Market Review- October 2025

Last Updated On: 22 Jan 2026

5 min read

Macroeconomic Update

Macroeconomic Update Equity Market Update

Equity Market Update Debt Market Update

Debt Market Update

Macroeconomic Update

The US and China last month reached a broad framework under which trade agreement will be discussed. In the interim, US agreed to lower import tariff on China while the latter agreed to ease export restrictions on rare earth minerals and magnets. The Government shutdown in US - which has impacted release of official economic data - has made decision making difficult for policymakers. However, in its latest FOMC review the Fed chair highlighted that alternative jobs data suggests that the labour market is broadly stable. The US manufacturing activity in October contracted at a faster pace as production slipped but Services sector held up well. While manufacturing activity in eurozone was slightly better in October than September, China's manufacturing activity deteriorated as exports orders fell at its sharpest pace in the last six months.

Inflation remained within a narrow range and largely on expected lines across most major economies. The Fed cut its policy rate by 25bps in its October review, but tempered market expectations of a rate cut in December. The Fed has indicated that it will be data dependent in its decision going forward. Both European Central Bank (ECB) and Bank of Japan (BoJ) kept its policy rates on hold along expected lines.

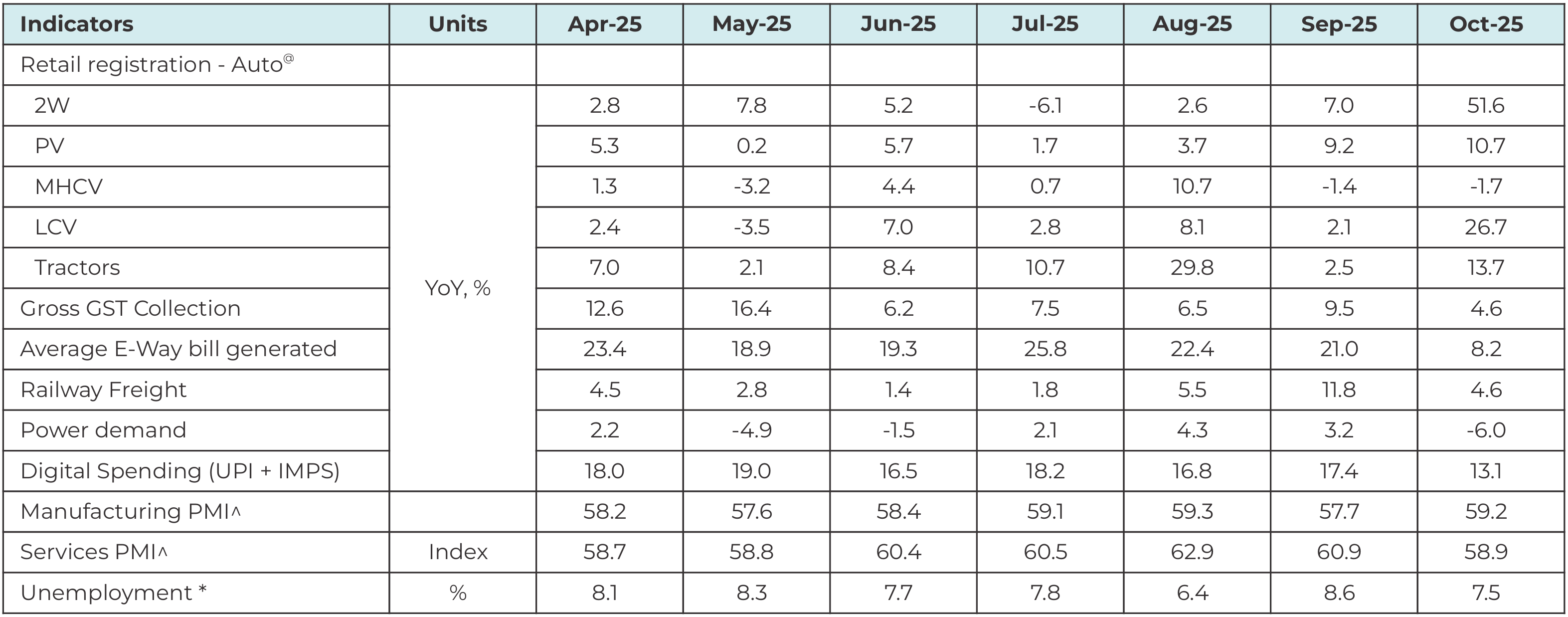

High frequency indicators remained encouraging in Oct: Pace of TW and PV registrations improved especially that of two TWs as GST cuts and festive season boosted demand. Both Manufacturing and Services PMI readings for October suggests robust economic activity with manufacturing PMI surging to nearly 17 years high in October. However, power demand contracted in October and has remained tepid in recent months mainly due unseasonal rains and resultant lower demand for cooling.

Going forward, urban demand is likely to get a boost from income tax cut, GST tax cut and easing monetary conditions while rural demand too is likely to remain steady on back of strong rabi output and above normal monsoon. However, global trade uncertainties higher US tariff on Indian imports and unseasonal rains are likely to hurt growth in the near term.

