Market Review- November 2025

Last Updated On: 22 Jan 2026

5 min read

Macroeconomic Update

Macroeconomic Update Equity Market Update

Equity Market Update Debt Market Update

Debt Market Update

Macroeconomic Update

The US growth remained steady although the overall picture remains hazy due to paucity of data due to government shutdown. Labour market showed mixed signs with September NFP rising by more than expected while previous two months numbers were revised lower. While October and November month labour market related data is delayed, other proxy indicators like initial jobless claims were holding up well. However, the ADP private payroll data came in weaker than expected. November Manufacturing PMIs gave mixed signals with S&P PMI improving and staying in expansionary zone while ISM manufacturing deteriorated and remained in contractionary territory. As the US government shut down has ended, picture on the US economy will be clearer henceforth. On the other hand, China growth momentum slowed down with retail sales, industrial profits, etc. moderating and f ixed assets investments growth decelerating sharply. PMIs also remained in contractionary zone. Eurozone remained steady supported by services sector as reflected in PMIs.

Inflation remained within a narrow range and largely on expected lines across most major economies. US Fed which reduced the rate by 25 bps in its October meeting is expected to cut further in December 2025 as per current market pricing. Both European Central Bank (ECB) and Bank of Japan (BoJ) kept policy rates on hold along expected lines.

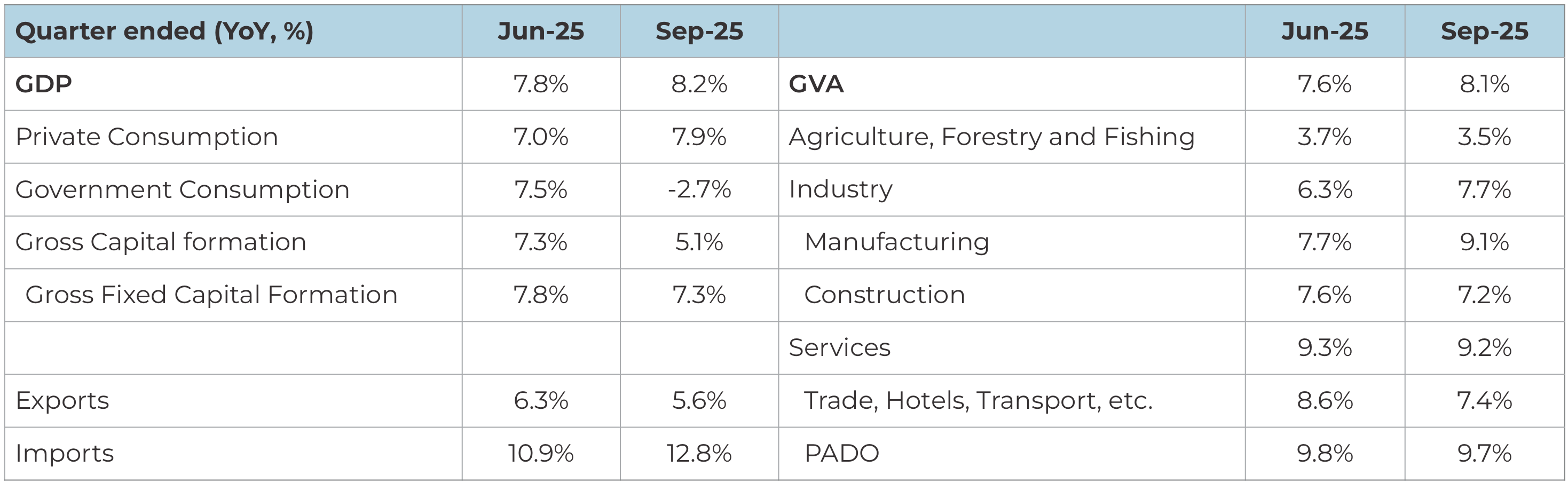

India's Real GDP shoots up on broad based strength; Nominal GDP growth remains muted: GDP growth in Q2FY26 came in significantly stronger than market expectations driven by broad based resilience and a favourable base. Private consumption grew close to 8% as tax cuts and early festive season boosted demand. Further, GFCF grew at a healthy pace on back of robust government capex. However, this was partially offset by contraction in government revenue spending and strong imports. GVA grew by equally strong pace on back of robust industrial and services growth. While festive season led production growth boosted manufacturing, services growth was driven by PADO and growth in financial & real estate services. Further, the construction sector continues to grow at a healthy pace driven by growth in government capex.

