India’s Resilience Amid Evolving Geopolitical Scenario

Last Updated On: 4 Mar 2026

5 min read

What’s the Point?

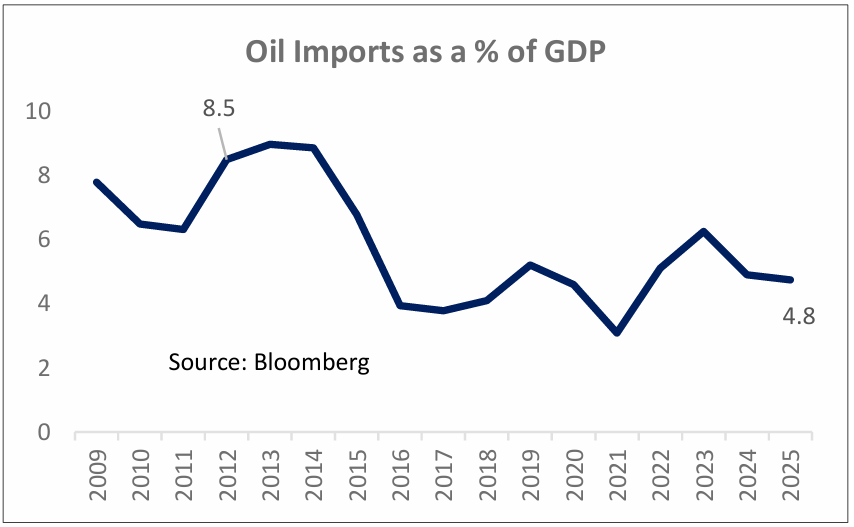

- Reduced Oil intensity: Oil imports as a share of GDP have declined sharply (from ~8.5% in 2012 to ~4.8% in 2025)

- Impact on Inflation: Inflation sensitivity to Crude Oil could be manageable (~20 bps for 10% rise in Crude Oil price)

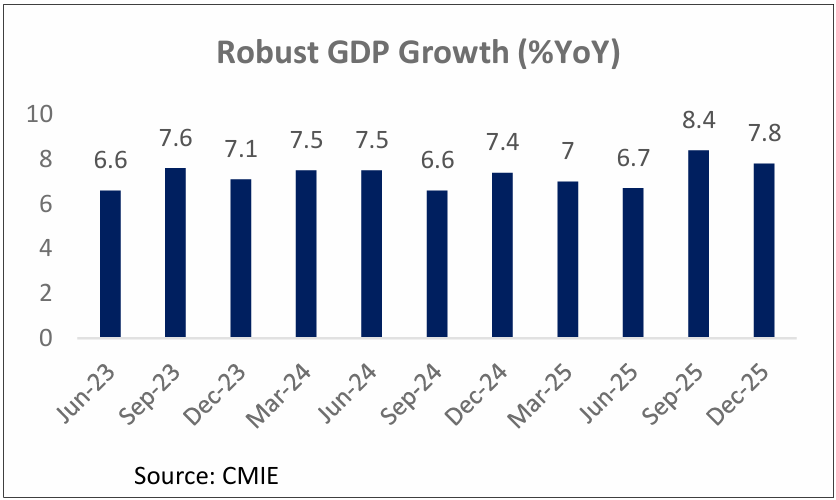

- Strong Fundamentals: Robust GDP growth, strong domestic demand, benign inflation, comfortable forex reserves, prevailing Fiscal discipline and manageable Current Account dynamics enhance resilience.

- Constructive Equity View: Valuations in several segments had already moderated over the past few months. Any further market correction, driven by external events rather than domestic fundamentals, could present accumulation opportunities for long-term investors.

On 28th February 2026, the United States and Israel conducted coordinated strikes on targets inside Iran, prompting retaliatory missile attacks on US assets in the region. This escalation has heightened geopolitical uncertainty in an already sensitive environment. Given the Middle East’s critical role in global energy supply, any further deterioration places immediate focus on crude oil prices and energy security. The broader implication is increased volatility across global financial markets, warranting assessment of potential impact on India.

Impact on Oil Prices

Middle East flashpoints typically generate a risk premium in crude markets, due to concerns around supply disruptions through the Strait of Hormuz, a key route for ~20% of global oil flows. The direction of oil prices will depend on duration of the conflict, extent of disruption to physical flows and signals from major producers on spare capacity. Past episodes indicate that price spikes fade if physical flows remain largely uninterrupted and major producers signal spare capacity readiness.

India’s reduced Oil dependency over the years

Indian Economy resilient to withstand temporary fluctuations

India’s Growth Story Intact: New GDP series reveals

Conclusion

In the near term, geopolitical developments may contribute to episodic volatility, influencing risk appetite and global flows. Such phases are typically sentiment-driven and may lead to short-term price corrections across emerging markets, including India. However, historical experience suggests that domestic-oriented economies with strong internal demand tend to demonstrate relative resilience during external shocks.

Importantly, valuations in several segments had already moderated over the past few months, creating a more balanced risk-reward profile. Any further market correction, if driven by external events rather than domestic fundamentals, could present accumulation opportunities for long-term investors. Over a medium- to long-term horizon, India’s growth trajectory and structural reforms remain key support factors for equities.

Sources: RBI, ^ Jefferies, Bloomberg, CMIE and other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.