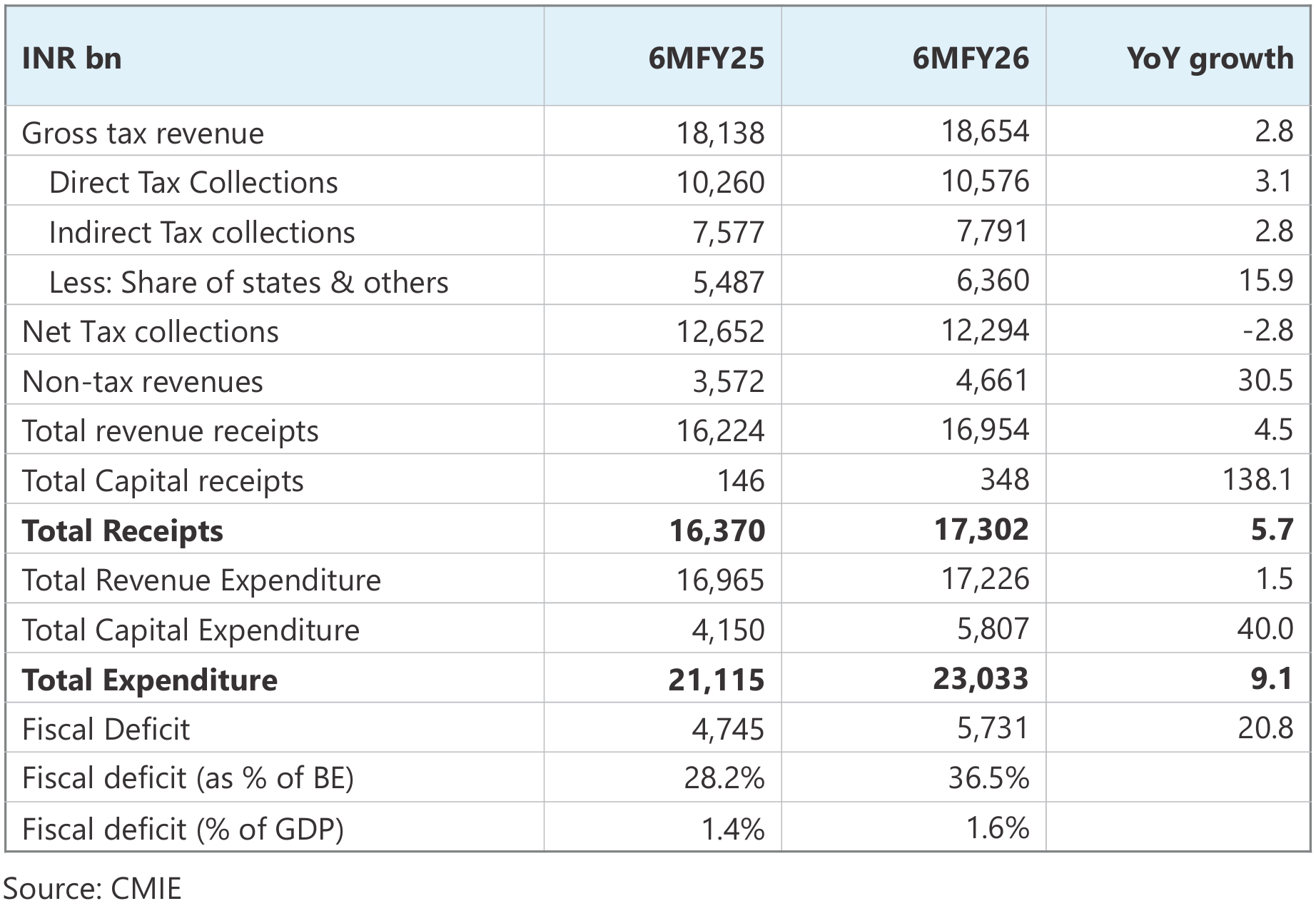

Tax collections under pressure: Gross tax revenue growth in the first six months of this fiscal has been sluggish driven by poor growth in both direct tax and indirect tax collections. The Government has given relief to consumers by cutting both personal and GST tax rates which will impact tax revenue collections this year. Total expenditure growth in first 6 months of this fiscal has been decent driven by front loaded capital expenditure even though revenue expenditure growth has been muted. Consequently, fiscal deficit has widened to 37% of BE in the first 6 months compared to 29% of BE during the same period last year. However, risk of fiscal slippage in FY26 remains low as the Government can use a mix of lower expenditure and higher revenue from other sources (like higher than budgeted RBI dividend) to keep fiscal deficit close to budgeted.

