Globally, FY26 was a year of intense uncertainty, marked by major geo-political conflicts and imposition of tough U.S. reciprocal tariffs on economic partners. Together, these developments have clouded the outlook for the global economy in FY27. However, the US economy continued to exhibit exceptionalism despite headwinds from government shutdowns and macro uncertainty caused by tariffs. Growth in US was robust due to AI/tech related capex, but high growth did not translate into job creation as non-farm payroll kept declining. However, as crackdown on illegal immigration reduced the supply of labour as well, the unemployment rate did not increase materially. Europe witnessed a rebound in growth in last 12 months led by the services sector, however future growth remains uncertain due to the fallout from the West Asia war. Ongoing geopolitical tensions and related surge in energy prices continue to pressure manufacturing competitiveness and raise the risks of a general increase in price levels. China, meanwhile, experienced subdued growth over the past year, weighed down by weak domestic demand and sluggish property sector. However, China’s exports continued to show resilience even in the face of US tariffs as exports to rest of the world (ex US) surged last year.

The war in West Asia poses significant risks to the global economy. It’s akin to a supply shock especially for Asia given its dependence on the zone of conflict for its energy needs. If the conflict gets elongated, it risks a general increase in price levels and lower output increasing stagflationary risks.

Throughout 2025 and early 2026, a widespread calibrated easing cycle saw major central banks like the U.S. Fed and ECB cut rates by 75-100 bps as the global economy shifted from fighting inflation to supporting growth. Japan was an exception which undertook rate hikes. However, with energy prices rising sharply due to the war in West Asia, globally central banks may need to reassess their policy stance. Higher energy costs are spilling over into other commodities, increasing the risk of worsening commodity prices and a rebound in overall inflation and lower growth.

Few key developments in FY26 were:

- Liberation Day tariffs: On April 2, 2025, U.S. President invoked emergency powers to impose broad reciprocal tariffs, triggering a global market shock and a year of trade volatility. The US Supreme Court in February 2026 ruled the "Liberation Day" emergency tariffs illegal, forcing the administration to pivot to statutory trade laws.

- India-Pakistan 2025 Conflict: A four-day military escalation in May 2025 led to the suspension of the Indus Waters Treaty and the closure of regional airspaces before a ceasefire was reached on May 10.

- NATO’s 5% Defense Spending Pivot: Member nations at the June 2025 Hague Summit agreed to target 5% of GDP for defense, a massive increase driven by prolonged conflict in Ukraine.

- Bank of Japan Interest Rate Hikes: The BOJ signaled a series of rate hikes to stabilize the Yen, ending years of ultra-loose monetary policy and rattling global bond markets.

- Fed rate cuts: Fed resumed rate cuts and cut policy rates by a total of 75bps between September and December 2025

- The Israel-U.S.–Iran War: The conflict has escalated into a direct "crushing" exchange between the U.S., Israel, and Iran, resulting in the near-total closure of the Strait of Hormuz and a global surge in oil prices.

