Domestic Growth Momentum Builds, yet an India-US Trade Deal remains key

Last Updated On: 25 Nov 2025

5 min read

What’s the Point?

- Recently, Indian PSU oil companies have successfully concluded a 1-year structured contract to import around 2.2 million tonnes per annum of Liquified Petroleum Gas (LPG) from the US Gulf Coast for the contract year 2026. This represents close to 10% of India’s annual LPG imports and marks the first such structured US LPG contract for the Indian market.

- In October 2025, India’s trade deficit widened by 29.6% to nearly US$42 billion vs September 2025 on account of total exports dropping by 5.5% and total imports increasing by 11% during October 2025. As per reports, India’s Current Account Deficit (CAD), which currently stands at 0.2% of GDP (June 2025), is expected to rise to 1.7% of GDP for FY26 due to the tariff pressures that continue to keep the trade deficit elevated.

- Against this backdrop, the structuring of such a contract is very important. While India’s structural drivers of growth remain sound and has potential to weather the pressures of tariffs imposed by the US Government, a trade deal with India and US will support India’s stronger economic growth.

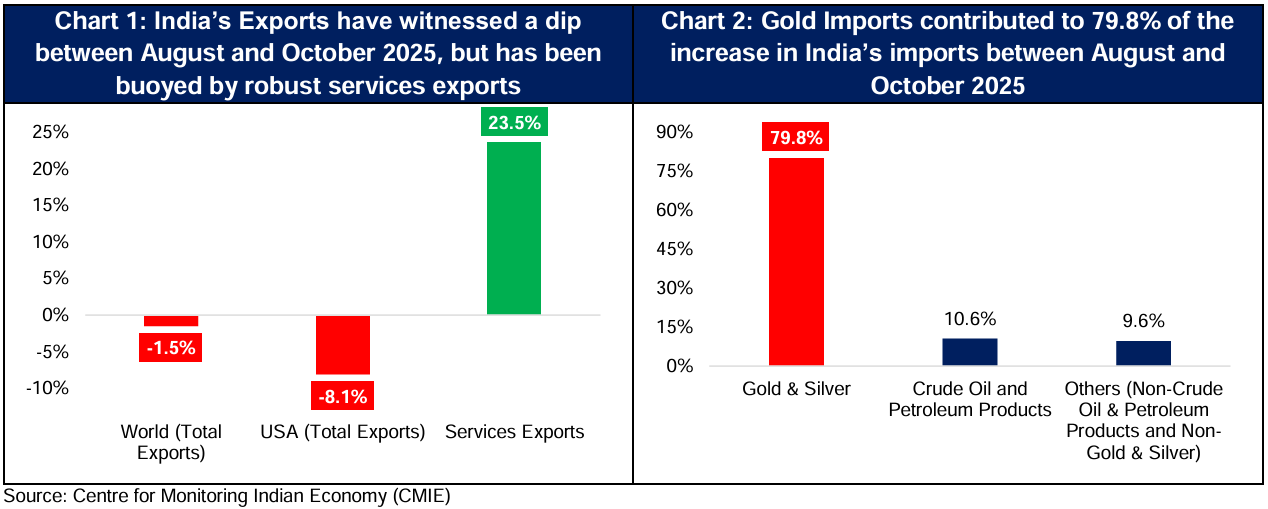

Trade Balance – A Wider, but Manageable Deficit

Exports – On August 06, 2025, the US Government imposed an additional 25% tariff on India, raising the total effective tariff rate to 50%. This higher tariff took effect from August 27, 2025 and was linked to India’s continued imports of Russian oil. In the two full months after the tariff came into force, India’s total exports slipped 1.5% in October compared to August levels, as a result of exports specifically to the US falling by 8.1% during the same period. (Please refer to Chart 1 below).

Imports – Between August 2025 and October 2025, India’s total imports rose significantly by 23.5%, reaching US$76 billion. Notably, 79.8% of this increase was driven by a surge in gold and silver imports, which doubled (2x) over this period. The spike was largely due to festive buying, the start of the wedding season, and a cautious external environment. (Please refer to Chart 2 below).

Although India’s goods trade deficit has widened, the overall trade deficit has stayed relatively contained because services exports have grown strongly. Between August 2025 and October 2025, services exports rose by 23.5% to US$19.8 billion. On the imports side, there is likely to be some relief ahead, as gold and silver imports should decline after the wedding season ends.

Government has taken several GDP-supportive initiatives to offset the Impact of Tariffs

The first 3 quarters of FY25 saw India’s GDP growth being lower than the forecasts by RBI due to a slow pick-up in urban consumption. While higher GDP growth in Q4FY25 lifted the overall growth for FY25, this improvement came from the fillip to consumption during the Maha Kumbh Festival in January and February 2025. Since the new US administration took office in 2025, the Indian Government had been pre-empting the eventual imposition of tariffs on India. Hence, in a bid to support a stronger economic growth, the Government has intervened through measures on fiscal and monetary sides.

On the fiscal side, it conducted one of the most significant tax reforms in recent times, with the Goods and Services Tax (GST) Council delivering a much-awaited GST overhaul effective from September 22, 2025. The earlier four-slab system and Compensation Cess gave way to a new two-slab structure of 5% and 18%, with a demerit rate of 40% for luxury and sin goods. While the effects of this reform is yet to show its full impact, it has already started to show positive signs on a key high-frequency indicator – automobile registrations, with the Navratri to Diwali window recording the strongest-ever registrations. During this window, 33.57 lakh units – 17% higher than 2024 – were registered supported by GST reforms laid ahead of the festive season.

On the monetary side, RBI has cut the Repo Rate by 75 bps (basis points) – 25 bps in February 2025 and 50 bps in June 2025. Lower interest rates, in addition to targeted tax rebates, GST rationalization and improved liquidity in the system are slowly helping in reviving another high-frequency indicator – credit demand, with system credit demand, especially retail credit demand, witnessing an improvement. (Covered in our recently-published Tuesday’s Talking Point: Credit Growth and Valuations Align for Private Banks).

GDP = Consumption + Government Expenditure + Investments + Exports – Imports

As per the equation, it can be understood that the tariffs imposed by the US Government has led to softer exports, thereby creating a downward pressure on India’s GDP. However, the Government’s interventions are providing support in offsetting some of that impact through higher consumption in the economy.

Key Takeaway: Government measures have provided an impetus to high-frequency indicators, signalling early stabilisation in domestic demand. These interventions are helping cushion the impact of softer exports and a wider trade deficit brought on by elevated tariffs. However, while these domestic efforts provide near-term support, neutralising the external pressures would require a comprehensive India-US trade deal, which remains critical to unlock higher stability and create a stronger platform for India’s stronger economic growth.

Sources: CMIE, RBI, Bloomberg and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.