Geopolitical Volatility - A Structural Opportunity in Indian Equities

Last Updated On: 31 Mar 2026

5 min read

Whats the Point?

- Geopolitical conditions remain fluid, with backchannel diplomacy underway; however, ongoing disruptions in the Strait of Hormuz continue to influence oil prices, pose inflation risks and impact market sentiments.

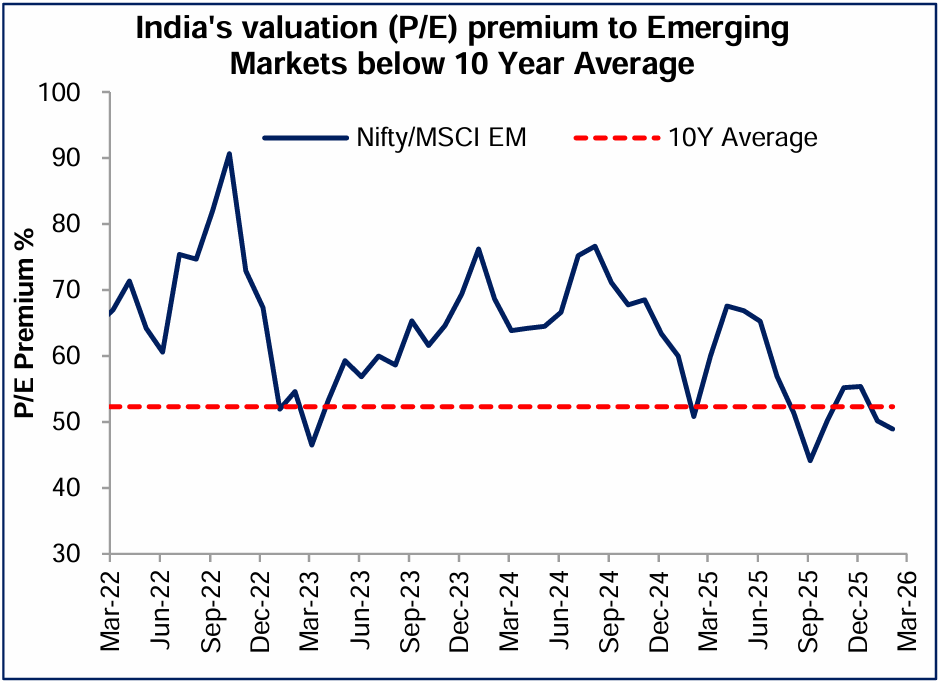

- Risk-off sentiment has weighed on emerging markets, including India, but valuation compression alongside resilient domestic inflows bodes well for the relative attractiveness of Indian equities.

