Market Review - December 2025

Last Updated On: 27 Jan 2026

5 min read

Macroeconomic Update

Macroeconomic Update Debt Market Update

Debt Market Update Equity Market Update

Equity Market Update

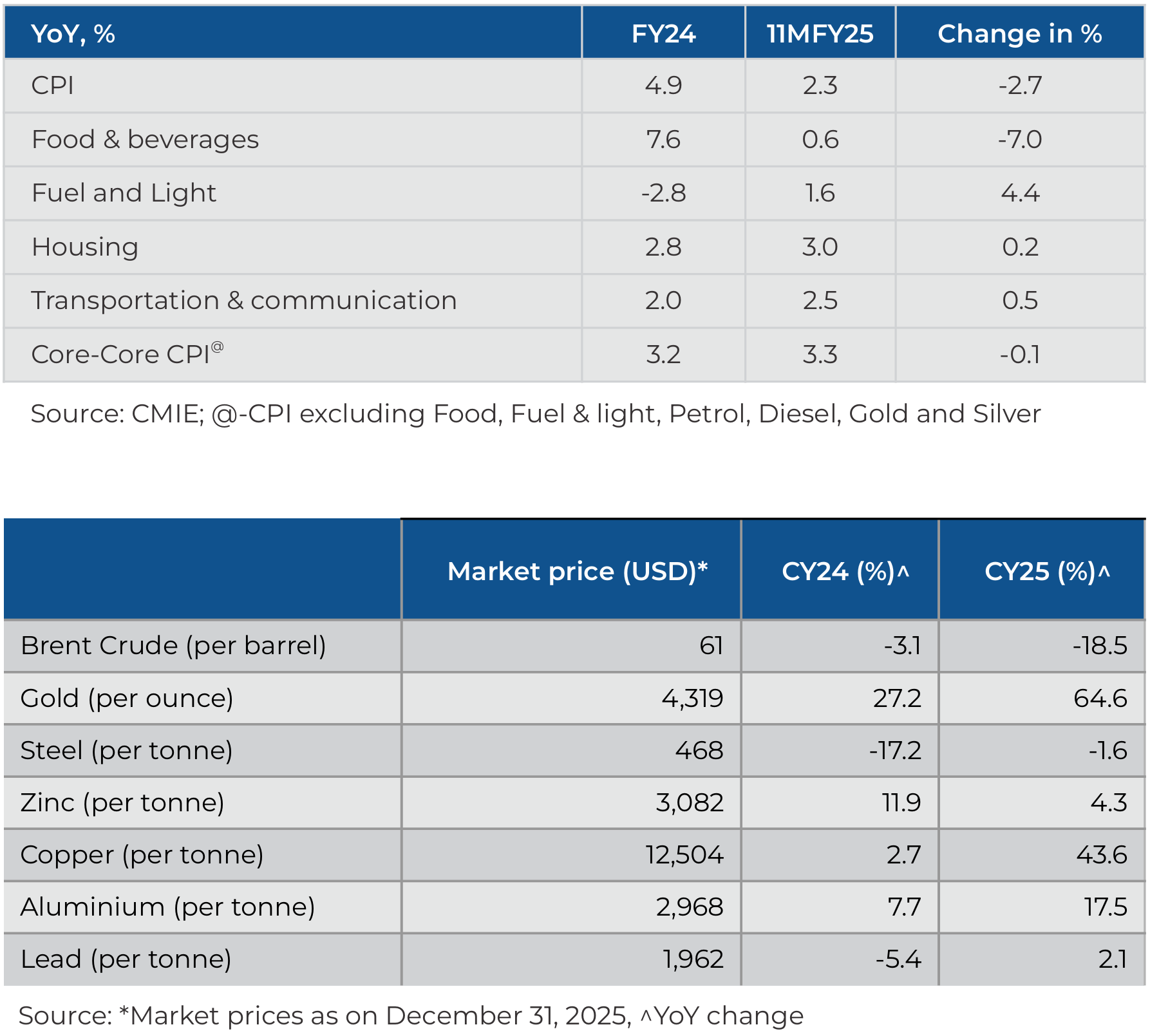

Macroeconomic Update

CY25 was a year when global growth held up well despite heightened uncertainties. The growth was particularly resilient in US which benefitted from strong AI/Tech related investments. However, resilient growth did not help the labour markets in the US where job creations fell, and unemployment rate inched up. EU and Japan also witnessed growth acceleration in CY25. Growth in China on the other hand remained subdued due to depressed domestic consumer demand amidst a slump in the property markets which deepened further in CY25.

Inflation remained contained across geographies which helped central banks reduce rates in CY25 (except Japan). While the US Fed cut the policy rate by 75 bps, ECB by 100bps, and China by ~85bps, Bank of Japan raised rates by 50bps as inflation there remained above target.