Nominal GDP growth has moderated substantially over the past couple of quarters as the deflator which is a combination of WPI and CPI has been near historical lows. While real GDP growth is largely tracked, the weakness in nominal GDP is equally important as it has implications on corporate profitability, government debt to GDP and tax collections.

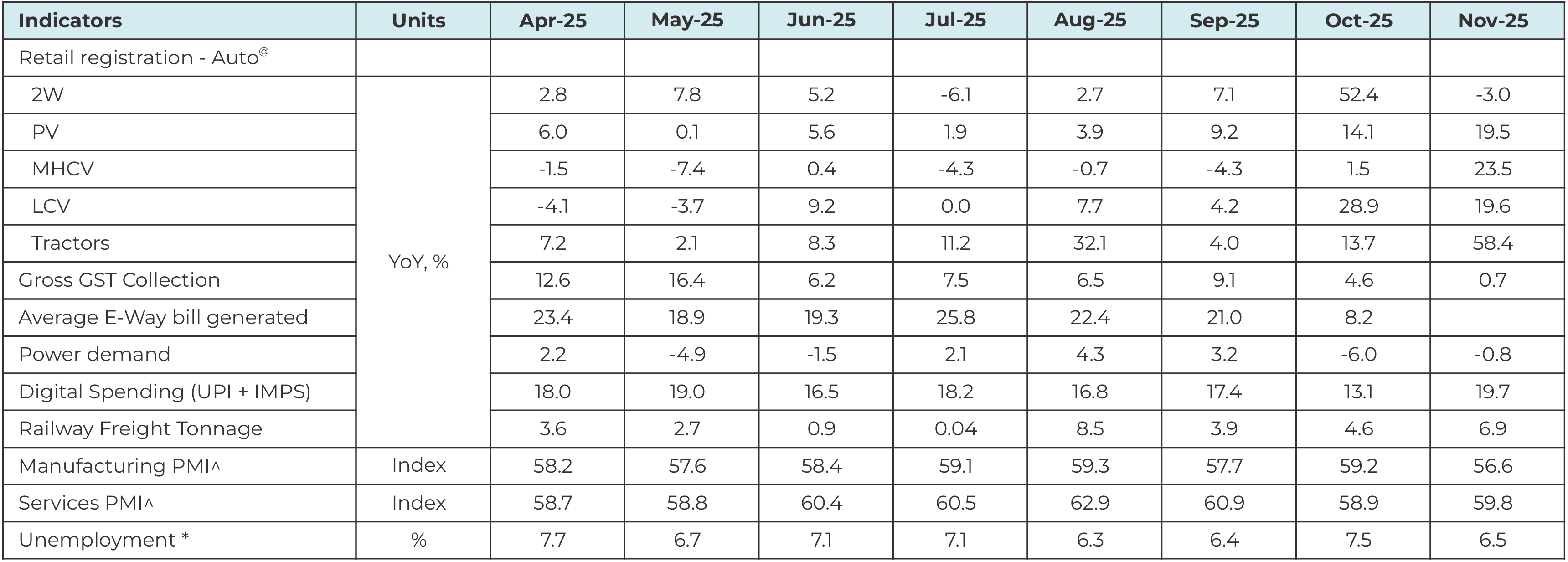

High frequency indicators holding up well in November: The recent activity indicators suggest that growth continues to hold up well over the past two months led by consumption. The retail auto registration growth was buoyant post the GST rate cuts in September while digital spending continued to grow at a healthy pace. However, some moderation was observed in the economic indicators with PMIs decelerating while power demand contracting YoY partly due to extended monsoon. GST collections growth was flat YOY mainly due to rate rationalisation.

While the GST rate rationalization has aided the consumption boost in the past two months, future sustenance of the same remains to be seen and is likely to determine the growth trajectory in coming quarters. In view of the strong growth in H1FY26, FY26 growth is likely to be higher than 7%, although the growth rate is likely to decelerate in H2FY26. Global trade uncertainties, elevated US tariff on Indian imports and unseasonal rains can act as a near term headwinds.

