Market Review - February 2026

Last Updated On: 16 Mar 2026

5 min read

Macroeconomic Update

Macroeconomic Update Debt Market Update

Debt Market Update Equity Market Update

Equity Market Update

Macroeconomic Update

The ongoing conflict in West Asia poses fresh challenges for World Economy as energy supply chain gets disrupted. So far, growth in US continues to hold up well as suggested by strong readings in both manufacturing and services PMI for February. Labour markets in US, though remain weak as evidenced by low non-farm payroll additions and inch up in unemployment rate. Although the dominant services sector saw a slight underperformance, manufacturing in the EU continued to hold up well. On the other hand, growth in China continues to be weak as domestic consumption demand continues to be dragged down by weak property markets.

Inflation in US and EU remained contained and in line with expectations. On the other hand, CPI inflation in China undershot market expectations due to sharp decline in food prices. While ECB kept its policy rates unchanged in Feb'26, all eyes would be on US Fed's Mar'26 meeting, the first one post the US Supreme Court ruling against Trump's tariffs.

New revamped GDP series:

The Government released the new GDP series with 2022-23 as base year (from 2011-12 earlier). The Government not only changed the base year but also incorporated significant methodological changes in the new series to make GDP measurement more robust and reflective of changes which has taken place in the past decade. The new GDP series confirms continued growth momentum. Q3FY26 real growth came in at a strong 7.8% YoY (as against growth of 8.4% in Q2). Full year FY26 GDP growth is estimated at 7.6% (from 7.4% in old series) implying a growth rate of 7.6% in Q4. GDP growth in Q3 was driven by strong growth in private consumption and investment demand. On supply side, both Manufacturing and Services sector posted strong growth.

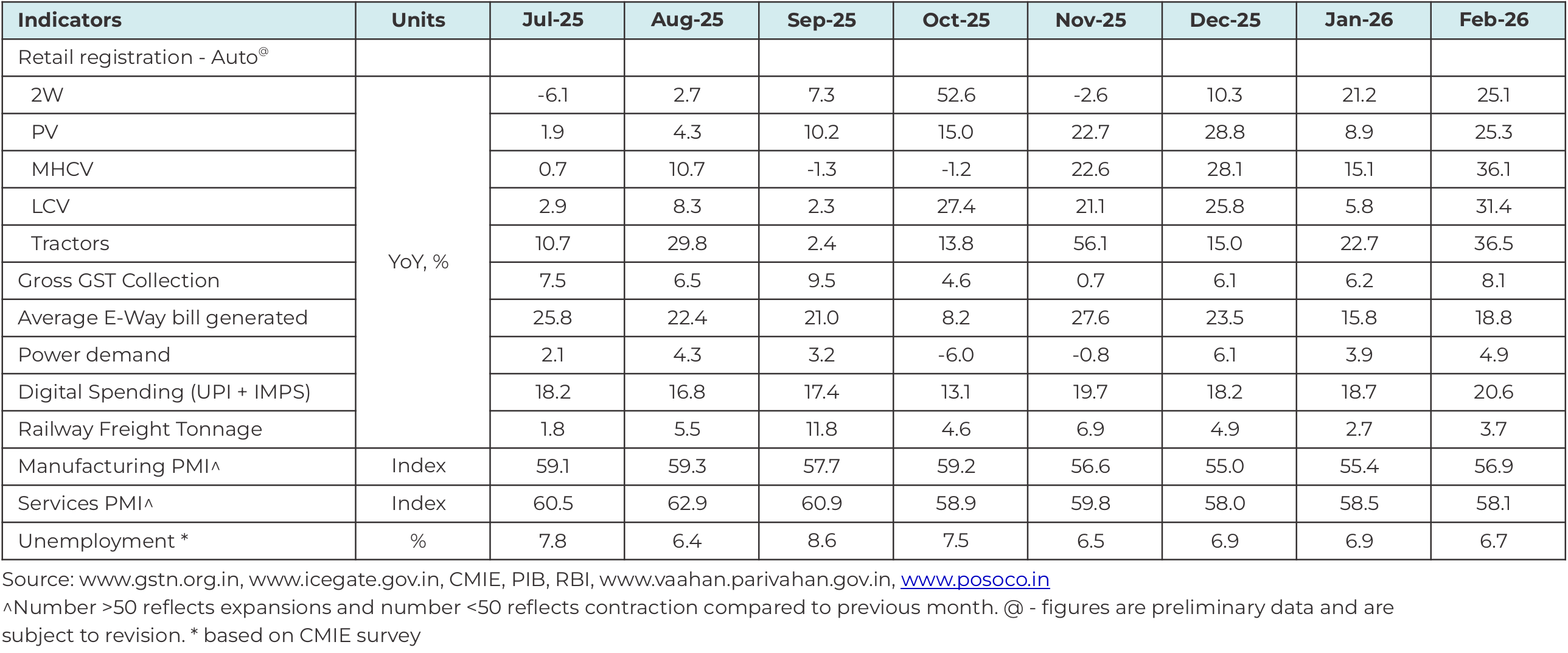

High frequency indicators point towards continued growth momentum: The high frequency indicators for February suggest that growth continues to hold up well. The effect of tax cuts on demand is clearly visible especially on vehicle registrations which continue to post strong growth for fifth month in a row. Power demand too continues to hold up well while GST collections has also picked up and is being sustained.

Going forward, demand is likely to remain healthy on the back of tax cuts, lagged effect of monetary easing and key trade deals especially that with US and EU. Also, prospects of a good rabi harvest and low inflation are likely to keep rural demand buoyant. However, recent geo-political developments and resultant supply chain disruptions could hamper growth in the near term.

Summary and Conclusion:

Global economy faces heightened uncertainty due to flare up in geo-political tensions in west Asia. If the conflict gets elongated, it can have profound implications for the global economy as energy supply chains get disrupted. Growth in the US has held up well and prospects too remain bright on the back of continued investments in AI/tech and supportive fiscal policy. However, labour markets in US are exhibiting signs of weakness. Growth in China is following a two-speed path where domestic consumption and property markets are in a slow lane, but exports and manufacturing are holding up well.

Growth in India has held up well on the back of fiscal (income tax and GST cuts) and monetary (lowering of interest rates) stimulus. High frequency indicators have steadily improved over the last few months with rural demand continuing to hold up well and urban demand too showing signs of uptick. Inflation remains well anchored and though it's expected to rise from here on due to the base effect, it's likely to remain close to RBI's target of 4%.

Looking ahead, India's growth is likely to be steady as Government continues to take up reform measures. Monetary easing too will continue to boost demand this year as monetary policy works with a lag. Several trade deals, especially those with the EU and US, will also support growth going forward. However, the recent flare up in geo-political tensions in west Asia poses risk to India's growth and inflation as India's dependence on the region remains high not just through trade but also remittances.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.