Q3 FY26 Earnings - Growth turns broad-based, Small Caps shine!

Last Updated On: 25 Feb 2026

5 min read

What’s the Point?

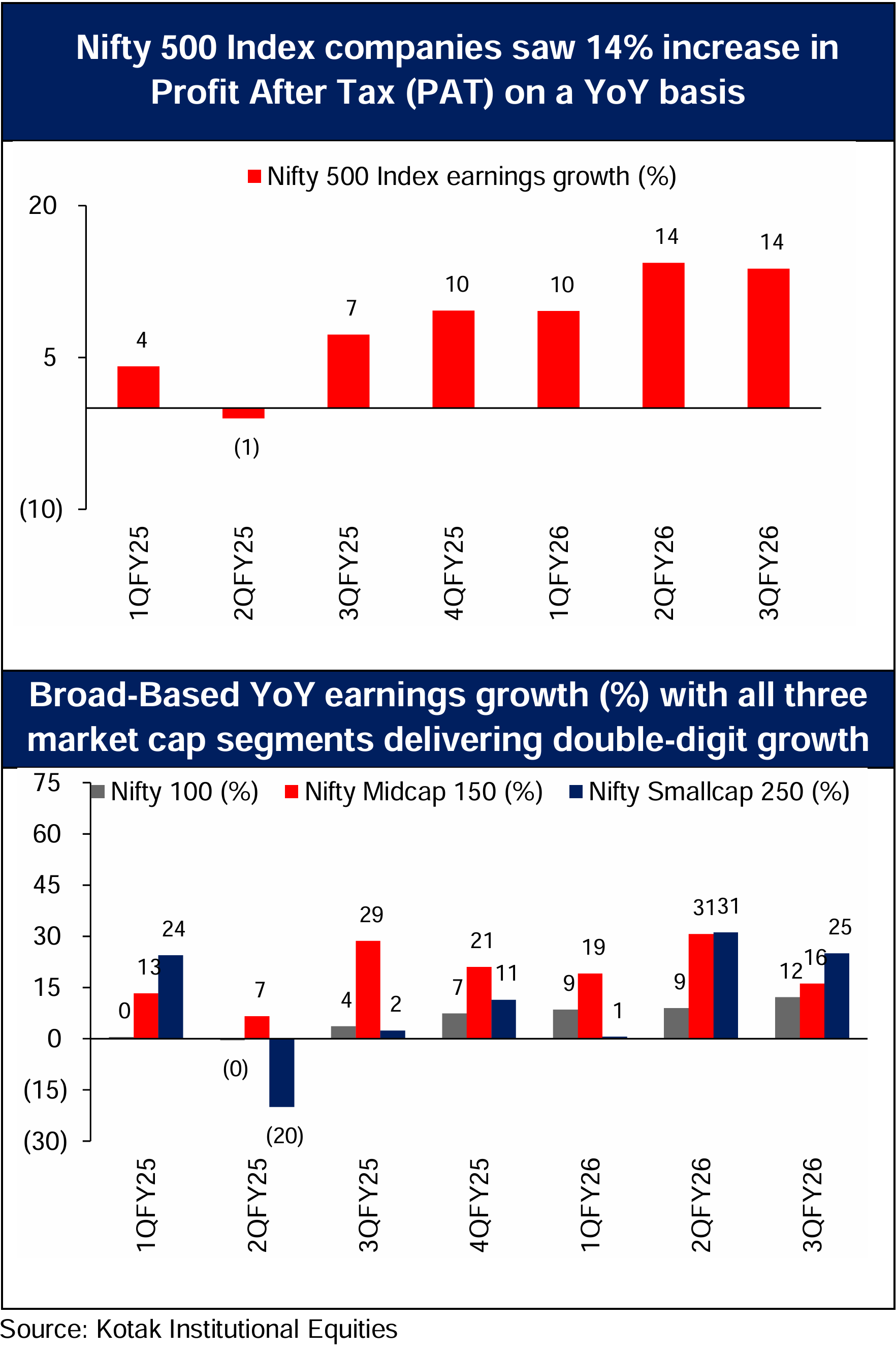

3QFY26 earnings for NIFTY 500 companies grew at 14% YoY.

Earnings growth was well distributed, with 17 out of 29 sectors delivering double-digit YoY profit growth.

