Q4FY26 Earnings: Mid Caps have outpaced Large and Small Caps, but…

Last Updated On: 9 Jun 2026

5 min read

What’s the Point?

- Broad-Based Earnings Season: NIFTY 500 Index posted 14.3% Year-over-Year (YoY) earnings growth in Q4FY26. Breadth improved, with 21 of 29 sectors recording double-digit YoY earnings growth vs 17 in Q4FY25.

- Multiple Levers across Sectors: YoY growth was supported by a mix of tailwinds – policy support via GST 2.0 cuts and State Government measures (Auto & Auto Components, Consumer Staples), healthy volume growth and stronger realizations (Metals & Mining), healthier asset quality for Banks and higher loan book growth for Non Banking Financial Companies (NBFCs), strong growth in domestic formulations and sharp revival in diagnostics (Pharma & Healthcare), and steady electricity demand (Utilities).

- West Asia Conflict: NIFTY 50 Index Earnings per Share (EPS) is expected to grow faster (double-digit forecast) in FY27. However, the uncertainty about the duration and intensity of the conflict, magnitude of its spill over effects and the pace of restoration of supply chains remains the common watch-point for Q1FY27 risk.

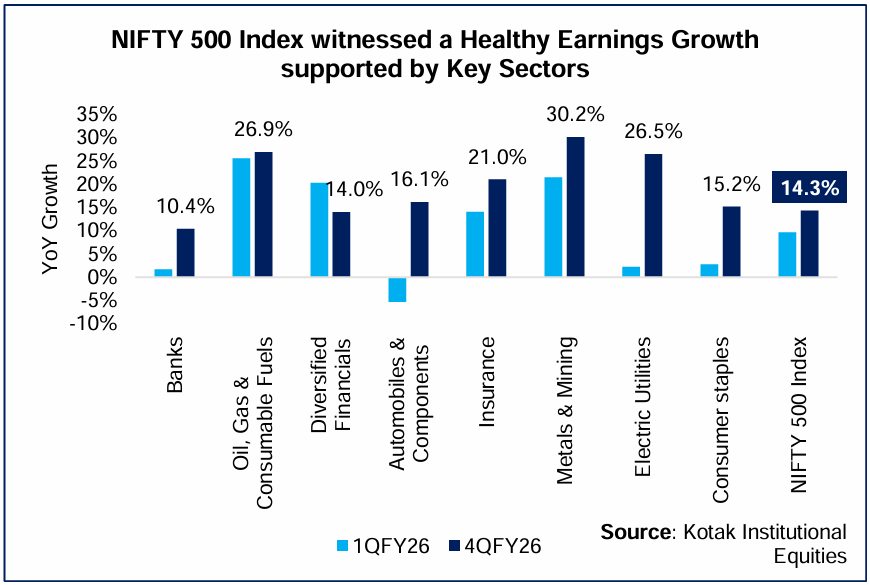

Q4FY26 YoY Earnings Growth: More Broad-Based compared to Q4FY25

The Q4FY26 earnings season delivered a healthy performance, with NIFTY 500 companies posting a robust 14.3% YoY earnings growth. Some of the key sectors driving this growth were Auto & Auto Components, Consumer Staples, Banks, Oil & Gas, Metals & Mining, Diversified Financials and Insurance.

The earnings growth in Q4FY26 was broad based than Q4FY25, with 21 sectors (out of 29) reporting double-digit YoY earnings growth at the end of the previous fiscal year compared to 17 sectors (out of 29) for Q4FY25. Furthermore, only 3 sectors reported single-digit earnings growth (YoY) compared to 5 reported in Q4FY25.

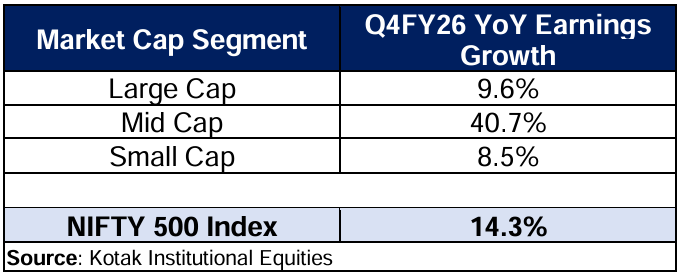

Market Cap Level Earnings Growth: Mid Caps have outpaced Large and Small Caps

While NIFTY Smallcap 250 Index and NIFTY 100 Index posted 8.5% YoY and 9.6% YoY earnings growth in Q4FY26, NIFTY Midcap 150 Index delivered a strong double-digit YoY earnings growth of 40.7%. The growth in the Mid Cap segment was supported by companies belonging to sectors like Banks (Mid-size), Auto & Auto Components, Electrical Utilities, Diversified Financials and Real Estate.

