Market Review - May 2026

Last Updated On: 11 Jun 2026

Macroeconomic Update

Macroeconomic Update Debt Market Update

Debt Market Update Equity Market Update

Equity Market Update

Macroeconomic Update

During the month, geo-political tensions remained elevated as resolution of conflict between US and Iran remained elusive, and Strait of Hormuz remained practically shut disrupting supply of oil and other commodities. Despite elevated uncertainty growth in US remained robust and labour markets continue to show resilience with three-month average non farm payroll now at its strongest since March 2024. However, the ongoing war is beginning to weigh on consumer sentiments in the US, as rising fuel costs continue to drive inflation. In Europe, business activity has contracted, with manufacturers struggling against supply constraints and escalating input costs. Manufacturing activity in China stayed just above the expansion threshold but remains pressured by weak domestic demand.

Inflation rose across regions in May 2026 due to higher energy costs and is expected to rise further as supply remains constrained.

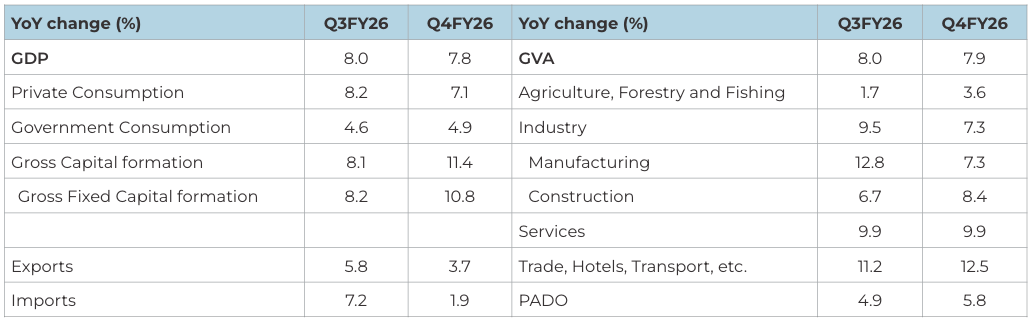

India Q4FY26 GDP was higher than expectations: India's GDP growth was recorded at 7.8% YoY in Q4FY26 which was above consensus expectations. The growth in Q4 was driven mainly by robust investment demand even as private consumption growth decelerated. On the supply side higher growth was supported by strong services sector growth and acceleration in construction and agricultural activity even as growth manufacturing decelerated. Within services, Trade, Hotel, Transport and Communication recorded double digit growth for third quarter in a row.

Source- MoSPI. Note- PADO: Public Administration and Defence

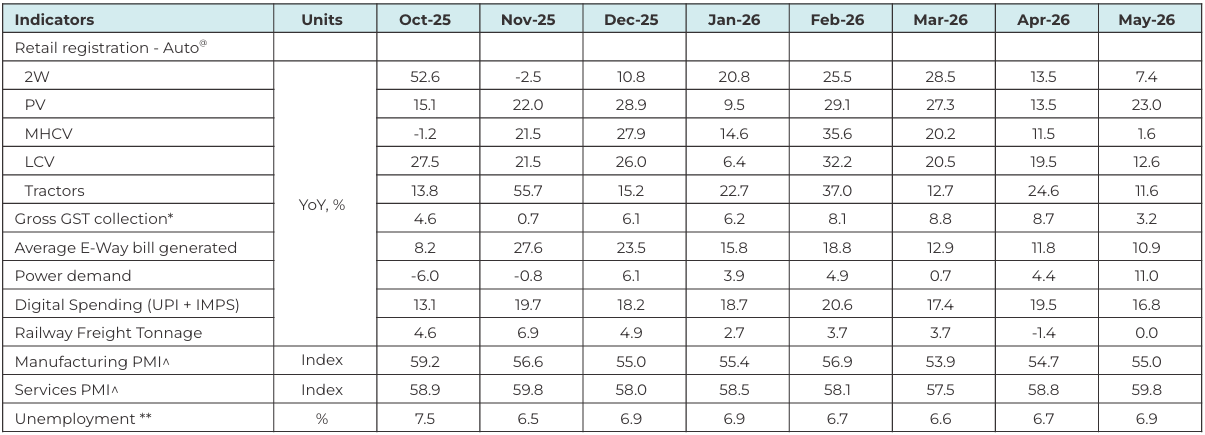

Economic activity in India remained resilient in May: The high frequency indicators for May 2026 suggest that economic activity continue to hold up well despite the ongoing conflict and resultant supply chain disruption. Both manufacturing and services activity recorded better growth in May 2026 compared to April 2026 alongside continued strong growth in vehicle registrations and a robust power demand. GST collections growth moderated in May, but this was driven by a high base during May 2025 which included Rs100 billion of one-time telecom spectrum payment. Adjusting for that one time payment, growth in GST collections was 9% YoY in May 2026.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, www.vaahan.parivahan.gov.in, www.posoco.in

^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. *GST collections for the month is for economic activity in the previous month. ** based on CMIE survey

Going forward, growth is likely to remain steady which may be supported by continued momentum. However, strength and direction of growth momentum will depend on how quickly the conflict in West Asia is resolved and supply chain restored to pre-war levels. The prospects of lower-than-expected south-west monsoon is also likely to adversely affect agriculture production and rural demand this year.