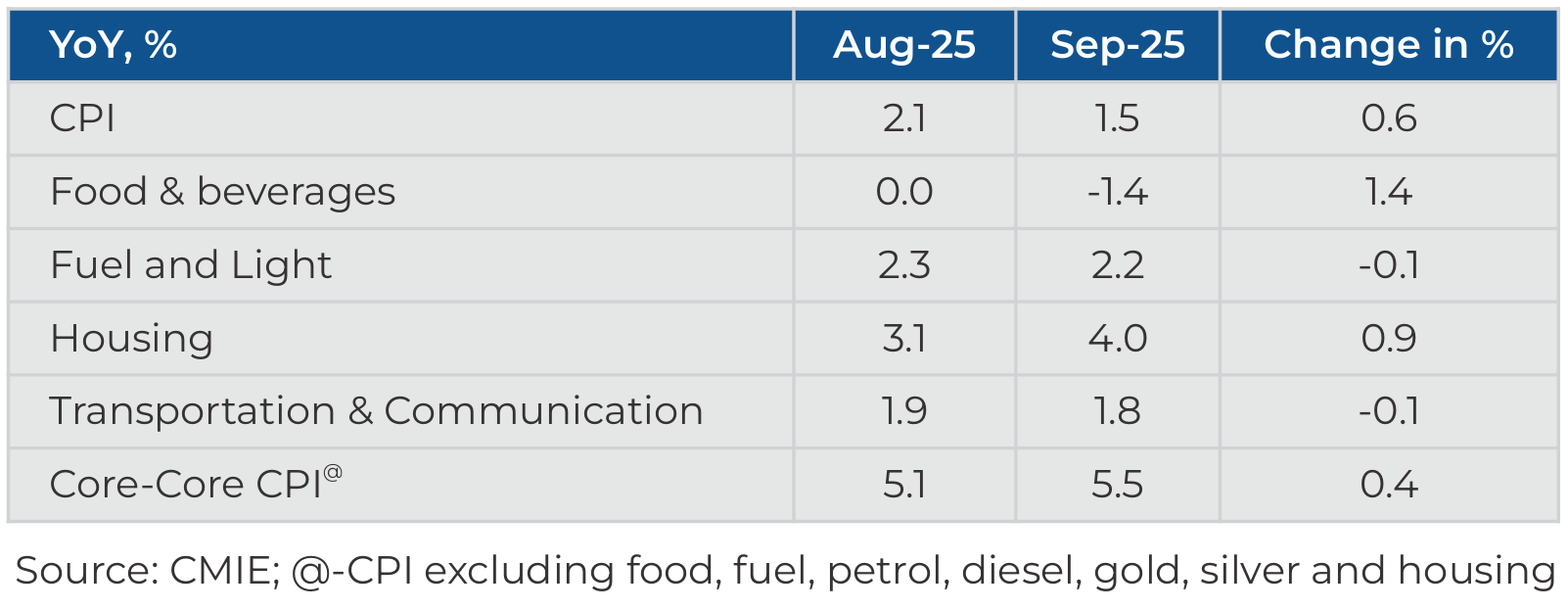

CPI inflation is likely to remain below 4% in the coming months due to favourable outlook on food inflation and favourable base effect.

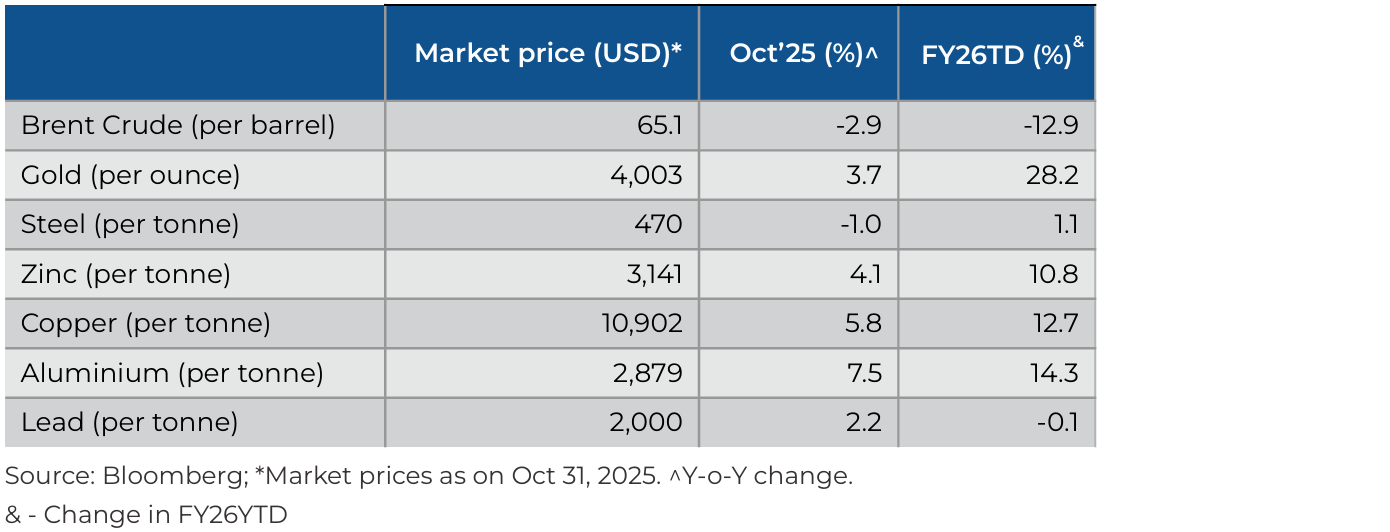

Commodity prices: Oil prices settled lower as geo-political tensions eased in middle east and OPEC+ agreed on modest output hike. China's tightening of supply led to rally in the prices of the industrial metals, but lackluster economic data globally led to steel prices cooling down.

Summary and Conclusion:

Global trade tensions subsided last month as US and China reached an agreement where US agreed to lower tariffs on Chinese imports while China agreed to lift restrictions on rare earth minerals exports. However, trade related uncertainties still remain high especially for countries like India which has been subjected to one of the highest tariff rates in the world by the US. Growth in US is being held up by AI related investments. The paucity of fresh economic data in the wake of US Government shutdown has made it difficult to track developments. The Fed chair in its press conference post FOMC meeting highlighted that the labour market has remained broadly stable and that inflation is likely to rise as tariff pass through takes place but is likely to be a one time increase rather than generalised spillover. Domestic demand in China remains subdued and deflationary forces have gathered steam. Growth in Eurozone has been better than expectations but remains below par.

