Monetary Policy Review - August 2025

Last Updated On: 13 Oct 2025

5 min read

In an expected move, the Monetary Policy Committee (MPC) unanimously decided to keep the policy repo rate unchanged at 5.5% and retained the ‘neutral’ policy stance.

The Committee noted that it should “wait for further transmission of the front-loaded rate cuts to the credit markets and the broader economy” before taking any further action on rates and stance, suggesting RBI would like to pause and assess the impact of its steps and analyse incoming data before taking any further action.

The RBI has emphasised that even though near-term CPI inflation outlook is benign it is due to volatile food prices while core inflation remains elevated. Furthermore, it noted that inflation is likely to edge up above target from Q4FY26 onwards and therefore the need “to a close vigil on the incoming data and the evolving domestic growth-inflation dynamics to chart out the appropriate monetary policy path.”

Conclusion and Outlook

The RBI’s decision to keep the policy rate and stance unchanged was on expected lines. The RBI emphasised on the point that the transmission of past policy actions is still under process and the outlook for inflation has become unfavourable given base effect turns adverse from Q4FY26 onwards. It also noted that the current headline inflation is benign due to falling food prices while core inflation has edged higher even after stripping the precious metal prices. The 10 year G-sec yields went up by 8bps post the policy announcement.

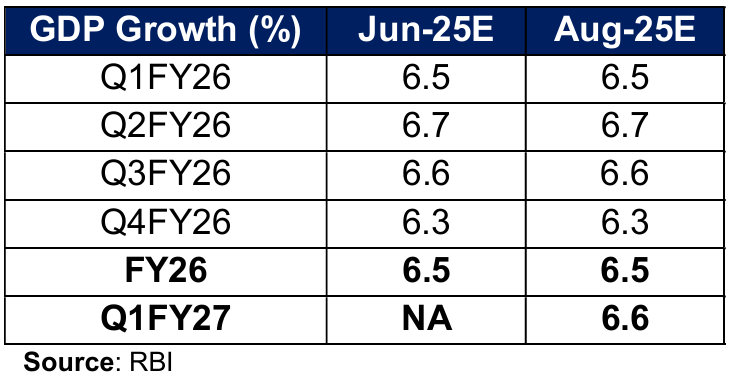

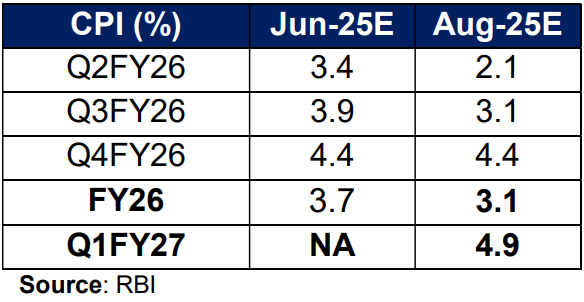

As highlighted by RBI, CPI inflation is likely to remain below RBI’s mid-point target of 4% in FY26 but rise to 4.9% by Q1FY27. In our view, in case the incoming data surprises on the downside due to global trade uncertainties, RBI could lower policy rate further as the neutral stance provides RBI with flexibility to move in either direction.

In our view, medium term outlook on Indian fixed income market remains favourable, considering:

- Headline CPI inflation is likely to undershoot RBI target of 4% in FY26. Thereafter too the rise due to unfavourable base is likely to be contained.

- Liquidity is likely to be in ample surplus given RBI’s past actions and CRR cut effective later during the year

- External sector could remain comfortable in view of steady growth in services exports, decline in oil prices and adequate foreign exchange reserves.

- Government sticking to path of fiscal consolidation and reiterating to bring down its debt to GDP bodes well for supply of Gsec over the medium term

- Higher tariff on India likely to dampen growth to the extent of 20-40bps based on most estimates

Key risk to the favourable outlook

- Below normal monsoon posing risk to food prices

Overall, in our view, yields are likely to remain rangebound with a downward bias. Falling inflation and front loading of policy rate cuts is positive from yields perspective. Thus, in view of significant liquidity provision, convergence of short-term rates and healthy corporate bonds spreads (over Gsec), one may consider investment in medium duration (schemes with duration of upto 5 years) categories especially corporate bonds focussed funds in line with individual risk appetite. Further, as long bond spreads have widened over 10 yaer G-secs, investors with a relatively longer investment horizon could continue with their allocation to longer duration funds in line with individual risk appetite.

DISCLAIMER

The views of HDFC Asset Management Company Limited, Investment Manager for HDFC Mutual Fund expressed herein as of 6th August 2025 are based on internal data, publicly available information and other sources believed to be reliable. The source for this document is the Bi-monthly Monetary Policy Statement, 2025-26, dated 6th August 2025 published by the RBI. Any calculations made are approximations, meant as guidelines only, which you must confirm before relying on them. The information contained in this document is for general purposes only and is not investment advice. The document is given in summary form and does not purport to be complete. The document does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. The information/ data herein alone are not sufficient and should not be used for the development or implementation of an investment strategy. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Past performance may or may not be sustained in future. HDFC Mutual Fund/HDFC AMC is not guaranteeing/ offering/communicating any indicative yields or guaranteed returns on investments made in the scheme(s). Neither HDFC AMC and HDFC Mutual Fund (the Fund) nor any person connected with them, accept any liability arising from the use of this document. The recipient(s) before acting on any information herein should make his/her/their own investigation and seek appropriate professional advice.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.