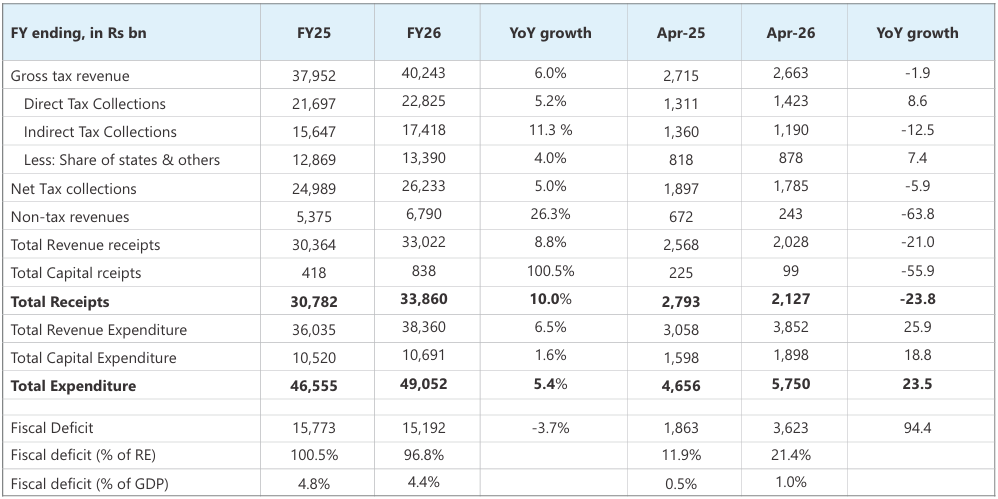

Govt expenditure growth starts on a strong footing: The Government was able to contain the FY26 fiscal deficit to 4.4% of GDP as per the revised estimates. The capital expenditure in FY26 grew at 1.6% YoY, lower than revised estimates of 4.2% YoY. The first month of FY27 (April 2026) has seen strong expenditure momentum in both revex and capex. However, tax revenue growth contracted in April dragged down by weaker indirect tax collections even as direct tax collection growth was strong.

Source: CMIE Note: YoY: Year on year growth

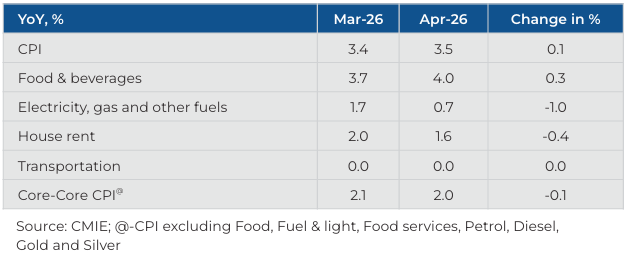

CPI inflation inched up in April 2026: CPI inflation rose slightly in April but remained contained as the Government shielded consumers from the rising crude oil prices by keeping retail prices of petrol and diesel unchanged during the month. Food inflation continued to rise driven by higher edible oil and meat prices and was recorded at 14 months high in April. Core inflation (ex of precious metals) continue to remain benign.

Going forward, inflation is likely to inch up in FY27 on adverse base effect, higher commodity prices and a prospect of a below normal monsoon but is likely to be within the RBI's tolerance band. The geo-political situation in West Asia and monsoon progress remains a key monitorable from an inflation perspective.

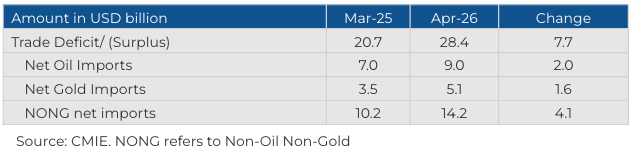

Trade deficit increased in April 2026: Trade deficit rose in April driven mainly by non-oil-non-gold imports, although net gold and net gold imports were also higher during the month. Non-oil-non-gold imports growth was driven by electronic and machinery imports. Going forward, trade deficit is likely to be under pressure if the ongoing conflict in the West Asia gets elongated. However, healthy growth in services exports is likely to keep CAD within manageable limits.