Few key developments in CY25 were:

- Mr. Donald Trump was elected as the President of the USA for the second time. He signed 225 sweeping directives in 2025 alone, which included protectionist tariffs against major economic partners such as China, Mexico, Canada, the EU, India, etc. However, some of the tariff impact has been mitigated through trade deals and negotiations. The new government has adopted a more stringent stance on immigration as mass deportation campaigns have commenced, while H-1B visa processing norms have been tightened.

- During the first half of 2025, tension in the Middle East heightened as the US and Israel conducted airstrikes in Iran but eventually it eased as Israel and Hamas entered a ceasefire agreement.

- The Russia-Ukraine war entered its fourth year with intensified drone strikes and stalled negotiations.

- A brief armed conflict erupted between India and Pakistan after India's Operation Sindoor missile strikes on May 7 targeted terrorist camps in Pakistan following the April 22 Pahalgam attack that killed 26 tourists.

- Japan undertook a rate hike cycle: Japan increased its policy rates twice, with the rate currently at 0.75%, the highest in 30 years. Japan's tight monetary policy actions are a response to elevated inflation in the country.

- Major European countries undertook a shift in fiscal policy. Germany announced in March 2025 that it plans to loosen its constitutionally enshrined limit on annual borrowings.

- In October 2025, China drastically expanded export controls on rare earths, battery materials, and superhard materials, notably asserting extraterritorial jurisdiction via a "0.1% Chinese-origin" licensing rule for global products.

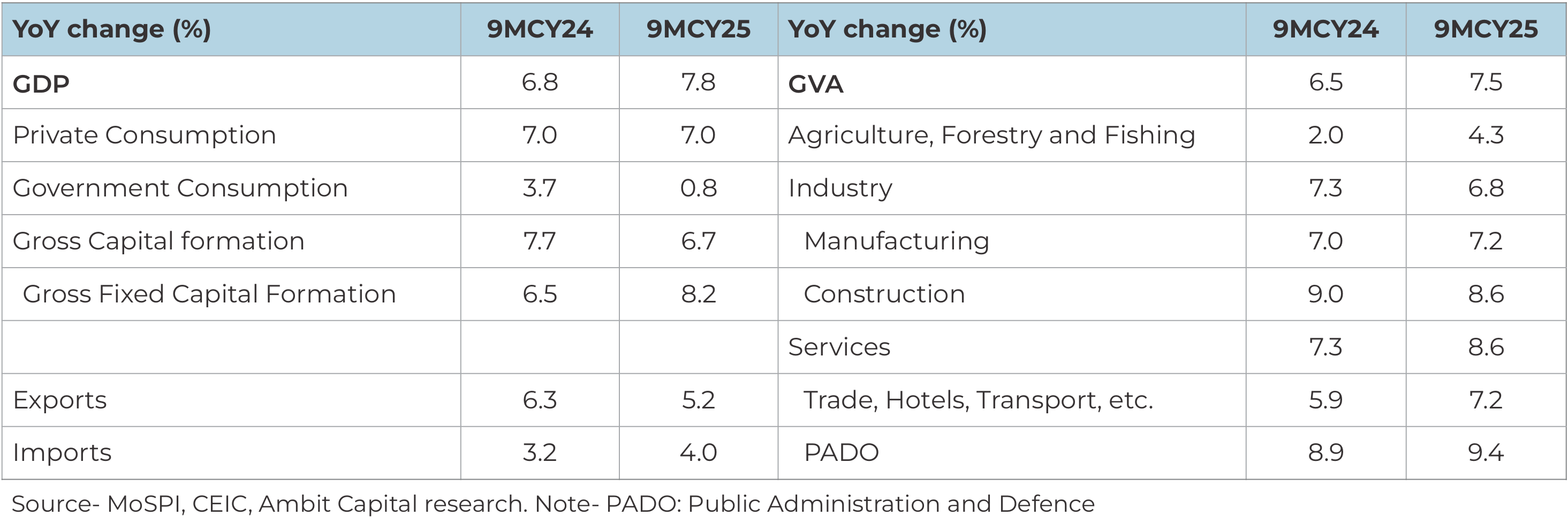

Real GDP growth remained robust in CY25:

India's real GDP grew by 7.8% YoY in 9MCY25 (as against 6.8% YoY in 9MCY24) despite uncertainties on the external front. Growth was driven primarily by Agriculture and Services sectors. While consumption growth remained steady on the back of strong rural demand and tax cuts, investment growth accelerated led by Government capex. However, Government consumption expenditure decelerated as revenue expenditure was curtailed in the face of slowing tax revenue growth. India's nominal GDP growth decelerated compared to last year as both WPI and CPI trended lower leading to much lower deflator.