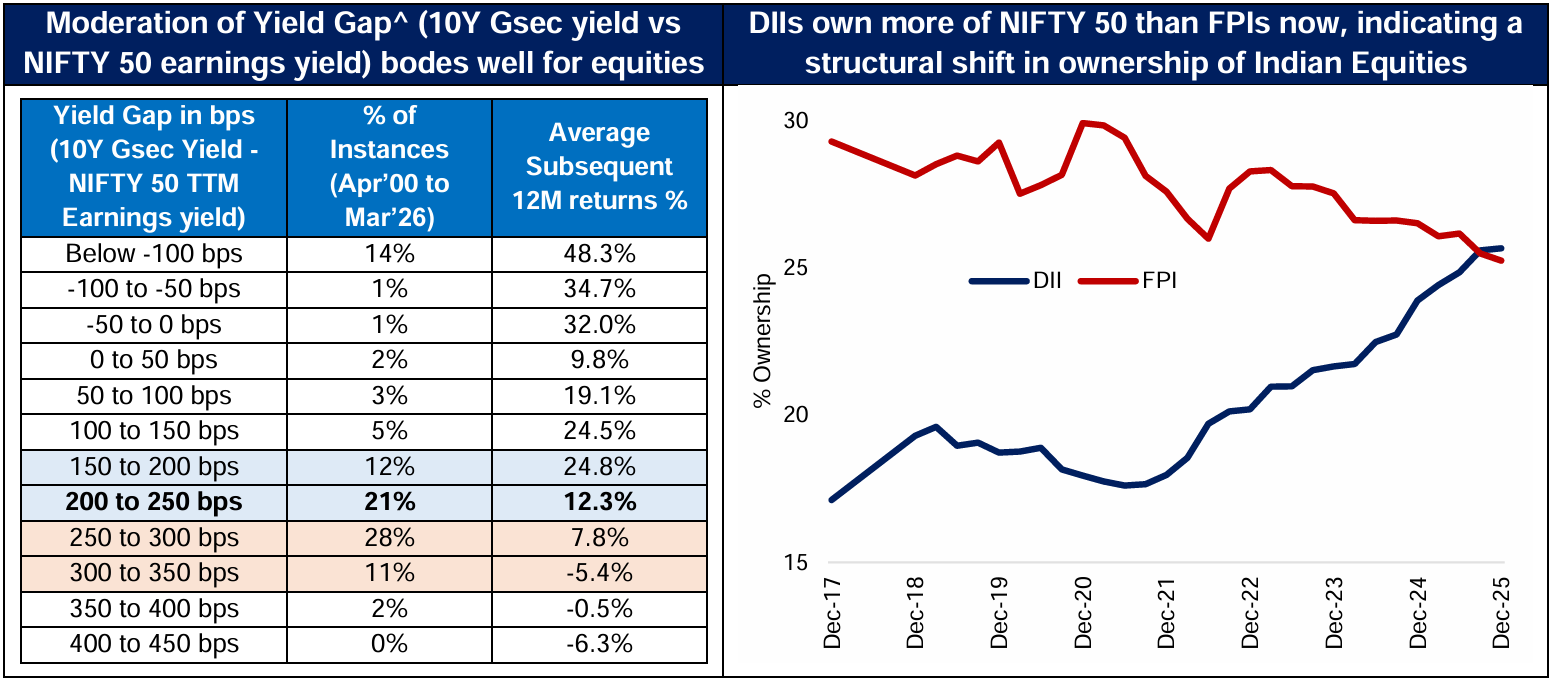

- Moderating valuation indicators, such as the yield gap (10-year G-Sec vs. NIFTY earnings yield) and forward P/E, may provide opportunity to add to investments in a staggered manner with a long-term horizon.

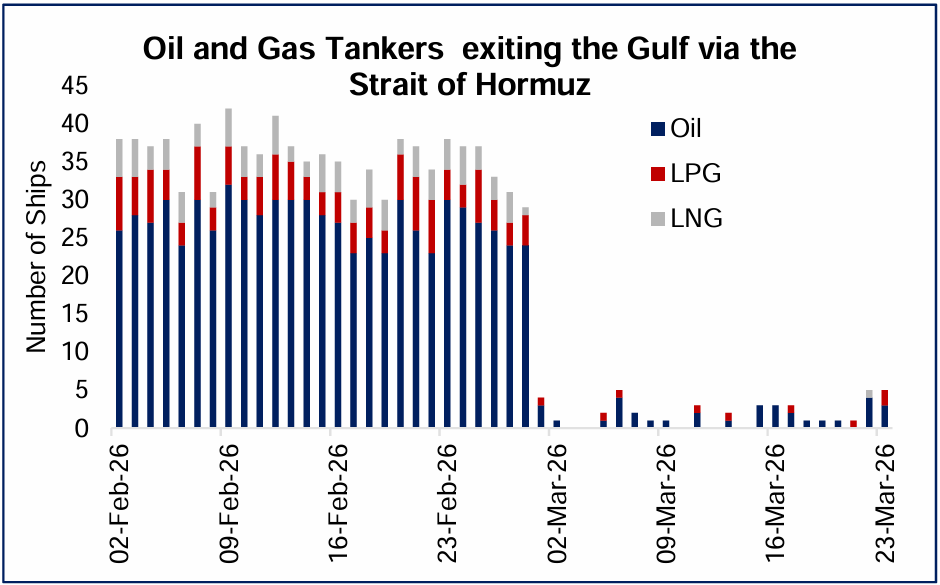

Recently, geopolitical tensions between the US–Israel alliance and Iran have shifted from acute escalation to a more contained, yet uncertain phase. While hostilities persist, there are early, albeit inconclusive, signals of de-escalation through backchannel diplomacy. For now, markets continue to focus on the Strait of Hormuz, a critical conduit for global energy flows, where ongoing disruptions have influenced energy prices and broader risk sentiment. This has weighed on equity markets globally, including India.

Narrow Strait, Wide ranging implications

Global Equities: Risk-Off Dynamics in Play

Indian Equities: Narrowing gap between 10Y Gsec Yield and Earnings Yield

In spite of recent spike in bond yields, the gap between 10-year G-Sec yield and NIFTY 50 Index Earnings Yield (Trailing 12M) has narrowed (225bps as of 25-Mar-2026), reflecting a moderation in equity valuations. Historical data suggests that when this spread approaches lower bands, forward equity returns tend to improve, as the relative attractiveness of equities versus fixed income improves. 1 Year Forward P/E of NIFTY 50 too has moderated sharply from 20.7 as of 31-Dec-25 to 17.3 as of 27-Mar-26 (vs 10 Year Average of 18.7)

Equally noteworthy is the resilience of domestic flows amid ongoing volatility, a trend evident over the past few years. While CYTD 2026 has seen FPI outflows of ~$11 bn, DIIs have remained strong net buyers at ~$24 bn, providing a meaningful counterbalance. Notably, DIIs now hold a higher share in the NIFTY 50 Index than FPIs, marking a structural shift in ownership. This growing domestic participation reduces reliance on foreign capital, enhances market resilience and strengthens the case for renewed foreign inflows once geopolitical headwinds subside.

Conclusion: The current geopolitical environment remains fluid, but a prolonged conflict would carry adverse economic consequences for all parties, increasing the incentive for an eventual resolution. Historically, externally driven market corrections, in the absence of domestic macro weaknesses, have created investment opportunities. With valuations supportive and India relatively attractive versus other EMs, such corrections could offer investors a timely opportunity to add to their investments with a long-term horizon.

Sources: Bloomberg, ^ Avendus Spark, CMIE and other publicly available information.

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.