relatively strong macro fundamentals. While some other EM currencies have weakened over the same period, the INR's move stands out in both magnitude and context. The depreciation of Rupee is not a story of weak fundamentals or inflation. It is rather an outcome of weak capital flows, which predated the West Asia conflict and has since been exacerbated by the risk-off sentiment the conflict has triggered across emerging markets. The 6-currency Real Effective Exchange Rate (REER) has fallen to levels last seen during the 2013 Taper Tantrum episode, underscoring the extent to which the rupee is now undervalued in real trade-weighted terms.

Reasons for INR depreciation

- Capital account challenge: Net FDI has collapsed from $44 Billion in FY21 to just $1 Billion in FY25, driven not by weak gross inflows but by a surge in PE/VC repatriation via India's buoyant IPO market. FY26 saw some recovery in net FDI flows although it is still significantly lower compared to history. FPI net flows too have declined with FY26 being the 3rd net negative FY in last 5 years. Net FDI and FPI flows, which together totalled +$80 Billion in FY21, turned negative in FY26 with net outflows of $9 Billion.

- The West Asia war has added cyclical pressure on the current account through three simultaneous channels. India imports ~45% of its energy from the region, exports ~15% of total goods exports and receives ~40% of its annual remittances from these countries. The West Asia conflict, which escalated in February 2026, impacts all 3 fronts simultaneously. While the full impact on the current account will only be visible in Q4 FY26 data and beyond, the potential widening of the Current Account Deficit is manifesting in pressure on INR.

INR Undervaluation and case for recovery

The Real Effective Exchange Rate (REER) measures the value of a currency against a weighted basket of trading partner currencies, adjusted for inflation differentials. Unlike the nominal exchange rate, the REER captures whether a currency is genuinely cheap or expensive in real trade-weighted terms.

With a REER Index reading of ~89.7 (as of 30-Apr-26), the INR is approximately 10% below its 10-year average in real terms. INR’S REER had last dropped below 90 in 2013-14 Taper Tantrum episode. In fact, in Real Terms INR is 3.46 Standard Deviations below its 10-year average i.e. Z-Score of -3.46, which is the most undervalued it has been in recent times. The contrast with the Turkish lira puts the scale of INR’s undervaluation in perspective. Despite a larger nominal depreciation of -14.5% (May’25 to May’26), the Turkish Lira’s REER Z-score is just +0.24 as Turkey's chronic high inflation explains the currency depreciation, leaving its REER broadly close its own historical mean. On the other hand, the INR's depreciation is not explained by inflation. Pressure on INR is primarily on account of capital flow dynamics and geopolitical risk aversion rather than deterioration in India's macro position.

Since 2000, a REER below 90 has been a genuine anomaly, occurring in 46 months out of 316 (Jan’00 to Apr’26). Historically, when this threshold was breached, the subsequent 12-months witnessed recovery for both the currency and Indian equities. In 78% of instances where REER was <90, the INR appreciated over the subsequent 12 months, with a median return of +4.0%. Further, Nifty 50 returns over the subsequent 12 months averaged +37% with positive returns in 91% of instances.

Conclusion

The INR's weakness is a flow problem, not a fundamental one. Several catalysts may drive a meaningful recovery from here. A resolution of the West Asia conflict may ease oil prices, relieve pressure on GCC remittances and restore broader EM risk appetite simultaneously. A correction in Indian equities may paradoxically help the capital account by reducing the attractiveness of the repatriation route that has driven net FDI lower in recent years. For foreign investors, the combination of a corrected market and a deeply undervalued currency creates a dual return opportunity viz. capital appreciation from the underlying asset and currency gains as the INR recovers.

More broadly, the capital flow headwinds India has faced predate the conflict. Global capital has rotated toward AI-themed technology economies and commodity exporters. With commodity prices having surged and several AI-related themes trading at elevated valuations, the relative attractiveness of those destinations may moderate and India, with its diverse economy and a currency at its most undervalued in more than a decade on a REER basis, may stand to benefit from any shift in global investor sentiment.

^9MFY26, Sources: Bloomberg, CLSA, Avendus Spark, CMIE and other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.