Rise in Short-Tenor Yields – An Investment Opportunity?

Last Updated On: 11 Mar 2026

5 min read

What’s the Point?

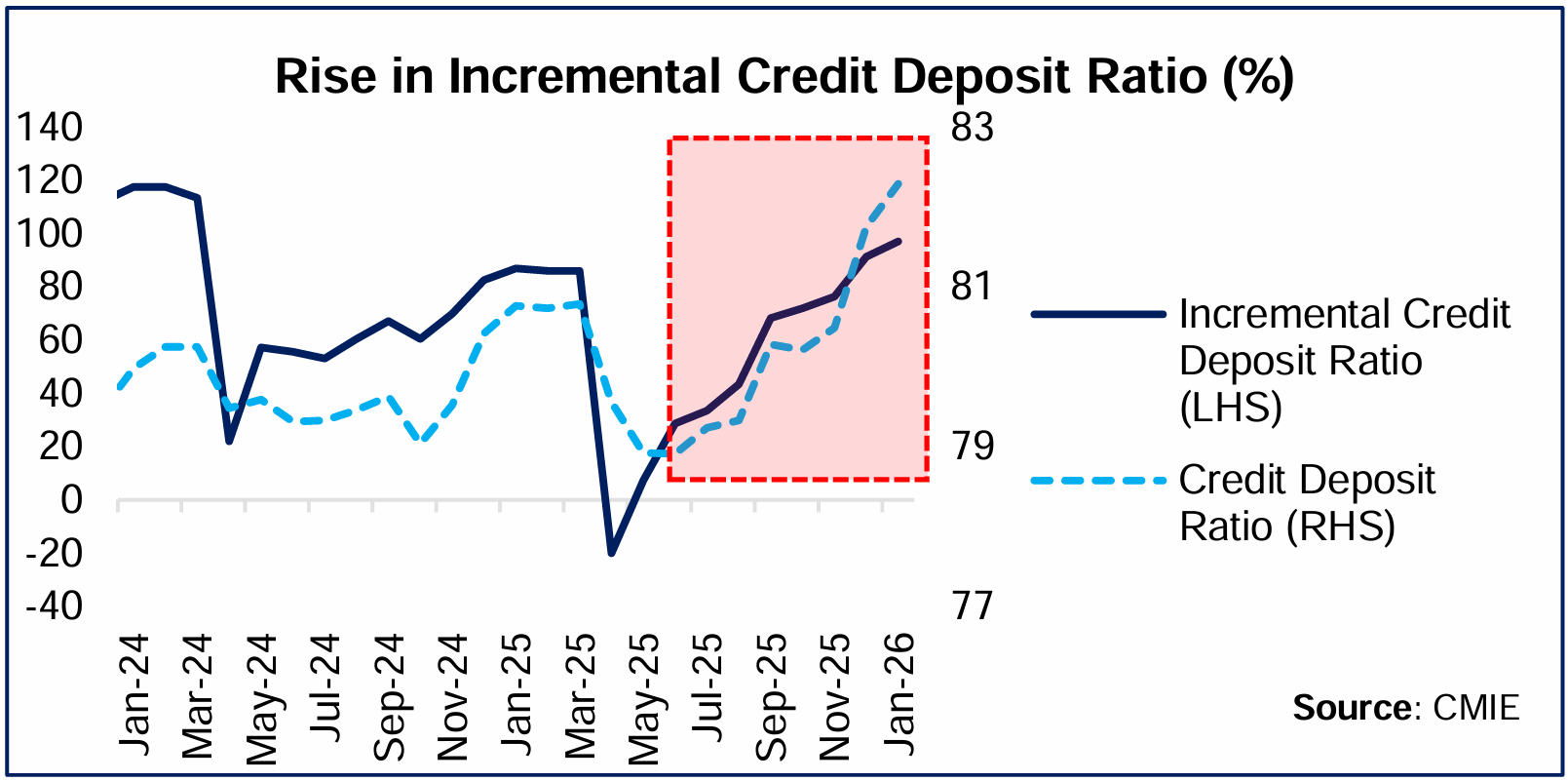

- Over the past couple of months, there has been a sharper rise in yields of shorter-tenor instruments compared to longer-tenor ones owing to tighter liquidity conditions on account of seasonal factors, RBI’s FX intervention, Credit growth outpacing Deposit mobilisation etc.

- At the shorter end, Commercial Papers (CPs), Certificate of Deposits (CDs) and Corporate yields have risen more than comparable Government Securities owing to divergent demand-supply dynamics.

- Current environment creates investment case for shorter-duration funds, which may offer a blend of higher yields, relatively lower duration risk and potential for gains if yields soften.

Past couple of months have seen rise in bond yields along with a flattening of the Yield Curve i.e. sharper rise in yields of shorter-tenor instruments compared to longer-tenor ones. This rise has been more noteworthy in Commercial Papers (CPs), Certificates of Deposits (CDs) and Corporate Bonds compared to Government Securities (G-Sec).