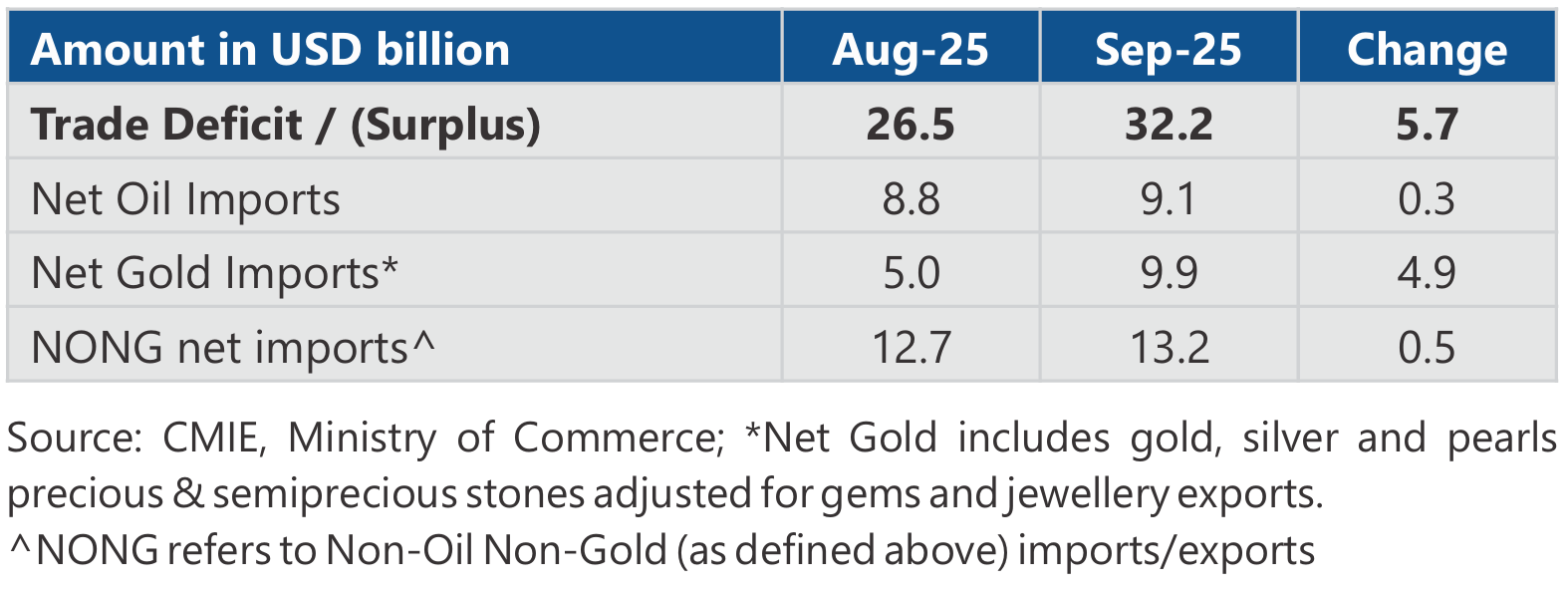

India's growth momentum is exhibiting signs of resilience as evident from recent high frequency indicators. GST rate cuts and festive demand has led to higher discretionary consumption. However, as India faces one of the highest tariffs by US on its exports, growth is likely to take a hit in the second half of this fiscal. The Government has realised this and has embarked on major reform overhaul for the country starting with lowering of GST rates to boost consumption. Going forward urban consumption is likely to remain healthy due to income tax relief and GST rate cuts announced by the Government and monetary easing by the RBI. Rural consumption too is likely to remain steady on the back of above normal monsoon, falling inflation and higher real rural wage growth. India's external sector also remains comfortable on the back of low current account deficit and adequate forex reserves. Rise in geopolitical tensions and tariff related uncertainty are key near-term risks.

Looking ahead, the medium-term outlook for India's economy seems optimistic, in our view. This optimism is driven by bi lateral trade deals with various countries, Governments renewed efforts for structural reforms, enhanced infrastructure investments, and the likely boost to private consumption.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.