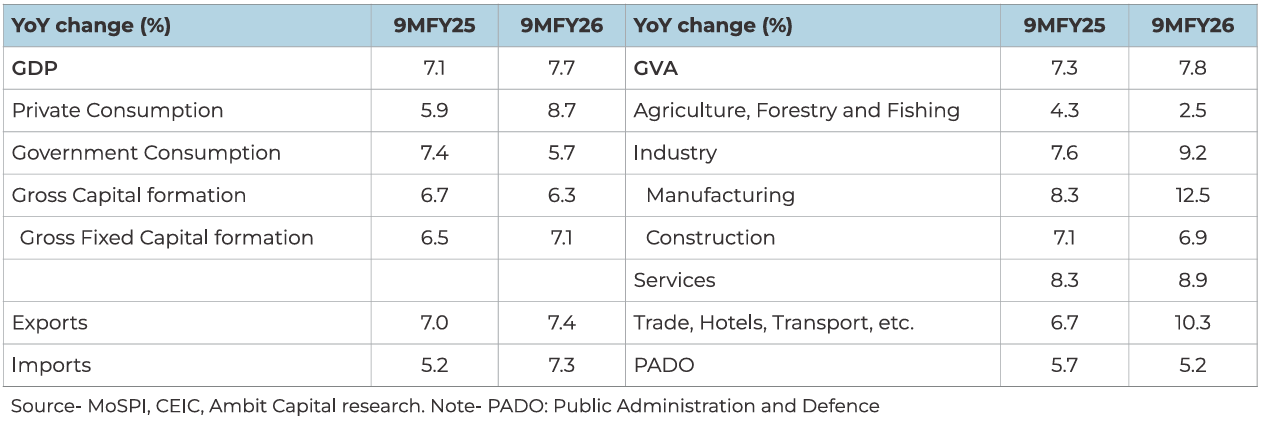

GDP growth accelerated in 9MFY26: The Government in February 2026 released the new GDP series with 2022-23 as base year (from 2011-12 earlier). The Government not only changed the base year but also incorporated significant methodological changes in the new series to make GDP measurement more robust and reflective of changes which has taken place in the past decade. The new GDP series confirms continued growth momentum. India’s GDP grew by 7.7% YoY in 9MFY26 (as against 7.1% YoY in 9MFY25). The acceleration was led by sectors, such as manufacturing and ‘trade, hotels, transport etc’. Agriculture growth on the other hand decelerated due to high base effect. On the demand side, the growth in 9MFY26 was led by private consumption and investments even as Government consumption demand moderated.