Between Q4FY22 and Q4FY24, the contribution of Large Caps to the profit pool of NIFTY 500 Index saw an increase of 2.4%, with Mid and Small Caps witnessing a decline. However, since Q4FY24, the contribution of Large Caps has been tapering, driven by the outperformance of Mid Caps. In FY26, the decline in contribution of Large Caps became even sharper – 3.3% decline between Q4FY25 and Q4FY26 – with the Mid Cap profit pool share increasing sharply by 3.7% during the same period.

Source: Kotak Institutional Equities; *NIFTY 100 Index, **NIFTY Midcap 150 Index, @NIFTY Smallcap 250 Index

Sectoral Snapshot

- Banks: Loan growth improved both Quarter-over-Quarter (QoQ) and YoY, driven by Corporate and Small and Medium Enterprises (SME). The biggest surprise was on benign asset quality across Private and PSU Banks. While Banks saw an improvement in margins on YoY basis, margin pressures continue to prevail with a low single-digit growth witnessed between Q3 and Q4FY26 on a QoQ basis. This relatively flat growth has been due to repricing of deposits taking more time.

- Diversified Financials: In addition to Q4 being a seasonally strong quarter for NBFCs, loan growth remains strong along with Net Interest Margin noting an improvement, as the benefit of Repo Rate reduction was seen in the borrowing cost. Asset quality also improved in both QoQ and YoY.

- Insurance: Life Insurance companies (sub-segment of insurance) reported decent increase in Value of New Business (VNB), especially in the traditional segment. Growth in premiums remained healthy with the impact of the GST 2.0 absorbed by Life Insurance companies.

- Oil & Gas: While Oil & Gas companies delivered strong YoY earnings growth (>25%) in Q4FY26, margins normalized from the elevated levels seen in Q2 and Q3FY26. This was driven by a moderation in marketing margins and inventory dynamics, as firming crude oil prices amidst geopolitical tensions in West Asia led to higher input costs without a commensurate increase in retail fuel prices.

- Auto & Auto Components: Growth was broad-based and structurally supported led by better affordability after the GST 2.0 cuts, lower interest rates and improved realizations from lower discounting and a favourable mix. Two Q4-specific seasonal factors that added support were the March fiscal year-end dispatch push and a modest end-of-quarter festive lift.

- Metals & Mining: Momentum in earnings growth was supported in Q4FY26, aided by firm commodity prices. While both ferrous players and non-ferrous players benefitted from seasonally strong volumes and an uptake in realizations, non-ferrous players saw a sharper uptake in realizations, thereby leading the sector to be a meaningful contributor to incremental profits.

- IT Services: IT Services reported a double-digit earnings growth predominantly on the back of INR’s depreciation against the US Dollar. Contrary to revenue beats witnessed in Q2FY26 and Q3FY26, Q4FY26 revenue did not see any beats. In addition to the management commentary highlighting AI-led revenue deflation as a key risk, the guidance for FY27 remained sluggish – similar to FY26 against expectations of improvement.

- Consumer Staples: GST 2.0 cuts on food, staples and personal care flowed through by Q4FY26, lifting affordability and volumes. Furthermore, State Government measures are helping the turnaround of the sector in terms of the pickup in volume growth. While benign inflation has acted as a tailwind for the sector, the West Asia conflict poses a risk in Q1FY27. However, companies in this sector are expected to utilize their pricing power and manage costs to support profitability.

- Pharmaceuticals: US generics witnessed largely weak performance, with ongoing price erosion, though key players highlighted a constructive two-year outlook. Domestic formulations delivered strong double-digit growth. Contract Development and Manufacturing Organization (CDMO) companies reported a strong QoQ recovery and robust results, with pipeline/Request For Proposal momentum improving and expectations of continued strength into FY27.

- Healthcare Services: Diagnostics saw a sharp revival with volume-led beat vs expectations, supported by wellness growth and offline shift. Hospitals trends remain structurally strong with double-digit Average Revenue Per Occupied Bed (ARPOB) growth and healthy occupancy levels.

- Utilities: Steady electricity demand amidst rising Mercury levels acted as a tailwind for the earnings recovery compared to the previous quarters.

Conclusion: Earnings expected to grow at a Faster Clip, but…

H1FY26 earnings growth started at a slower pace with Q1FY26 registering a 9.6% YoY earnings growth. However, earnings growth momentum increased in the subsequent quarters, supported by a broad-based performance. NIFTY 50 Index EPS grew ~6% between FY25 and FY26, with estimates indicating a higher growth for FY27. However, the growth estimates for FY27 could vary depending on the duration of the West Asia Conflict.

Sources: Kotak Institutional Equities, Bloomberg, and other publicly available information.

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.