Market Review - June 2026

Last Updated On: 10 Jul 2026

5 min read

Macroeconomic Update

Macroeconomic Update Debt Market Update

Debt Market Update Equity Market Update

Equity Market Update

Macroeconomic Update

Jun'26 marked a significant breakthrough in the West Asia conflict, with the US and Iran signing a 14-point memorandum that brought a temporary pause to hostilities and effectively reopened the Strait of Hormuz. As commodity prices, particularly crude oil, declined, US consumer sentiment improved. Growth in US continue to hold up well driven by strong AI/tech related investment demand and even though non-farm payroll was lower than expected in June, the labour markets remain resilient with unemployment rate declining marginally. In Europe, the business activity returned to expansionary territory as easing commodity prices helped reduce input cost pressures. China witnessed another strong month of exports driven by AI hardware even as domestic demand and property investments continue to remain subdued.

US CPI inflation hit 4.2%YoY in May'26 (highest since April-23), driven mainly by a spike in energy costs due to West Asia conflict. Core CPI too remained elevated at 2.8% YoY. In Jun'26 meeting Fed remained on hold although with a hawkish pivot as 9 of 18 officials expect at least one rate hike by end of 2026, a reversal from March's projections, which had shown a median forecast of one rate cut for 2026. ECB and BoJ both hiked policy rate by 25bps in June as inflation rose on the back of higher energy prices.

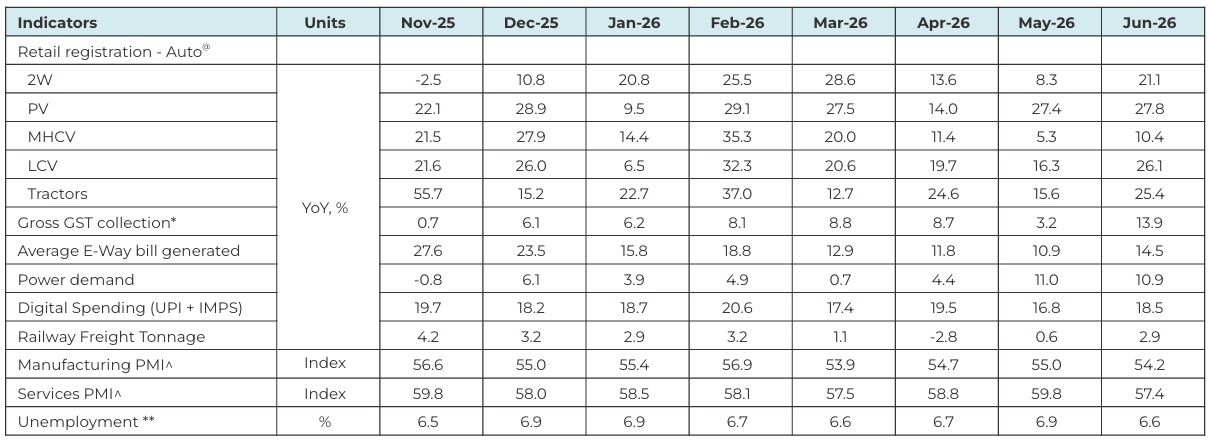

Economic activity in India remained resilient in June 2026: The high frequency indicators for June suggest that economic activity continue to hold up well. Vehicle registrations and power demand recorded another month of strong growth, along with sharp pick-up in GST collections and e-way bill generation. Manufacturing and services PMI moderated in June compared to May but remain firmly in expansion zone.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, www.vaahan.parivahan.gov.in, www.posoco.in

*GST collections for the month is for economic activity in the previous month. ^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. ** based on CMIE survey

Going forward, growth is likely to remain steady which is likely to be supported by continued momentum. Ceasefire between US and Iran and resultant restoration of supply chains bode well from growth perspective. The prospects of lower-than expected south-west monsoon, however, is likely to adversely affect agriculture production and rural demand this year.

