Structural Shift – India’s Declining Sensitivity to Crude Oil Prices

Last Updated On: 27 Jan 2026

5 min read

What’s the Point?

Crude oil has historically been an important macro variable for India, however, structural changes in the economy have significantly reduced vulnerability to oil price shocks.

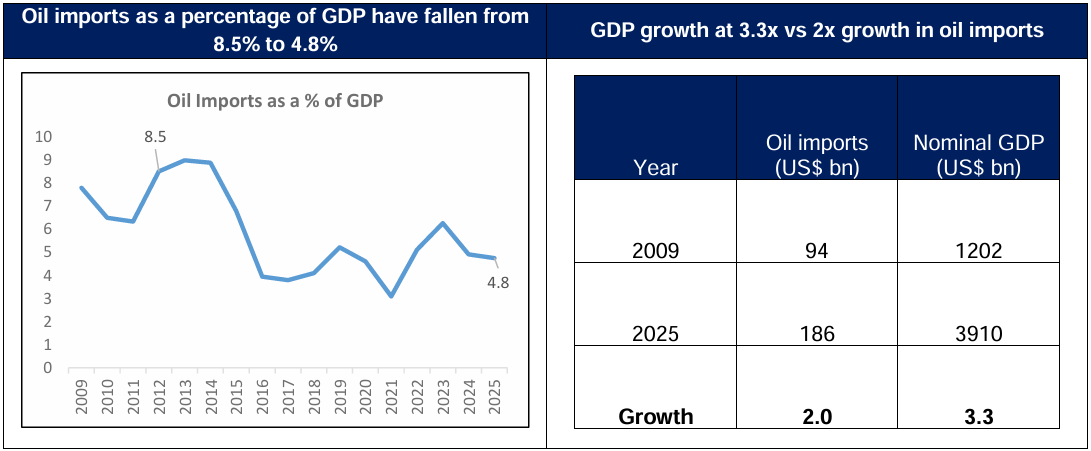

Oil imports as a percentage of GDP have fallen from 8.5% to 4.8% over the years.

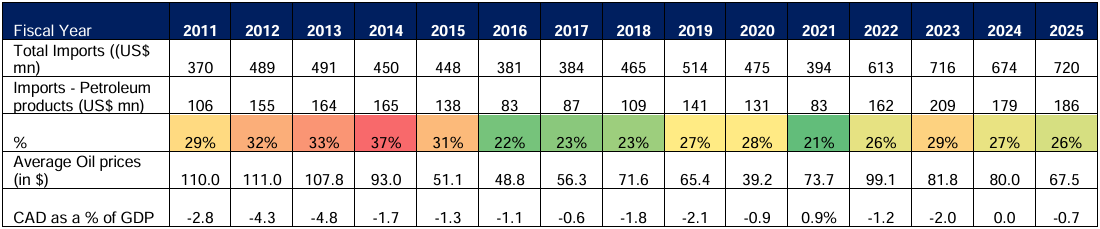

The share of petroleum products in total imports has fallen, with greater diversification into other products, lowering macroeconomic sensitivity to oil volatility.

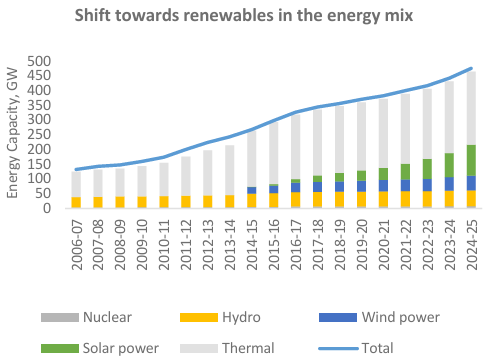

Share of investments in renewables has increased from ~23% in 2013-14 to over 40% in 2024-25.

Reducing sensitivity to crude oil prices is positive for India’s macroeconomic stability and external balance.

Historically, crude oil has been an important macro variable for the Indian economy. As a net importer of oil, India’s growth, inflation, external balance and fiscal dynamics have historically been sensitive to global crude prices. However, over the years, the structure of the Indian economy has evolved meaningfully. Improved energy efficiency, diversification of imports, a rising services sector and policy reforms have reduced the economy’s vulnerability to oil shocks.

India’s Oil Imports as a % of GDP: A Declining Trend

The relative burden of oil imports on the economy has declined over time. Oil imports which accounted for a much larger share of GDP between 2009-14 has seen a sharp decline. Multiple factors have contributed to a gradual reduction in oil imports as a percentage of GDP.

First, the Indian economy has grown faster than oil consumption, led by services and domestic demand. Second, energy efficiency improvements, substitution toward gas and renewables, and better fuel standards have moderated oil intensity. Third, policy measures such as rationalisation of fuel subsidies and market-linked pricing have improved consumption efficiency. As a result, even when crude prices rise temporarily, the macro impact is less severe than in earlier decades.

Changing Composition of Import Basket and Shift towards Renewables

Demand Supply Dynamics

The current global backdrop is supportive of relatively benign oil prices. On the supply side, the US has emerged as a major swing producer over the last decade, significantly altering global oil dynamics. US has expanded its oil output, from a low of about 5 million barrels per day (bpd) in 2008 to over 13 million bpd recently, making it the world’s largest oil producer.

Additionally, recent geopolitical developments between the US and Venezuela could add incremental oil supply over the medium to long term. While Venezuela currently accounts for only ~1% of global oil production, it holds the world’s largest proven oil reserves, estimated at around 300 billion barrels.

On the demand side structural moderation in energy demand growth, driven by electric vehicles, efficiency gains and climate-focused policies, further reduces the risk of sustained oil price inflation. Together, these factors create a favourable environment for oil-importing economies like India.

Conclusion

India’s macroeconomic sensitivity to crude oil has declined meaningfully over time, strengthening its external balance. While India remains a net oil importer, oil imports as a share of GDP and total imports have fallen due to faster GDP growth, improved energy efficiency, diversified import composition. Investments in renewables, alternative energy, electric vehicles and ethanol blending have further reduced oil dependence. In the current global environment of relatively benign oil prices, lower oil import bills help narrow the current account deficit, ease pressure on the rupee, bolster foreign exchange reserves, and helps to provide greater macroeconomic and policy stability.

Sources: CMIE, Bloomberg, Morgan Stanley and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.