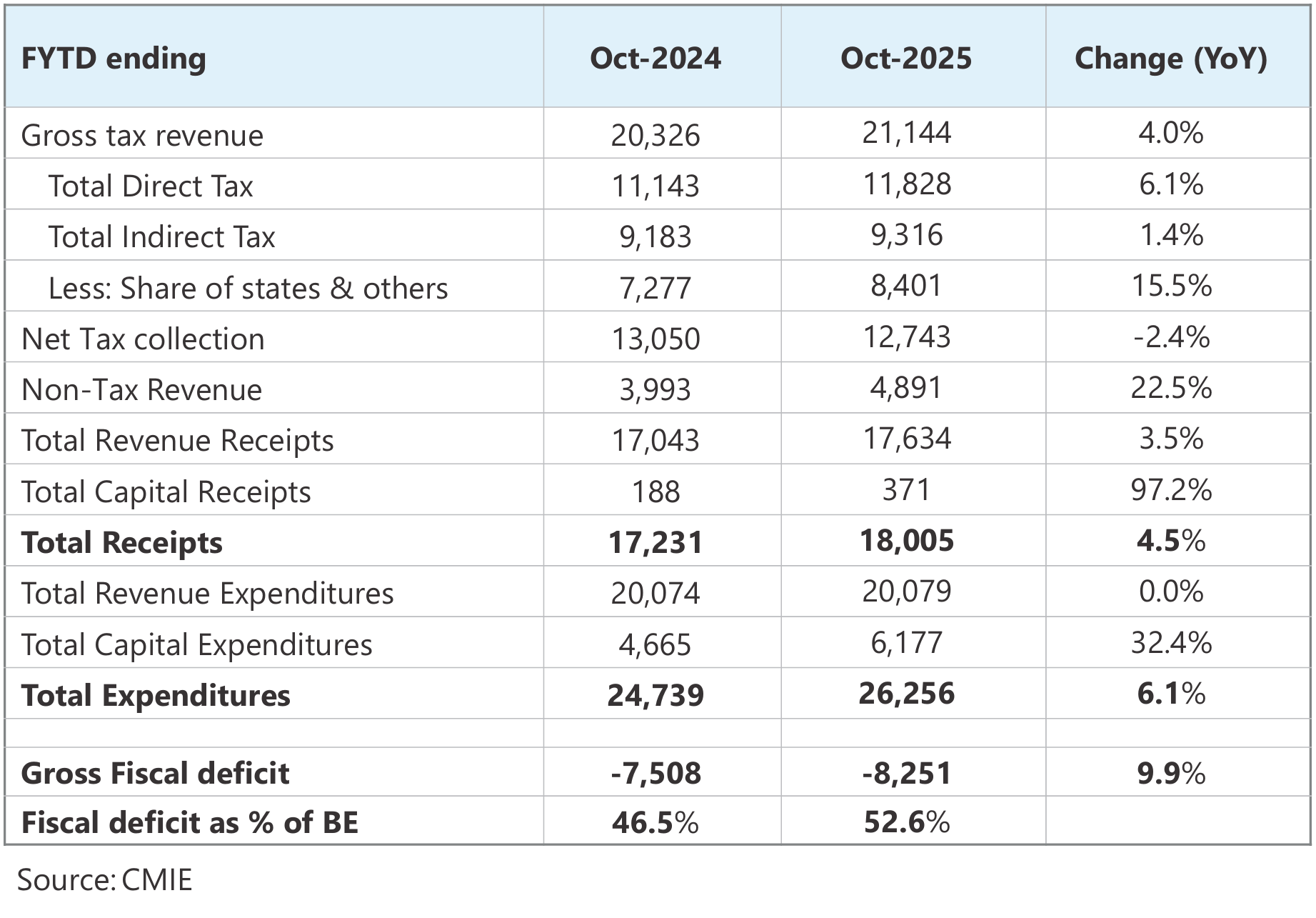

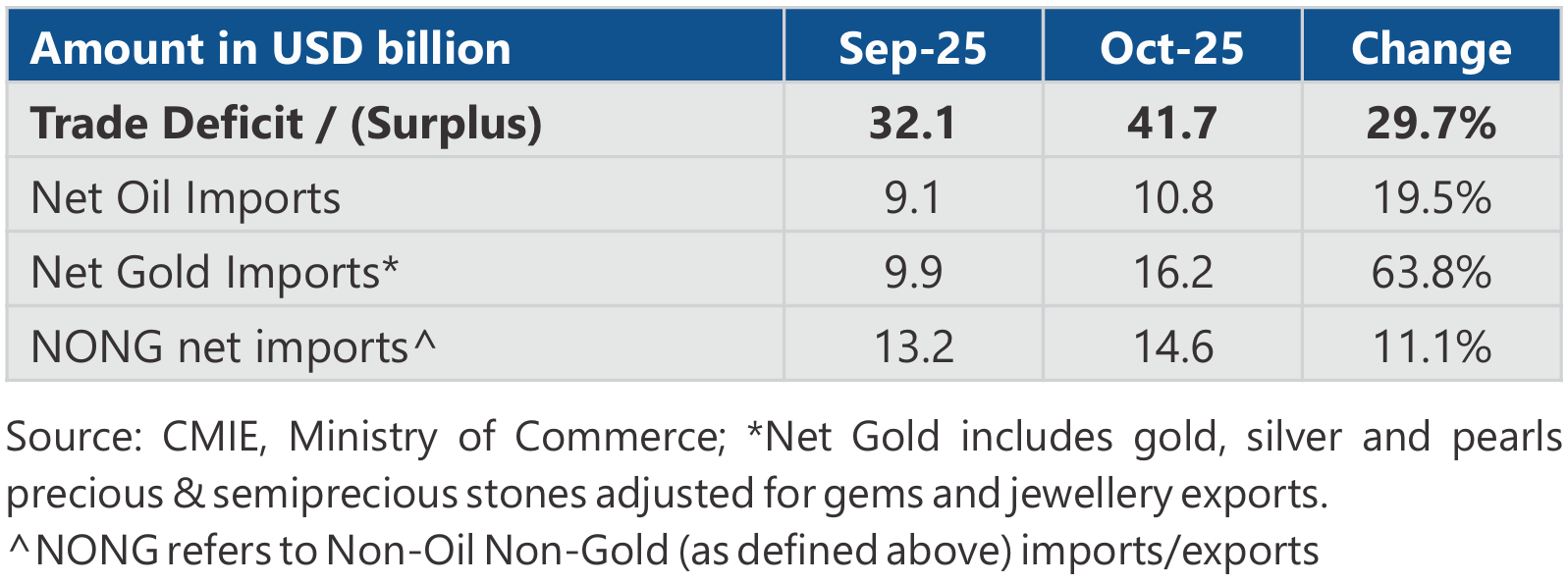

Risk of fiscal slippage rises, but still manageable: Direct tax collections growth picked up in last few months led by improvement in personal income tax collections. However, on FYTD basis, the growth is still soft and weaker than expected in budget. The slowdown in tax collection is partly driven by reduction in income taxes announced in the budget. Further, Indirect tax growth moderated due to weakness in GST collections. This is partly due to IGST sharing settlement between Centre and states being preponed vis a vis last year. Centre continues to exercise restraint in revenue spending which was flat yoy while capex spending continues to grow at a healthy pace. Consequently, fiscal deficit has widened to 53% of BE in the first seven months compared to 47% of BE during the same period last year.

In view of weakness in tax collection and GST rate rationalization, risk of tax collections under shooting the budgeted target remains high. Further, given the weakness in nominal GDP growth, the deficit as % of GDP could be higher than budget estimates. However, this is likely set off by the higher RBI dividends, lower state devolutions and possibility of lower spending. Overall, we believe the risk of fiscal slippage has increased, although issuance of additional dated market borrowing remains low as this can be managed by higher small savings, improvement and / or usage of government cash balance.