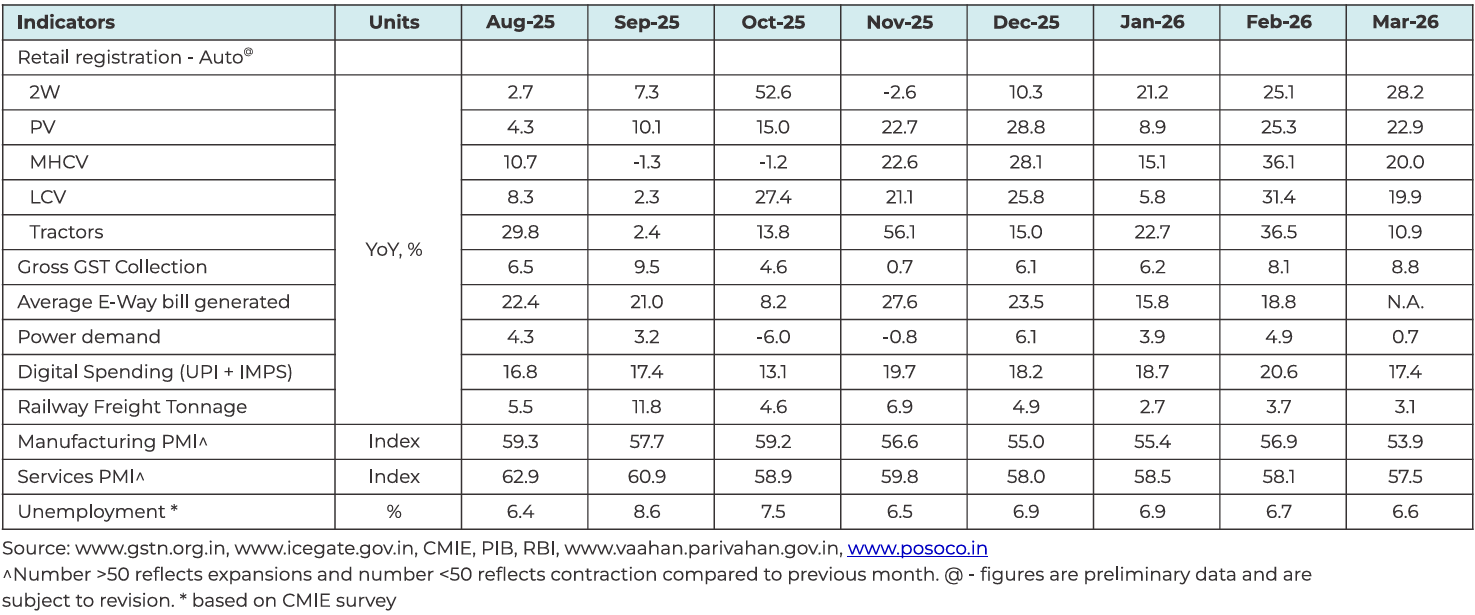

Indian economic activity was mixed in March: The high frequency indicators were mixed in March. While vehicle registrations continued to grow at a strong pace, power demand and PMIs for both manufacturing and services decelerated. The PMIs also revealed rising input cost pressure as energy prices continue to climb higher due to the war in West Asia.

Going forward, the direction and strength of demand will depend whether the temporary truce between Iran and US holds and energy supplies are restored to pre-war levels.

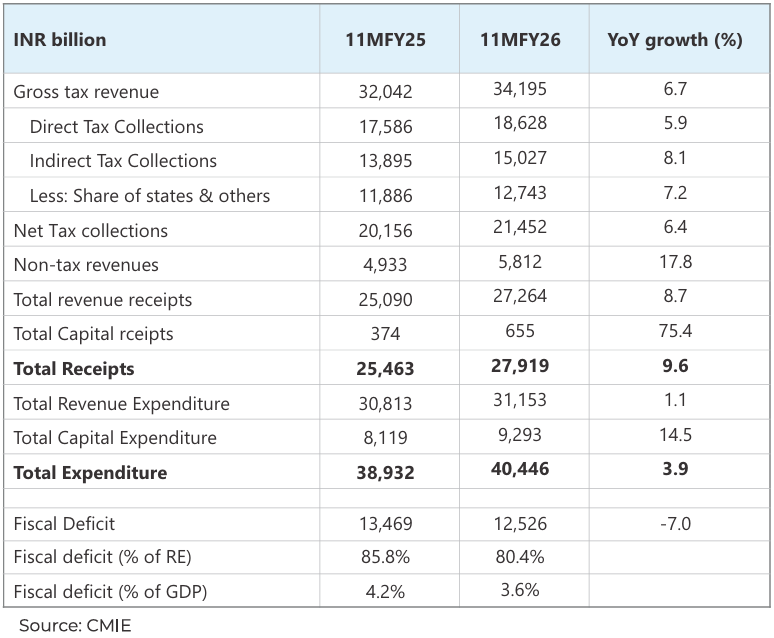

Tax revenue growth in slow lane: As Government cut both personal income tax and GST rates last fiscal, tax revenue growth has been slower, and the Government might miss the revised revenue targets for FY26. Despite the shortfall in tax revenue, the Government is likely to meet the fiscal deficit target in FY26 through a mix of higher non-tax revenue and lower expenditure than budgeted.