All market-cap segments posted double-digit growth, large caps at 12%, mid-caps at 16% and small caps at 25% YoY.

Large-cap profit share in NIFTY 500 has declined from 78% (Q3FY23) to 74% (Q3FY26), highlighting a broadening earnings base.

After a muted FY25, corporate profitability has regained momentum, supported by broad-based performance and improving operating metrics.

Sectoral Snapshot

- Automobiles: The auto segment saw a healthy revival in demand momentum in 3QFY26, with all segments recording double-digit volume growth post a muted 1st half, supported by the festive season and the benefit of the GST rate cut.

- Banks: Improved credit growth and stable asset quality supported earnings; PSU banks outperformed, while private banks saw gradual normalization after margin pressures.

- Metals & Mining: Earnings upgrades continued in 3QFY26, aided by firm commodity prices and operating leverage; sector has been a key outperformer and a meaningful contributor to incremental profits.

- Oil & Gas: Strong earnings led by upstream and downstream oil and gas companies, supported by gas pricing, stable crude prices.

- Cement: The sector saw a strong volume growth; however, realizations were weak. Lower fuel & power costs were unable to offset the impact of weak realizations, leading to lower profitability.

- Healthcare: Growth remained mixed in 3QFY26, with strong domestic formulation sales offsetting weak US generic sales.

- Telecom: 3QFY26 was a steady quarter for telecom companies. The growth was primarily driven by higher average revenue per units (ARPUs) led largely by subscriber mix improvements.

- IT - IT services companies reported better-than-feared earnings, with management commentary remaining constructive on discretionary spending and early AI-led demand. However, broader sector sentiment turned cautious, influenced by commentary from AI-native players highlighting faster productivity gains, shorter implementation cycles, and potential disruption across application development, testing and ERP implementations.

- Consumer Staples - Key government initiatives are driving the consumption recovery. Milder inflation, improved affordability after the recent GST rate rationalization, and falling interest rates are driving rural/urban consumption catalysts.

- Utilities: Sustained weak demand weighs on earnings due to weather related disruptions.

Conclusion: Strengthening Equity Outlook

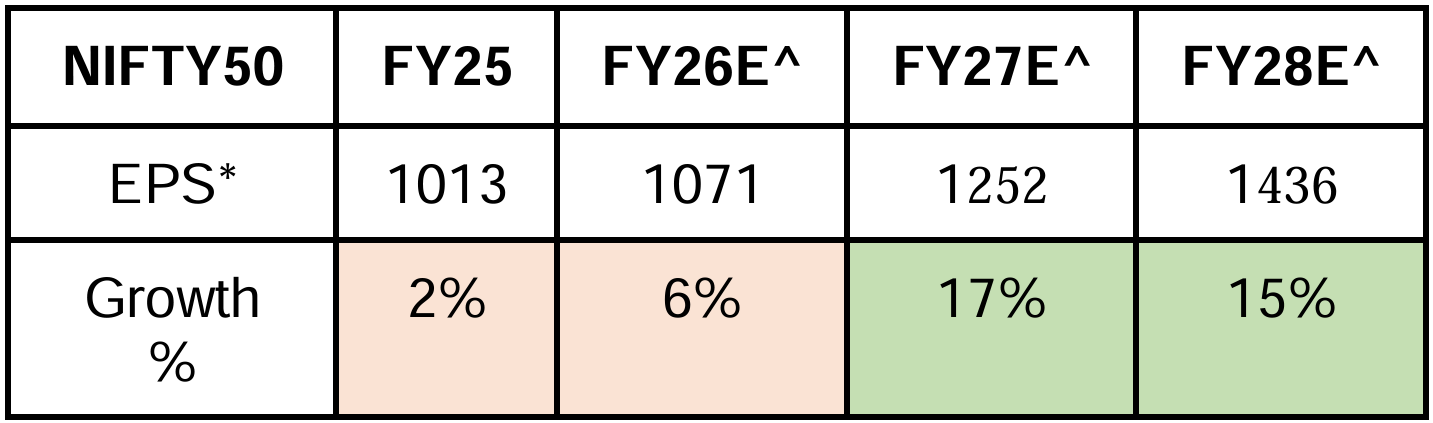

*Earnings Per Share, Sources: Bloomberg, ^ Kotak Institutional Equities

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.