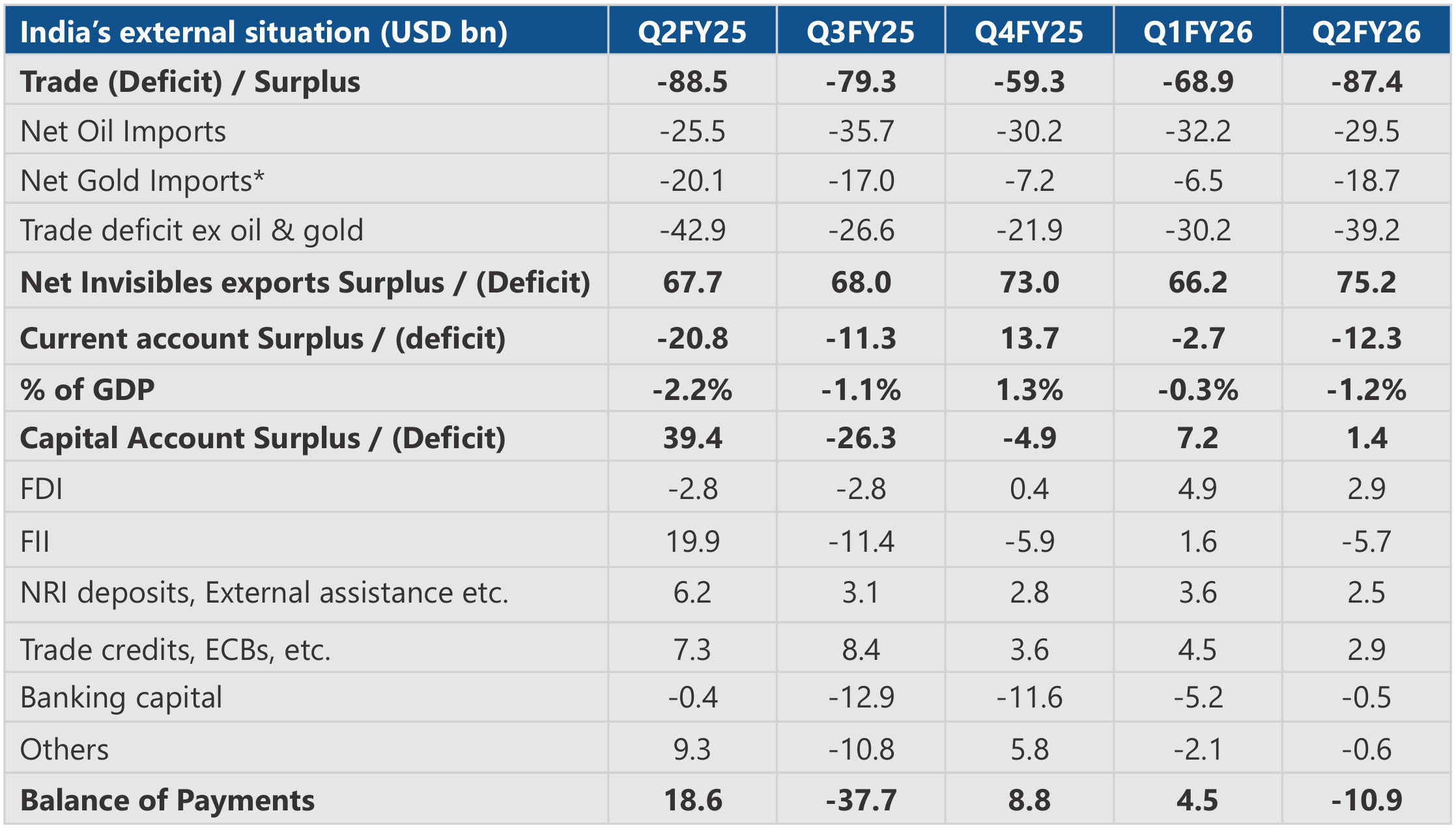

Despite widening trade deficit, current account is expected to remain within manageable range in our view supported by healthy growth in services exports. However, subdued net FDI due to exits by Private equity and foreign promoters selling along with weakness in FII flows might weigh on the capital account. Thus, BoP is likely to remain negative in FY26 but within manageable levels in view of the large forex reserves.

