Why India Could Appeal to Foreign Investors Once the AI-led Trend Fades

Last Updated On: 15 Jul 2026

5 min read

What’s the Point?

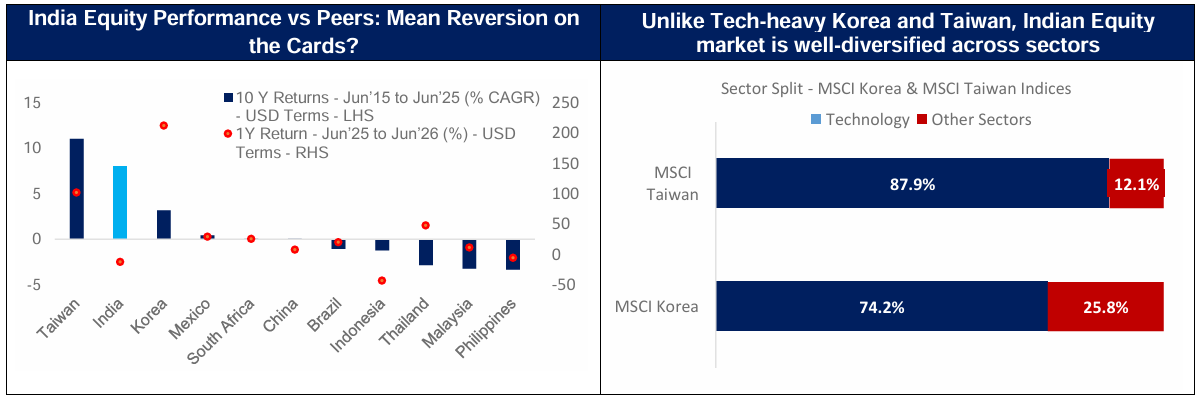

- FPIs have been net sellers of Indian equities over the past few years. After outperforming EMs (Emerging Market) peers on a USD basis over 10 Years (Jun-15 to Jun-25), India has underperformed over the last one year as EM returns became concentrated in markets which are beneficiaries of AI theme, mainly Korea and Taiwan.

- India has low direct exposure to AI revenues and lower sensitivity to US interest rates than Korea and Taiwan. Once the AI-led trend fades, these characteristics support India’s case within EM allocations.

- EM correlation with US equities has risen above that of DM’s (Developed Markets), driven by the recent concentration of AI names in the EM index. A tilt within EM away from Korea and Taiwan towards India could improve diversification versus the US.

Foreign portfolio investors (FPIs) have been net sellers of Indian equities over the past few years. After a decade of outperformance versus EM peers on a USD basis (Jun-15 to Jun-25), Indian equities have underperformed over the last one year, declining roughly 13% in USD terms in 1 Year ended 30-Jun-2026 against a roughly 40% gain for the EM index. This underperformance reflects the composition of EM returns rather than a deterioration in India’s fundamentals. Korea and Taiwan now account for close to half of the EM index by weight, the top five stocks account for over a third, and index returns have been driven by AI-linked names. This has resulted in rising EM Correlation with US Equities, higher than that of DM vs US.

1) AI revenue exposure: India offers a more diversified profile

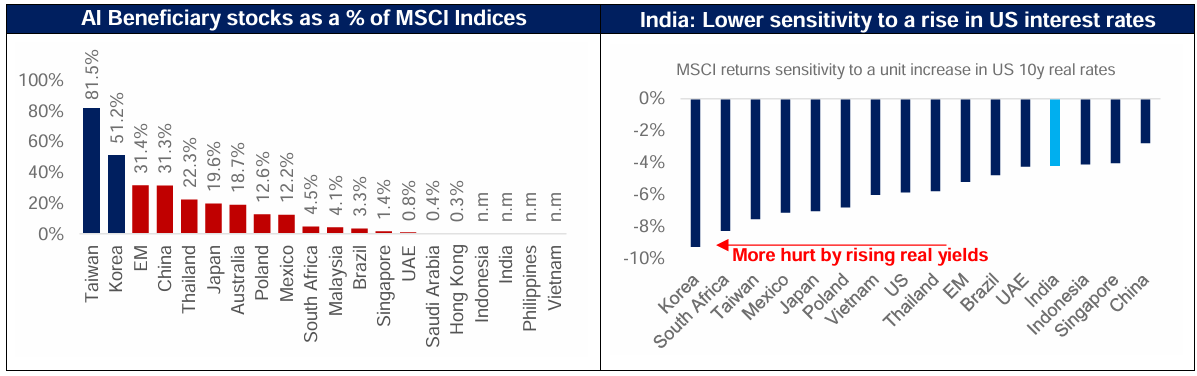

Stocks with revenue linked to AI account for roughly 30% of the EM universe by weight, including ~80% of Taiwan’s index and 50% of Korea’s. The corresponding share for India is negligible. This gap explains most of India’s relative underperformance over the past year. It also means Indian earnings primarily depend on domestic demand spread across wide array of sectors and themes rather than on a single global theme. Interestingly, foreign investors have already started reducing positions in Korea and Taiwan. CYTD (up to 7-Jul-26) they have sold a net $100bn of Korean equities and $30bn of Taiwanese equities, attributed largely to rebalancing and profit-taking in concentrated winners rather than a change of view on those markets. So far, the foreign flows have seen rotation to proxy AI plays like Japan, which has seen Net Inflows of $50bn (CYTD up to 7-Jul-26). However, once the AI-led trend fades, India’s more diversified earnings profile is likely to be of interest to investors reassessing concentrated EM exposure.

2) Lower sensitivity to US interest rates

US rates could stay higher for longer owing to elevated energy prices and sticky inflation expectations. In fact, probability of rate-hike this year stood at 80% (As of 10-Jul-26). Historically, Korea has been among the EM markets most sensitive to rising US real yields, with Taiwan close behind. India’s sensitivity is less than half of Korea’s. In a higher-for-longer rate environment, the markets that led EM returns recently carry greater interest rate risk than India.

3) Rising EM correlation with US equities

For most of the last two decades, EM equities had a lower correlation with US equities than developed markets (ex US). Global portfolios therefore held EM partly as a diversifier away from the US. Over the past year this relationship has inverted. With the largest EM stocks now closely tied to the US AI theme, EM’s correlation with US equities has risen above that of developed markets. For a foreign investor who wants EM exposure without adding to US-linked AI risk, a tilt within EM away from Korea and Taiwan towards India improves diversification, as India’s earnings drivers are domestic and have practically no linkage to global AI capex cycle.

Conclusion

EM leadership has rotated repeatedly over the last twenty years, with the top two index positions changing hands several times. Whenever the current AI-led phase matures, breadth is likely to return to EM allocations. At that point, India which offers foreign investors a domestically driven earnings base, lower sensitivity to US rates and improved portfolio diversification versus US equities, alongside a currency at its most undervalued in real trade-weighted terms since 2013, may present a viable investment opportunity.

Sources: Bloomberg, UBS, other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.