The Banking Sector: Time for a fresh look?

Last Updated On: 9 Apr 2026

|Created On: 9 Apr 2026

5 min read

#To know more, click here.

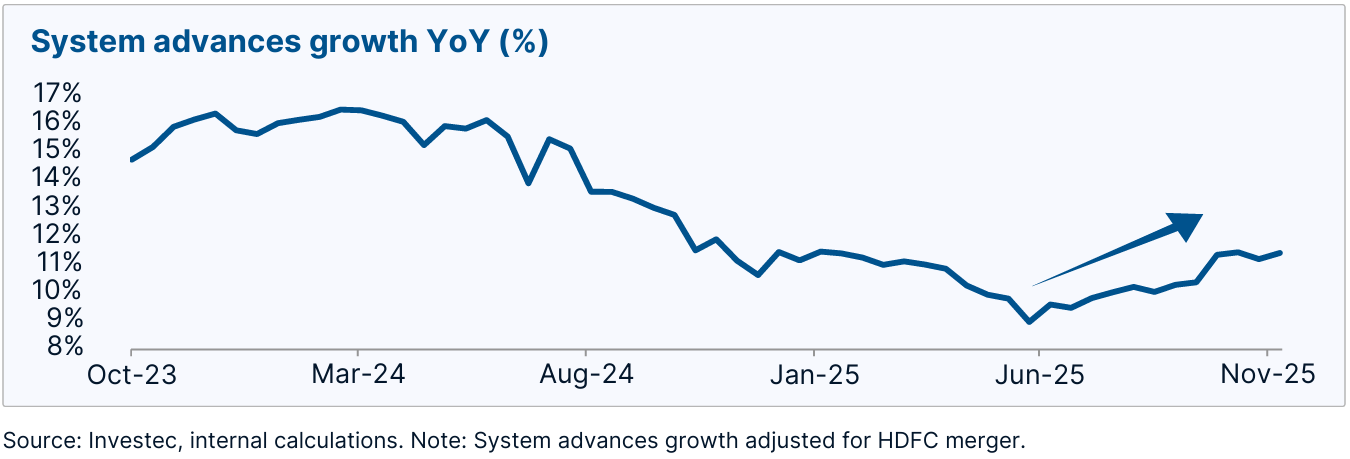

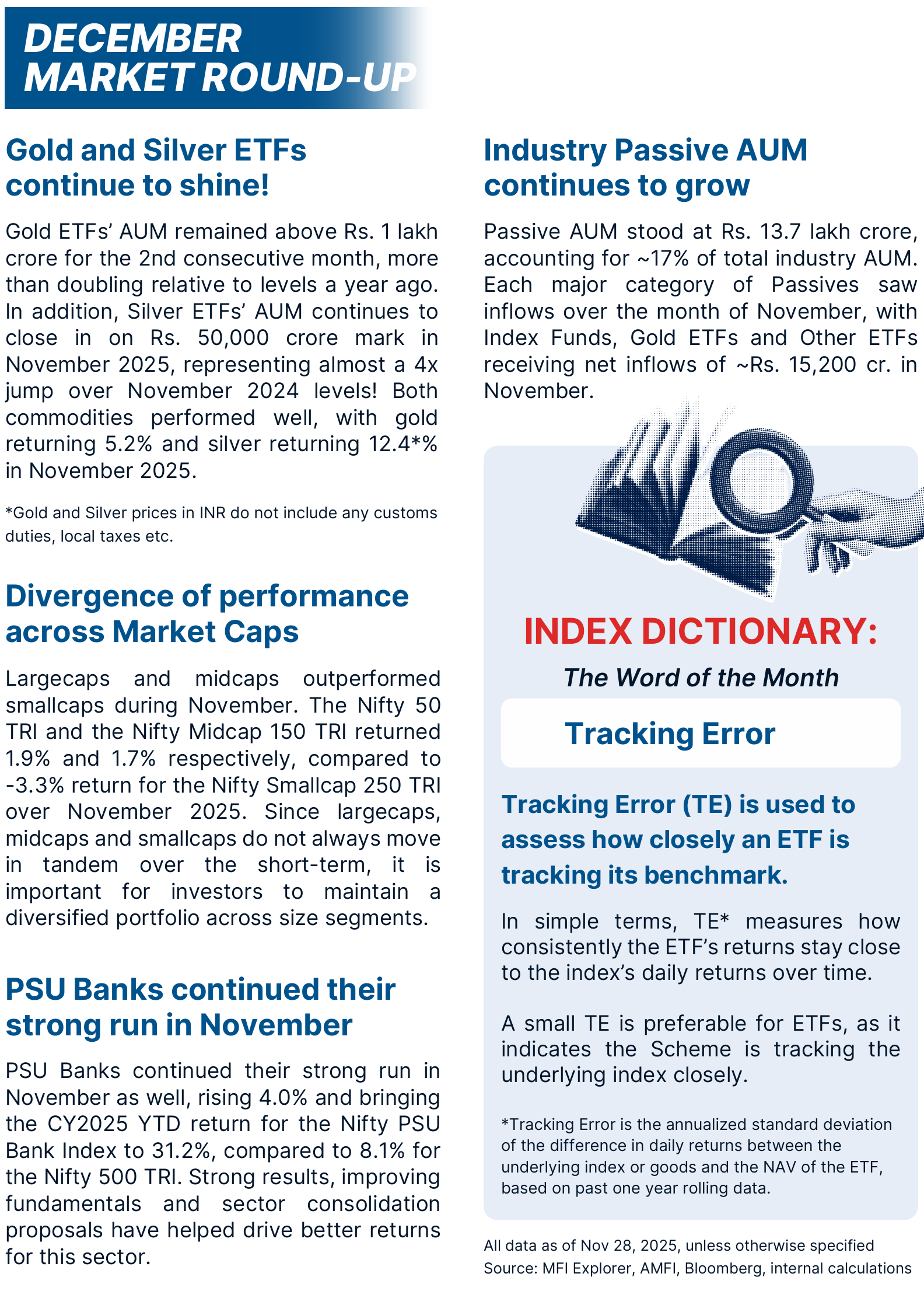