Going forward, real GDP growth is likely to normalize as inflation picks up from current levels. However, growth is expected to remain steady on the back of Government's renewed push to revive demand through tax cuts and reform measures and lagged effect of monetary easing. However, the impact of higher US tariffs and flareup in geo-political tensions are key risks to growth this year.

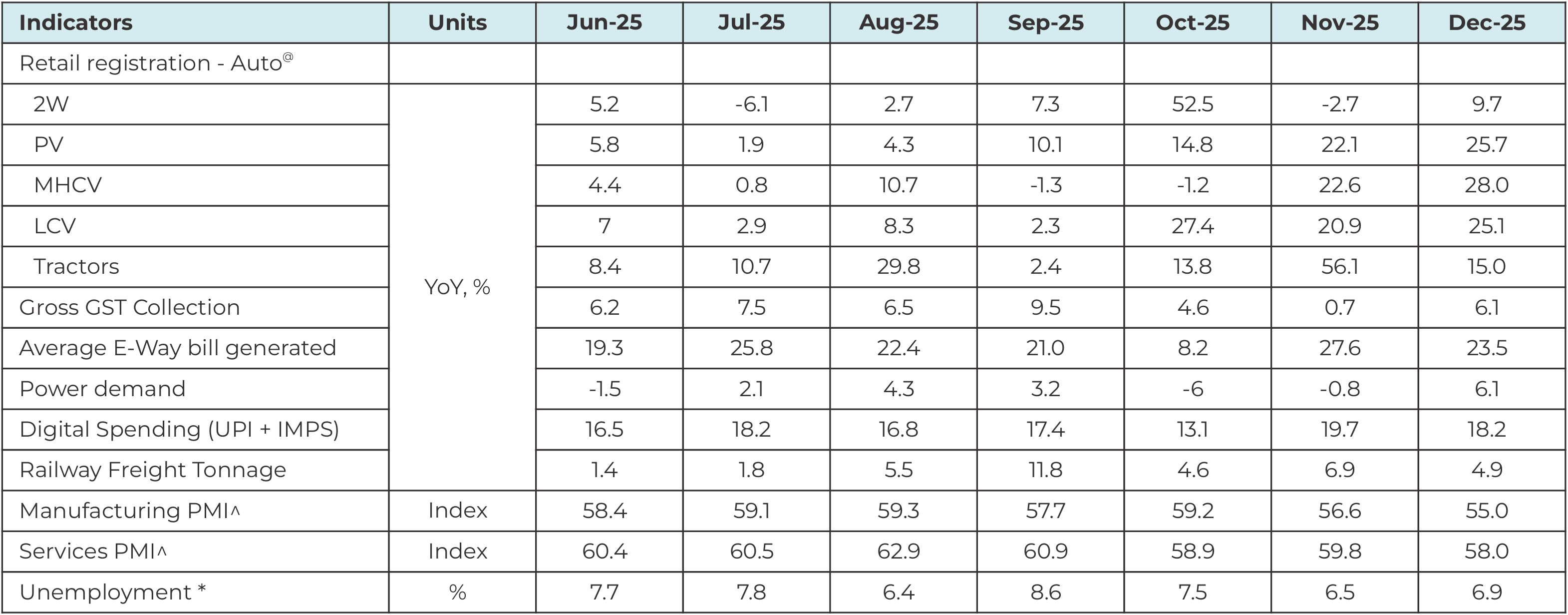

Indian economic activity remained upbeat in Dec: The high frequency indicators for December suggests that growth continues to hold up well. The effect of tax cuts on demand is clearly visible especially on vehicle registrations which continue to post strong growth for third month in a row (GST cuts became effective on 22nd September 2025). Power demand too rebounded in December following two consecutive months of contraction.

Going forward, demand is likely to remain healthy on the back of tax cuts and lagged effect of monetary easing. Prospects of a good rabi harvest and low inflation is likely to keep rural demand buoyant. However, external dynamics remain a key risk to growth.