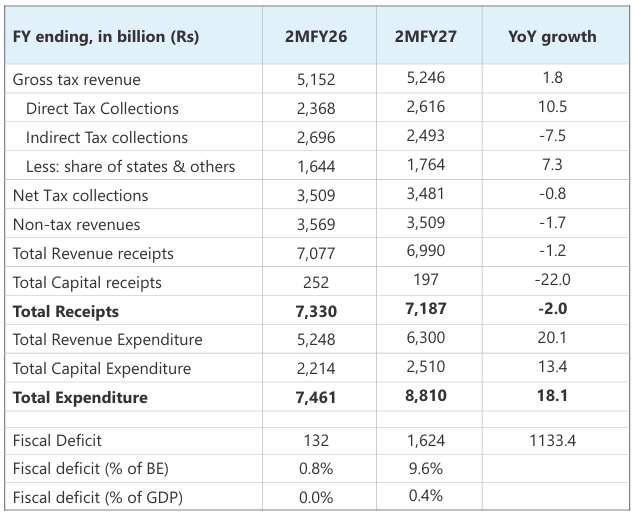

Government expenditure growth on a strong footing: Total Government expenditure has grown by 18.1% YoY in 2MFY27 driven by both revex and capex. Tax collections growth, however, remain muted dragged down by GST collections growth (as GST rates were reduced in September 2025) even as direct tax collection growth has been decent. A combination of higher expenditure and lower tax collections growth has meant that fiscal deficit has expanded compared to the same period last year. Fall in fertilizer and crude oil prices bode well from fiscal deficit perspective and any minor shortfall in revenue can be met through economic stabilisation fund and/or expenditure rationalisation.

Source: CMIE Note: YoY: Year on year growth

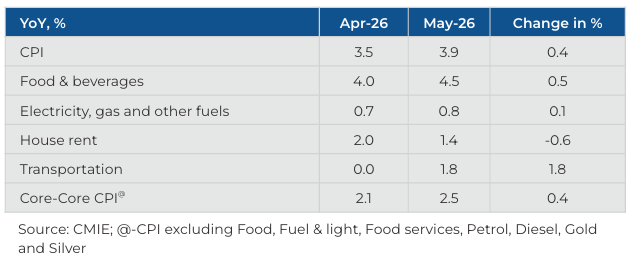

CPI inflation inched up in May 2026: CPI inflation rose in May but remained contained and was below market expectations. The rise in inflation was driven by food and transport segment. While inflation in transport segment was driven by higher retail prices of petrol and diesel, food inflation rose primarily due to rise in vegetable prices. Core inflation excluding precious metals also rose by 40bps due to rise in various goods and services but remains benign.

Going forward, inflation is likely to inch up in FY27 on adverse base effect, and a prospect of a below normal monsoon but is likely to be within the RBI's tolerance band. The geo-political situation and monsoon progress remains a key monitorable from an inflation perspective.

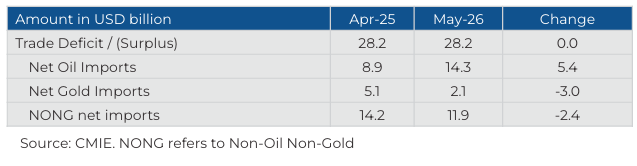

Trade deficit remained unchanged in May 2026: Trade deficit remained steady in May as increase in net oil imports was offset by a fall in net gold and net non-oil, non- gold imports. Going forward, upward pressure on trade deficit is likely to ease as ceasefire between US and Iran is likely to result in lower crude and other commodity prices. Moreover, healthy growth in services exports will help keep CAD within manageable levels.

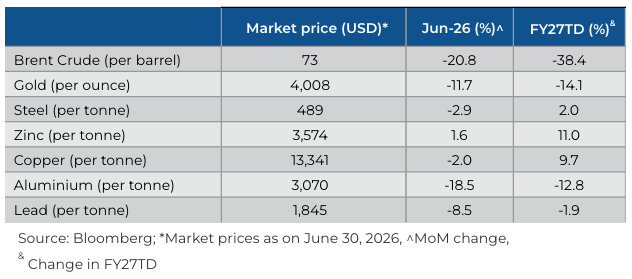

Commodity fall in June 2026: Crude oil prices declined significantly in Jun-26 following ceasefire between US and Iran and opening of Strait of Hormuz. The easing of geo political tensions also led to fall in most commodity prices during the month.

Summary and Conclusion:

The breakthrough in West-Asia conflict is a huge positive for global supply chains, which were disrupted by the blockade of Strait of Hormuz. The resultant fall in crude oil and other commodity prices bode well for both growth and inflation dynamics for the global economy. Growth in the US so far has held up well on the back of AI/tech related capex and higher Government spending. Recent data also point towards resilient labour markets conditions in US. Growth in China is following a two-speed path where domestic consumption, investments and property markets are in a slow lane, but exports and manufacturing are holding up well.

Contrary to expectations, growth in India held up remarkably well despite disruptions caused by West Asia crisis. High frequency indicators have steadily improved over the last few months with rural demand continuing to hold up well and urban demand too showing signs of uptick. Inflation remains well anchored and though it's expected to rise from here on due to adverse base effects and deficient monsoon, it's unlikely to increase significantly. RBI has projected an average inflation of 5.1% in FY27.

Looking ahead, the medium-term outlook for the Indian economy seems optimistic, in our view. This optimism is driven by steps taken by RBI and Government, opportunities arising from shift in the global supply chain, momentum of private consumption sustaining due to income tax relief and lower borrowing cost. However, resumption of hostilities between US and Iran and significantly below normal monsoon remain key risks to growth this year.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.