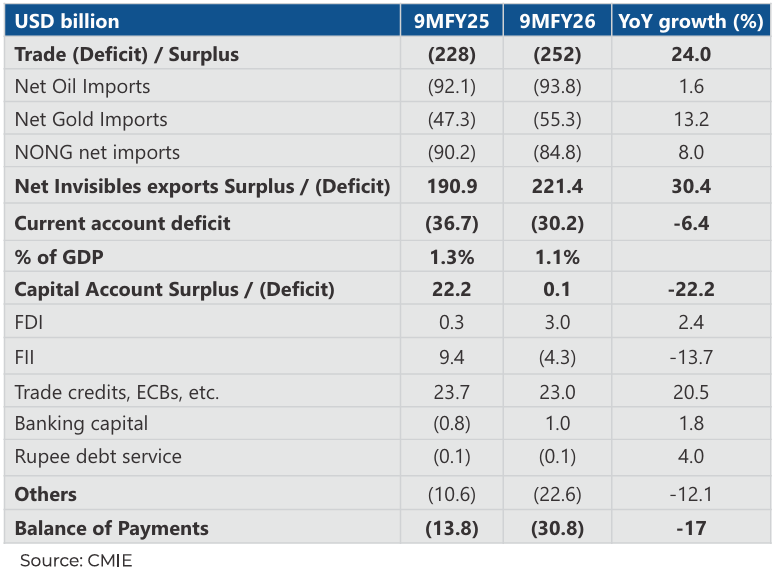

Current account deficit narrows but capital account weakens: India’s CAD narrowed in the first 9 months of FY26 due higher invisibles surplus even as trade deficit widened. However, capital account surplus narrowed significantly due to large FPIs outflows from equities leading to widening of BoP deficit.

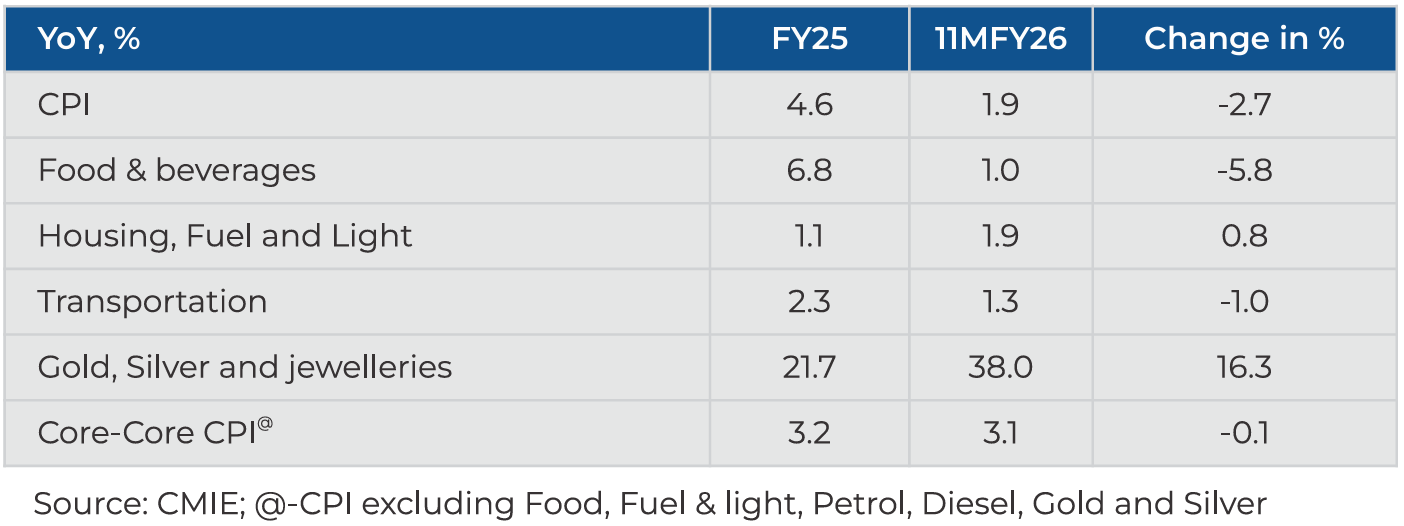

Retail inflation cools in FY26, likely to rise in FY27: CPI inflation moderated by 270bps in 11MFY26 led by decline in food prices. Ex of precious metals, core inflation too was benign as benefit of GST cuts led to decrease in prices.

CPI inflation is likely is to increase this year due to higher crude oil and other commodity prices, adverse base effect and likelihood of lower monsoon which could lead to higher food inflation.