Money Market Divergence: Yield movement of CDs vis-à-vis Treasury Bills

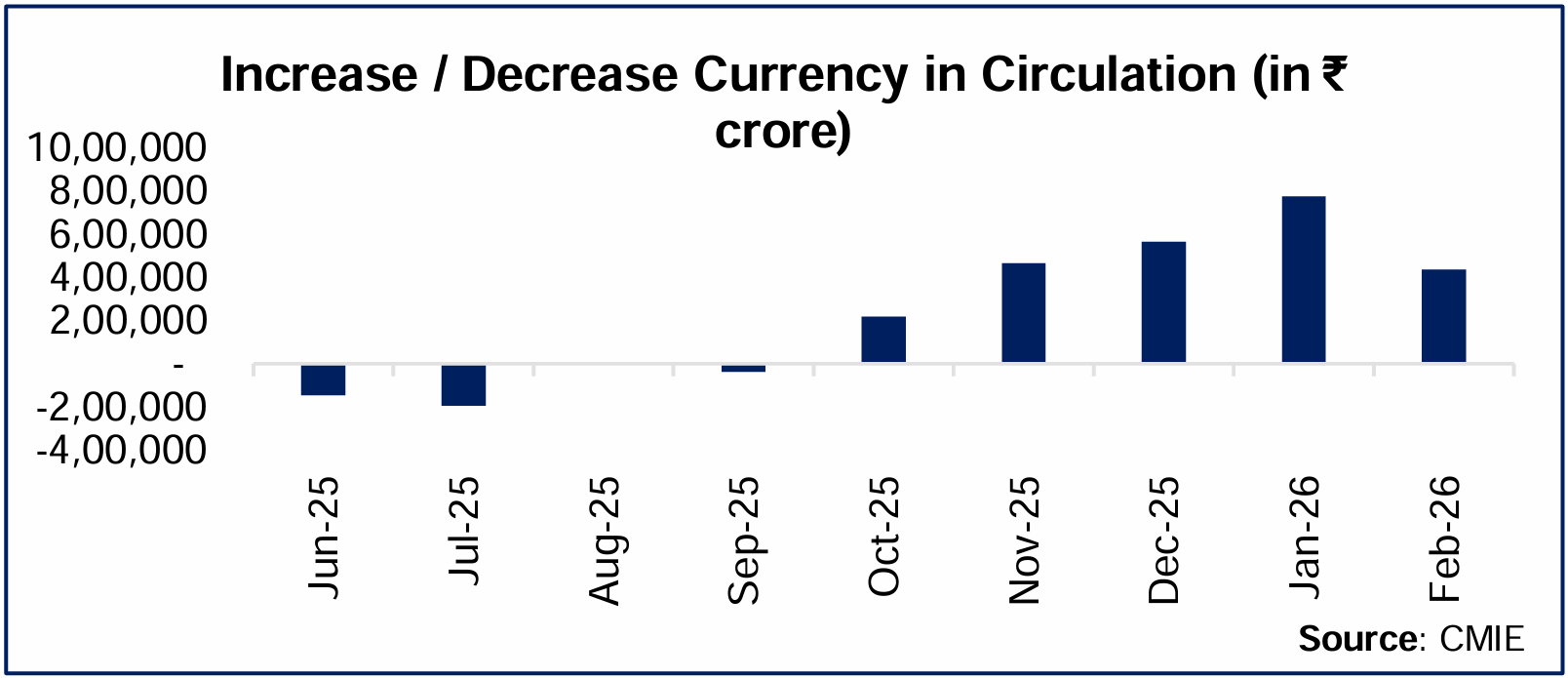

The Reserve Bank of India (RBI) has been proactive about maintaining ample liquidity in the system and has made use of liquidity management tools such as Open Market Operations (OMOs), FX swaps, Variable Rate Repo and others to aid transmission of rate cuts. However, demand supply dynamics in different segments of the Money Market have resulted in divergence in yield movement.

Over the past several months, 91-day Treasury Bill yields have moderated from their peak levels seen in late August 2025. Yields have softened by 20 bps from 5.51% on 28-Aug-25 to 5.31% on 05-Mar-26. This movement reflects RBI’s proactive liquidity management efforts.

In contrast, yields on three-month CDs have moved higher over the same period, resulting in a widening spread over comparable-maturity T-Bills. For instance, yields of 3-month AAA PSU CDs have risen by 76 bps from 6.41% to 7.17% between 28-Aug-25 and 05-Mar-26. This divergence between yields of Short-term T-Bills and CDs reflects funding dynamics within the banking system rather than a broad-based tightening of financial condition.

Why have Yields moved higher over the past couple of months?

Investment Case for Shorter-Duration Funds

As fiscal year-end pressures ease and government spending picks up, liquidity conditions could improve, potentially leading to moderation in short-term yields. Further, spreads of short-tenor corporate bonds and CDs over comparable-maturity G-Secs remain elevated vis-à-vis historical levels, indicating relative attractiveness.

At the same time, global developments such as geopolitical tensions in the Middle East warrant monitoring. A sustained rise in crude oil prices could have implications for India’s Current Account Deficit (CAD), Rupee stability and consequently, systemic liquidity conditions, with the eventual impact likely depending on the duration of the conflict. In such an environment, certain debt scheme categories having shorter-duration such as Money Market, Low Duration and Short-Term may offer a blend of relatively higher yields, lower duration risk and potential for gains if yields soften once liquidity normalises.

Sources: RBI, Bloomberg, CMIE and other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.