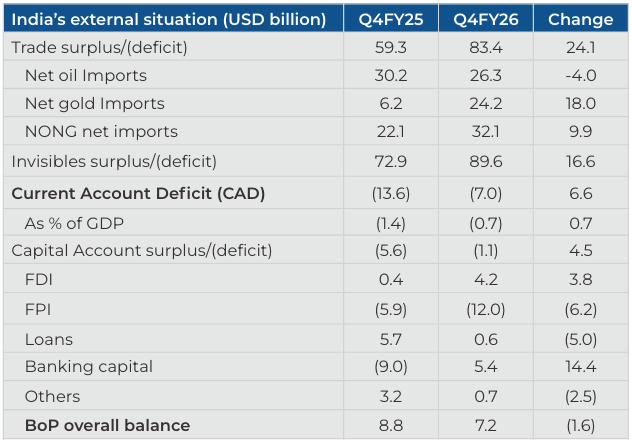

Current account turns surplus in Q4FY26: Q4FY26 current account recorded a surplus of 0.7% of GDP compared to a surplus of 1.4% of GDP in Q4FY25 due to widening of goods trade deficit. On the other hand, Capital account recorded a deficit of USD1.1 billion in Q4FY26 compared to a deficit of USD5.6 billion in Q4FY25.

In its latest monetary policy review, the RBI announced a series of measures to attract capital flows which should help ease pressure on the INR and reinforce external stability. These include.

- Expanding the universe for Government securities to include all new issuances of 15, 30 and 40 years maturity under the Fully Accessible Route (FAR). Additionally, FPI limits on short-term investments under the general route have been removed.

- Government approved tax benefits by withdrawing capital gains and withholding tax on returns from investments in G secs .

- Increased limits for investment by NRIs and OCIs in equity market without SEBI registration and extending it to all individual Persons Resident Outside India (PROIs) at par with NRIs and OCIs.

- Allowed concessional forex swap till 30th September 2026 to incentivize External Commercial Borrowings by Public Sector Undertakings

- RBI to bear the full hedging cost till 30th September 2026 for raising fresh 3–5-year FCNR (B) deposits by Authorized Dealers/Banks

- Restored the time for realisation of export proceeds to nine months (from 15 months earlier).

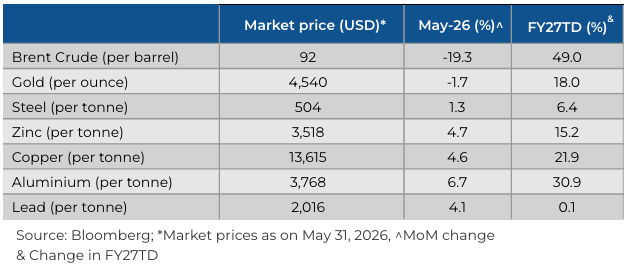

Commodity prices remain elevated: Crude oil prices declined in May'26 as ceasefire optimism between the U.S. and Iran raised hopes of reopening the Strait of Hormuz. However, most commodity prices, especially industrial metals, remain elevated as supply chains remain disrupted due to ongoing conflict and rising demand for new-age technologies, such as EVs and data centres.

Summary and Conclusion:

Global economy faces heightened uncertainty due to geo-political tensions in West Asia. If the conflict gets elongated, it can have profound implications for the global economy as not only energy but supply chains for various sectors will get disrupted. Growth in the US so far has held up well on the back of AI/tech related capex and higher Government spending. Recent data also point towards robust labour markets conditions in US. Growth in China is following a two-speed path where domestic consumption, investments and property markets are in a slow lane, but exports and manufacturing are holding up well.

Before the start of conflict in West Asia, growth in India too had held up well on the back of fiscal (income tax and GST cuts) and monetary (lowering of interest rates) stimulus. High frequency indicators have steadily improved over the last few months with rural demand continuing to hold up well and urban demand too showing signs of uptick. High frequency data since the start of the conflict also points towards continued resilience in the economy. Inflation remains well anchored and though it's expected to rise from here on due to rise in crude oil and other commodity prices, and adverse base effect, it's unlikely to increase significantly. RBI has projected an average inflation of 5.1% in FY27 (albeit with upside risks).

Looking ahead, the medium-term outlook for the Indian economy seems optimistic, in our view. This optimism is driven by steps taken by RBI and Government, opportunities arising from shift in the global supply chain, momentum of private consumption sustaining due to income tax relief and lower borrowing cost. However, the flare up in geo-political tensions remains a key risk to growth this year as supply shock risks lowering growth and increasing inflation.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.