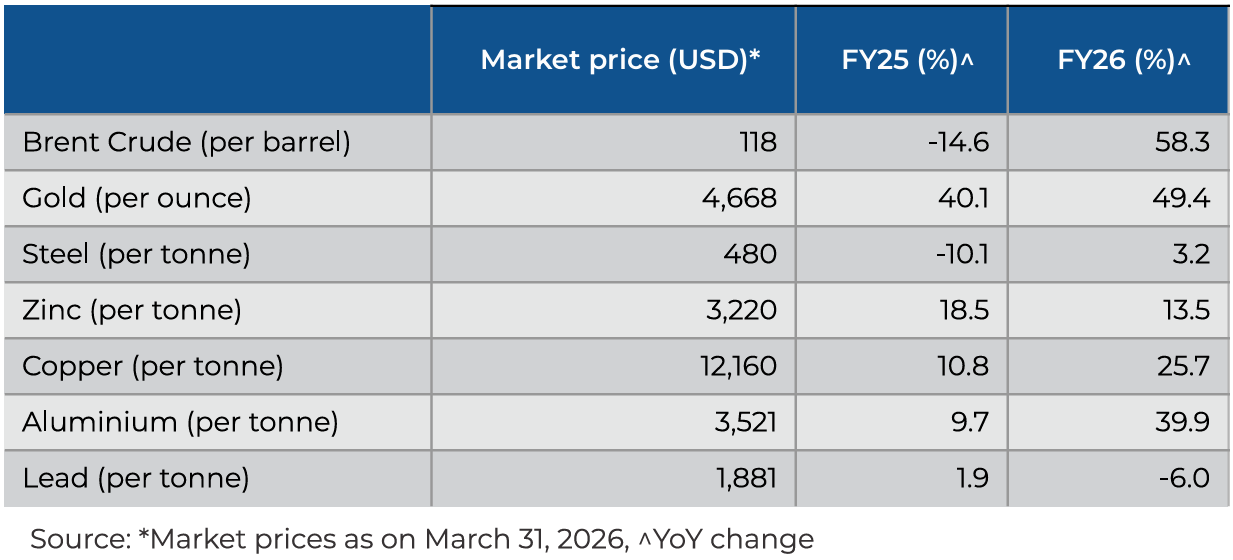

Commodity prices: While oil price remained largely benign through most of FY26, they spiked in Mar’26 following the escalation of the West Asia conflict, with the Strait of Hormuz, a critical choke point accounting for around 34%

of global oil trade, remaining shut. Elevated geo-political uncertainty continued to support gold prices during FY26. Moreover, industrial metals such as copper and aluminium benefited from increased investments in data centres and the accelerating adoption of electric vehicles. In contrast, steel prices saw only moderate gains, weighed down by Chinese overcapacity and subdued global demand.

Summary and Conclusion

Global economy faces heightened uncertainty due to in geo-political tensions in west Asia although the 2-week truce between US and Iran offers hope of early resolution of the conflict. If the conflict gets elongated, it can have profound implications for the global economy as not only energy but supply chains for various sectors will get disrupted. Growth in the US so far has held up well and prospects too were bright before the conflict started. This was due to higher AI/tech related capex and expansionary fiscal policy. However, labour markets have remained weak as evidenced by low non-farm payrolls although unemployment rate has not risen sharply as labour supply too has gone down simultaneously due to crackdown on illegal immigration. Growth in China is following a two-speed path where domestic consumption and property markets are in a slow lane, but exports and manufacturing are holding up well.

Before the start of conflict in west Asia, growth in India too had held up well on the back of fiscal (income tax and GST cuts) and monetary (lowering of interest rates) stimulus. High frequency indicators have steadily improved over the last few months with rural demand continuing to hold up well and urban demand too showing signs of uptick. Inflation remains well anchored and though it’s expected to rise from here on due to rise in crude oil and other commodity prices, and adverse base effect, it’s unlikely to increase significantly. RBI has projected an average inflation of 4.6% in FY27.

Looking ahead, the medium-term outlook for the Indian economy seems optimistic, in our view. This optimism is driven by policy continuity, benefits from production-linked incentive schemes, opportunities arising from shift in the global supply chain, and the likely boost to private consumption due to income tax relief and lower borrowing cost. However, the flare up in geo-political tensions remains a key risk to growth this year.

Macroeconomic Update

Macroeconomic Update Debt Market Update

Debt Market Update Equity Market Update

Equity Market Update