Q2 FY26 Earnings - Growth momentum driven by Small and Mid-Caps

Last Updated On: 2 Dec 2025

5 min read

What’s the Point?

- Healthy earnings season(Q2FY26): 15% year-on-year profit growth (NIFTY 500) driven by Metals and Oil & Gas. Breadth of growth was good as 17 out of 30 sectors recorded double-digit sales growth

- Shifting profit pool dynamics: Large-cap contribution to Nifty 500 earnings has tapered over recent quarters, driven by the outperformance of Mid-caps

- Strong margin expansion: Margins higher than a year ago owing to decline in Raw Materials Costs and improved operating efficiency

The Q2 FY26 earnings season delivered a healthy performance, with Nifty 500 companies posting a robust 15% year on-year (YoY) profit growth. The momentum was largely driven by metals and oil & gas sectors. Even after excluding these heavyweights, earnings grew a healthy 8% YoY. Encouragingly, the breadth of growth was good as 17 out of 30 sectors recorded double-digit sales growth despite overall Sales growth remaining modest at 6% YoY.

Small and Mid-Caps continue to outpace Large Caps

Nifty 100 companies posted a modest 9% YoY PAT growth in Q2 FY26, while Mid and Small-cap segments stole the spotlight with a robust 30%+ YoY increase. The surge in Mid and Small-cap earnings was fueled by strong performances from NBFCs, Metals, Oil & Gas, and Pharmaceuticals. Even after excluding Oil & Gas, which benefited from low base effect, Mid-caps and Small-caps delivered growth of 29% and 21% YoY, respectively. Notably, the profit pool dynamics are shifting with Large-cap contribution to Nifty 500 earnings tapering over recent quarters, driven by the outperformance of Mid-caps. Mid-cap contribution rose from 15% in Q4 FY25 to 19% in Q2 FY26, while Large-Cap share declined, highlighting the broadening earnings base beyond the top 100 companies.

Sectoral Snapshot

- Metals & Mining: Steel companies benefited from lower costs driving YoY growth, while non-ferrous segment benefited from higher realizations.

- Oil & Gas: Strong rebound driven by higher refining margins and favorable base effect.

- Construction Materials: In spite of seasonal weakness, profit growth driven by low base and stable input costs.

- Pharmaceuticals: Mixed bag as CDMO and Domestic Pharma did well, while in Generics, adverse base dampened growth. Sector continues to benefit from currency tailwinds.

- Telecom: Healthy growth aided by rise in Average Revenue per User (ARPU), data usage and premiumization

- Utilities: Earnings dragged by weak demand and execution challenges in Generation and Transmission

- Chemicals: Mixed quarter with generally weak showing from commodity chemical segment

- Banks: Earnings were impacted due to the pass-through effect of the regulator’s policy rate cuts.

- Automobiles: Healthy quarter with onset of festive season. Earnings momentum to continue with impact of GST cuts to reflect from Oct-Dec quarter (Q3FY26).

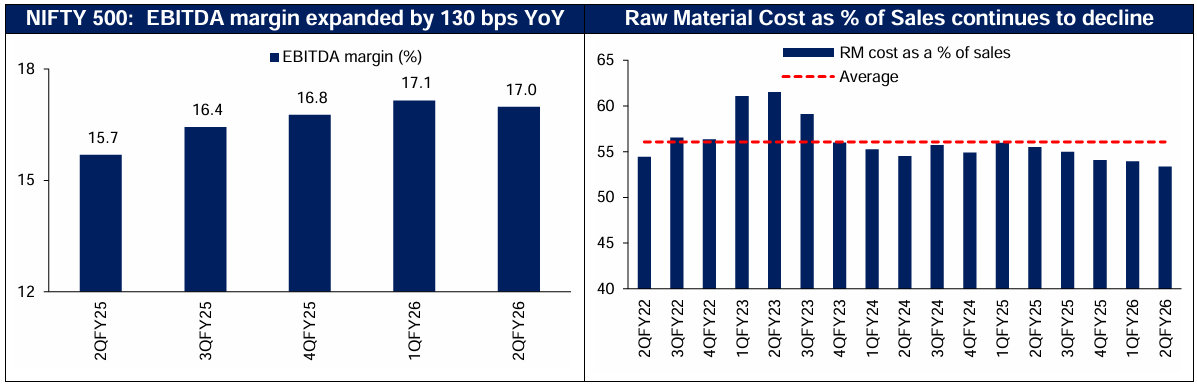

Margin Expansion

Similar to the preceding quarter, Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margin remained strong with margins being 130bps higher than a year ago. This could be attributed to decline in Raw Material Cost owing to benign crude oil prices and improved operating efficiency.

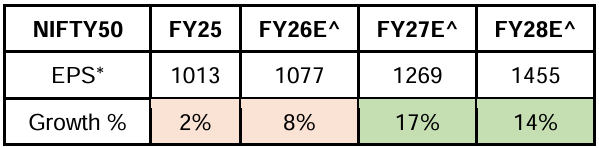

Conclusion: Strengthening Equity Outlook

*Earnings Per Share, Sources: Bloomberg, Capitaline, ^ Kotak Institutional Equities

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.