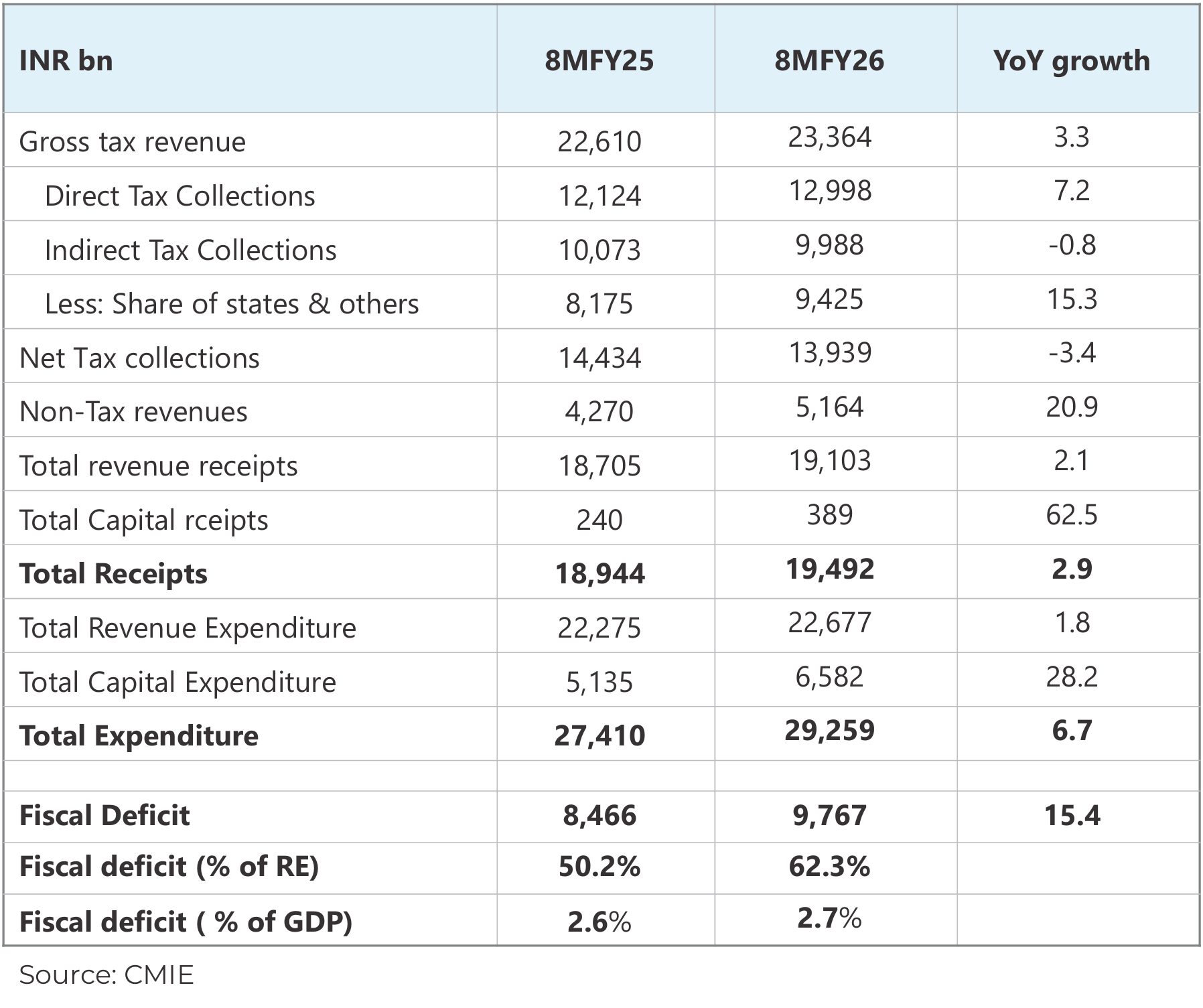

Tax revenue growth remains under pressure: Tax revenue growth has remained sluggish due to income tax and GST cuts announced by the Government to boost demand. Gross tax revenue in the first 8 months of this fiscal is up just 3.3% YoY. On the spending side, the Government has shown restraint. While capex growth has started moderating post front loading in the first of the fiscal, revex is up just 1.8% YoY in 8MFY26.

Summary and Conclusion:

Contrary to expectations, global growth held up remarkably well in CY25 led by the US where the growth consistently surprised on the upside supported by AI/tech related investments and strong consumer demand. However, job creation in the US has not kept pace with rising GDP growth. Growth in EU and Japan too accelerated and held up well in CY25. On the other hand, growth in China remains subdued as property markets continue to slump dampening consumer sentiments. The outlook for CY26 remains clouded amidst trade related uncertainties and risk of geopolitical flareups. The sovereign debt levels remain uncomfortably high especially in the advanced economies, and pressure to increase expenditure has resulted in long-term Government bond yields being elevated. This is also a potential source of risk going forward.

Real GDP growth in India surprised on the upside in CY25 even as nominal GDP growth came off due to significant fall in both CPI and WPI. Government's stimulus measures in the form of tax cuts and monetary easing by the RBI have helped lift urban consumer demand while rural demand has held up well due to back-to-back bumper crops and lower inflation. CPI inflation moderated significantly in CY25 led by a fall in food prices and GST cuts and even though inflation is likely to rise from current levels, it will remain close to RBI's target.

Looking ahead, India's growth is likely to be steady as Government continues take up reform measures. Monetary easing too will continue to boost demand this year as monetary policy works with a lag. However, lack of trade deal with US will continue to be a drag on growth as India faces on the of the highest tariff rates in the world by the US. Overall, medium-term outlook for the Indian economy seems optimistic, in our view.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.