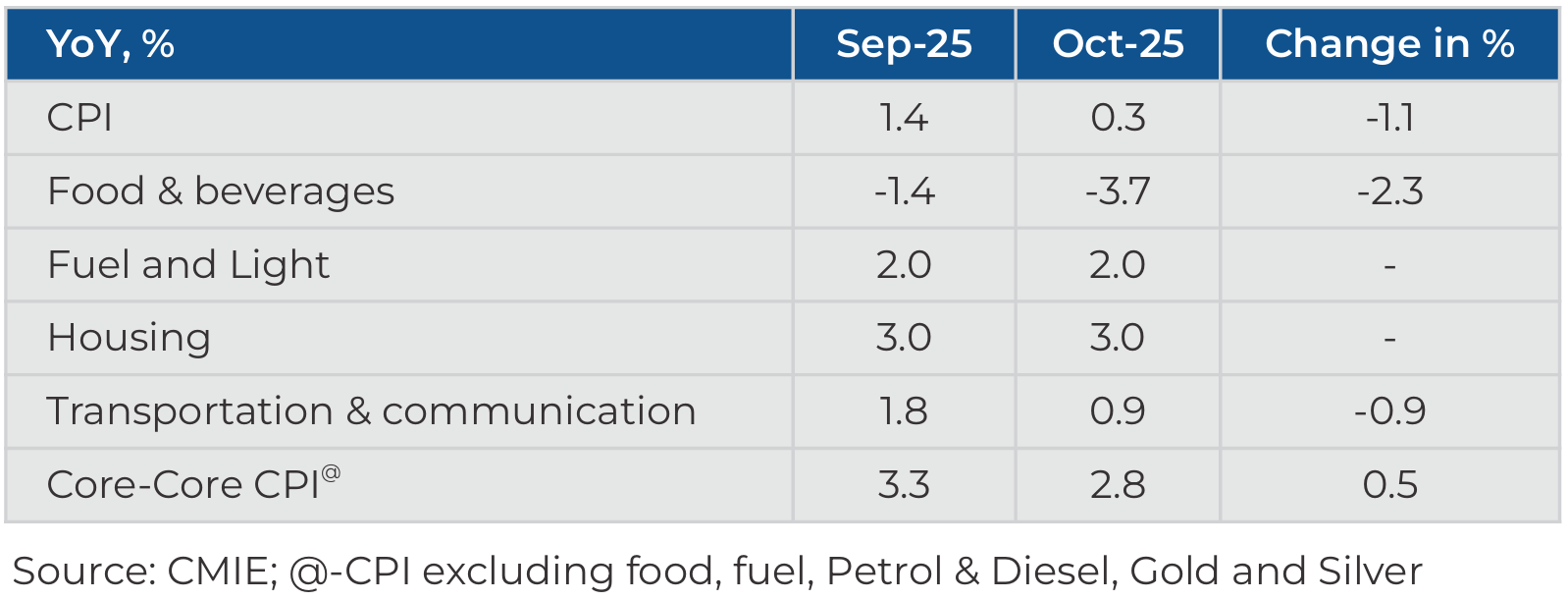

Retail inflation remains benign: India's CPI inflation in October declined to 0.3%, lowest since the beginning of the series in 2012. Bulk of the easing in inflation was driven by fall in food prices led by vegetables and pulses. Further, the transportation and communication inflation eased to 0.9% YoY on back of lower price of vehicles – car as well as two wheelers. Core inflation however inched up driven by sharp YOY rise in gold and silver. Excluding the same, the core inflation has eased to ~2.8% from 3.3% last month.

CPI inflation is likely to remain below 4% in the coming months due to favourable outlook on food inflation and favourable base effect.

Summary and Conclusion:

Global trade tensions eased after the United States and China agreed for framework for resolving trade related issues. Despite this progress, trade-related uncertainties remain elevated, particularly for countries like India, which continues to face some elevated U.S. tariff rates. In the U.S., economic growth is being supported by strong investments in artificial intelligence. However, the recent government shutdown has led to a scarcity of fresh economic data, making it challenging to evaluate economic conditions. However, this should resolve as the data releases are likely to start with an end of government shutdown. Meanwhile, domestic demand in China remains weak, and investments growth has also decelerated sharply.

Robust growth in India continued as reflected in over 8% real GDP growth in Q2FY26. Further, growth momentum remains resilient, as reflected in recent high-frequency indicators. Urban demand is likely to stay strong, supported by income tax relief, GST cuts, and monetary easing by the RBI. Rural consumption should also hold firm, aided by an above-normal monsoon, easing inflation, and rising real rural wages. However, with elevated US tariff growth is expected to moderate in the second half of the fiscal year. On the external front, India's position remains comfortable, underpinned by a low current account deficit and healthy foreign exchange reserves. Nevertheless, escalating geopolitical tensions and persistent tariff-related uncertainties remain key near-term risks.

Looking ahead, the medium-term outlook for India's economy seems optimistic, in our view. This optimism is driven by bi-lateral trade deals with various countries, Governments renewed efforts for structural reforms, enhanced infrastructure investments, and the likely boost to private consumption.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.