SIP + EMI: A Smarter Way to Think About Your Loans?

Last Updated On: 9 Jun 2026

Assume you have taken a ₹50 lakh home loan in April 2006.

You opted for a 15-year loan tenure.

Your monthly

EMI for this loan was ₹50,713*.

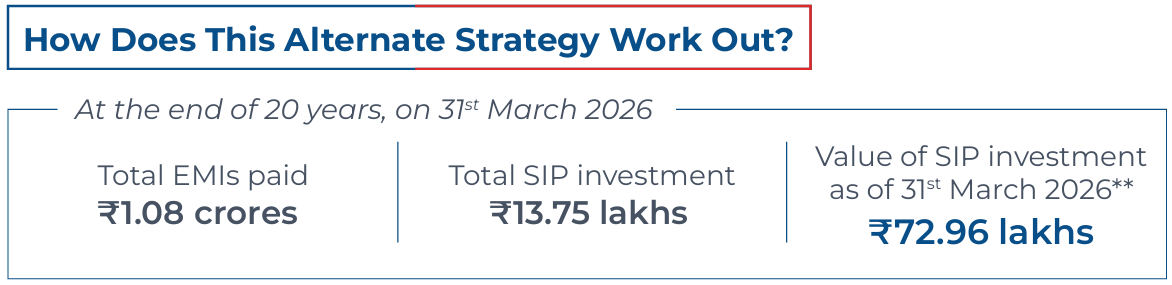

Over the full tenure, you repaid a total of ₹91.28 lakhs.

This means the loan was completely closed at the end of the

15-year period.

This is the traditional route, pay a higher EMI, finish the loan sooner, and save on interest.

*Interest Rate of 9% p.a considered#

Now, let’s explore a different strategy.

You revised the loan tenure to 20 years.

Your new monthly EMI was ₹44,986*, resulting in monthly savings of ₹5,727.

Instead of using this surplus for expenses, you invested the ₹5,727 every month through an SIP.

You decide to invest the EMI difference (₹5,727) every month into HDFC Flexi Cap Fund, starting 1st April 2006.

*Interest Rate of 9% p.a considered#

Source:MFI Explorer

**Regular-Growth Plan was considered for the HDFC Flexi Cap Fund. Assuming SIPs were executed on the 1st of every month from April 2006 to March 2026. Past performance may or may not be sustained in future and is not a guarantee of any future returns.

#Effects of taxation have not been considered in the above illustration. The above calculations are for illustrative and educational purposes only and hence the rate of interest is assumed for ease of understanding of the readers. These rates fluctuate as per market conditions. These are not indicative / assuring of any future returns. Past performance may or may not be sustained in future and is not a guarantee of any future returns.

This illustration shows how combining SIPs with EMIs can potentially create long term wealth. While you might pay more interest over time, disciplined investing can help offset this and may even build a decent corpus.

Of course, every individual’s situation is unique. The right approach depends on your comfort with EMIs, investment discipline, and long term financial goals.

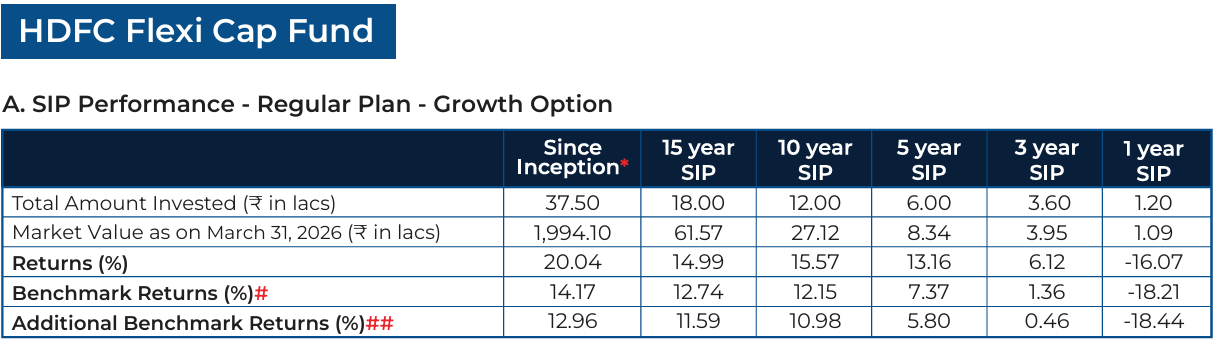

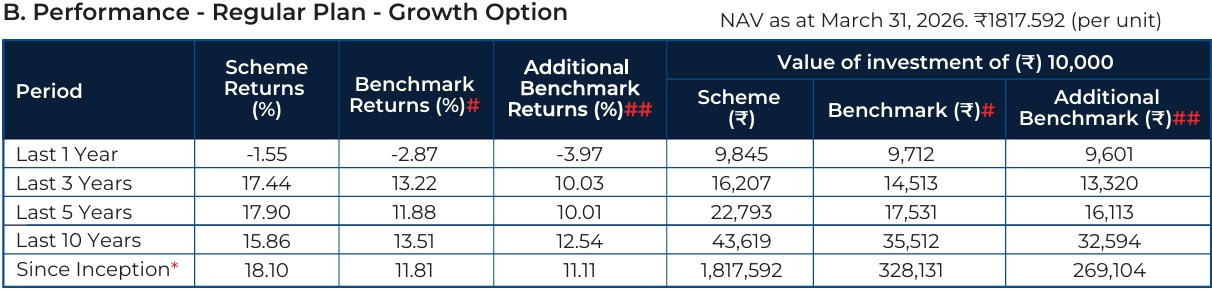

Assuming ₹10,000 invested systematically on the first Business Day of every month over a period of time. CAGR returns are computed after accounting for the cash flow by using XIRR method (investment internal rate of return) for Regular Plan - Growth Option. The above investment simulation is for illustrative purposes only and should not be construed as a promise on minimum returns and safeguard of capital. SIP - Systematic Investment Plan

Common notes for the above table A & B: Past performance may or may not be sustained in future and is not a guarantee of any future returns. *Inception Date: January 1, 1995. The scheme is managed by Mr. Amit Ganatra since February 01, 2026. # NIFTY 500 Index (TRI). ## Nifty 50 Index (TRI). The above returns are of Regular Plan – Growth Option. Returns greater than 1 year period are compounded annualized (CAGR). Load is not taken into consideration for computation of performance. Different Plans viz. Regular Plan and Direct Plan have a different expense structure. The expenses of the Direct Plan under the Scheme will be lower to the extent of the distribution expenses / commission charged in the Regular Plan. As NIFTY 50 TRI data is not available since inception of the scheme, additional benchmark performance is calculated using composite CAGR of NIFTY 50 PRI values from January 1, 1995 to June 29, 1999 and TRI values since June 30, 1999. Above returns are as on March 31, 2026.

Benchmark and Additional Benchmark performance is computed as on 30th March, 2026, since values for 31st March 2026 are not available.

For performance of other funds managed by fund manager, Please click here.

Views expressed above are indicative and should not be construed as investment advice or as a substitute for financial planning.

Due to the personal nature of investments, investors are advised to seek professional advice before investing.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.