Credit growth is showing signs of recovery

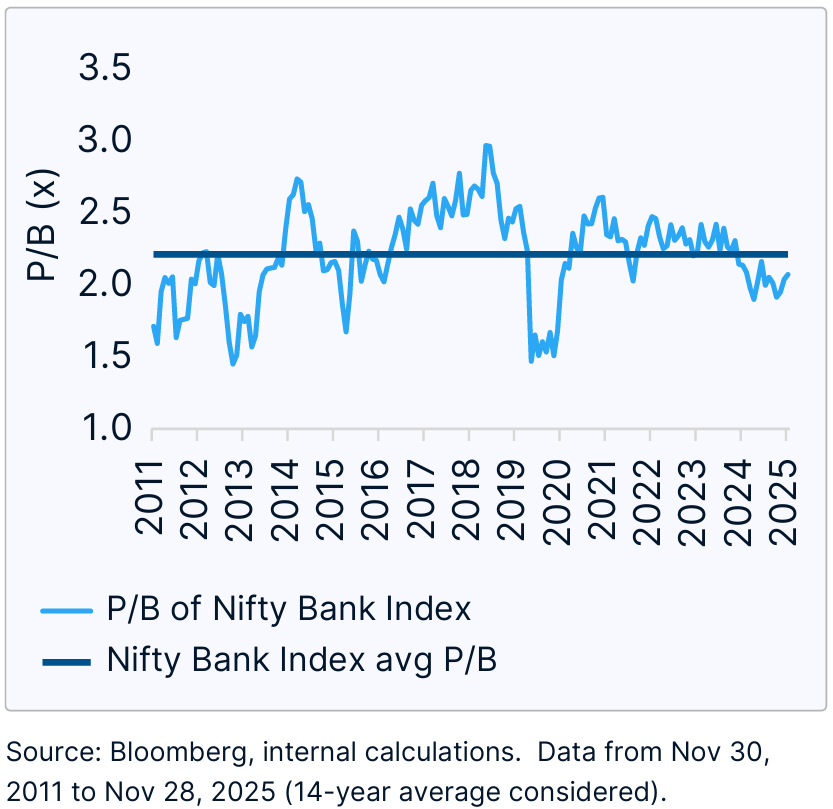

Valuations of the banking sector are close to their long-term average

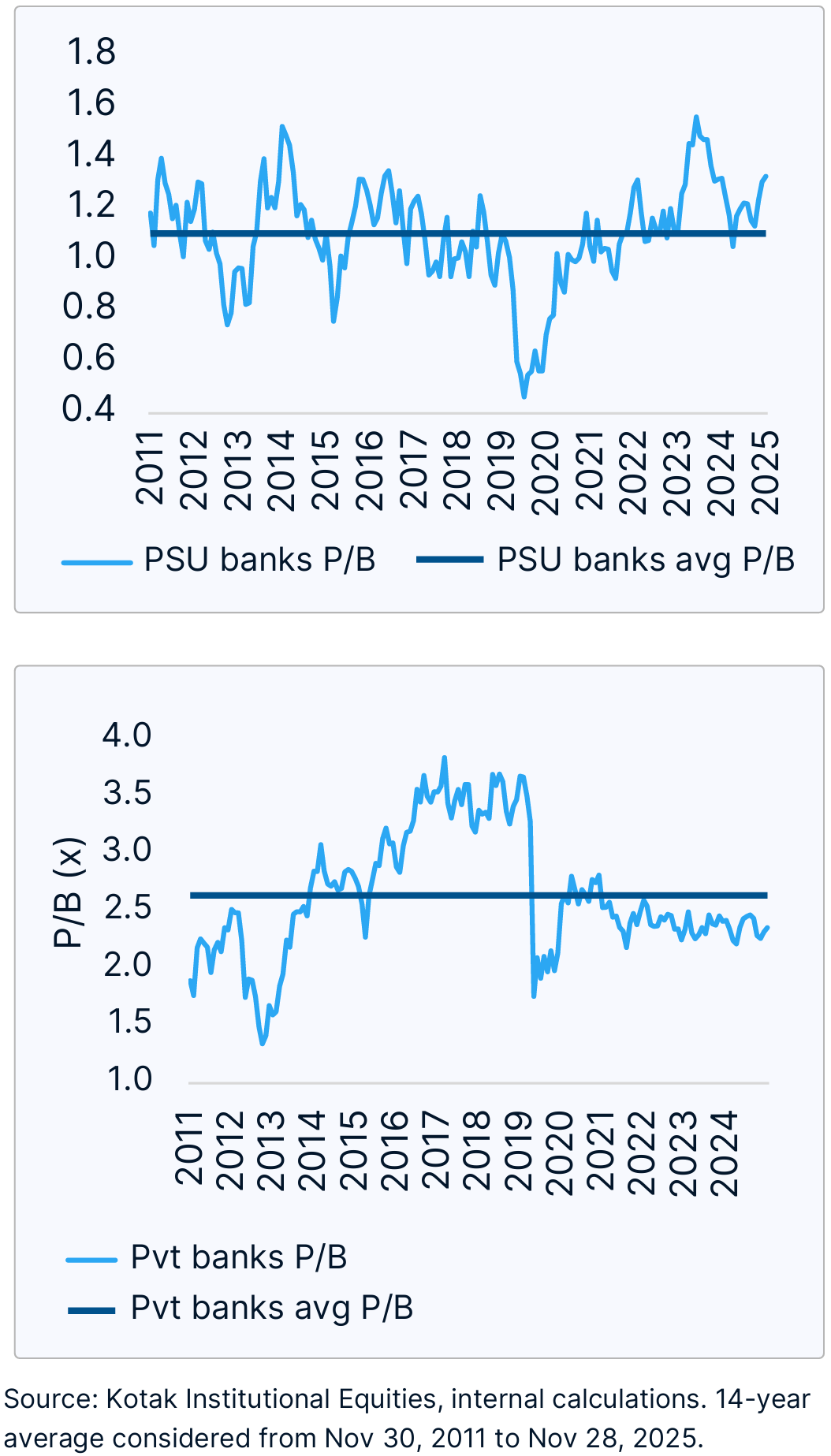

Within the banking sector, valuations of both PSU and Private banks are close to their long-term average. The P/B of PSU Banks was 1.3x and of Private Banks was 2.4x, with their long term (14-year) average P/B at 1.1x and 2.6x respectively, as of November 28, 2025.

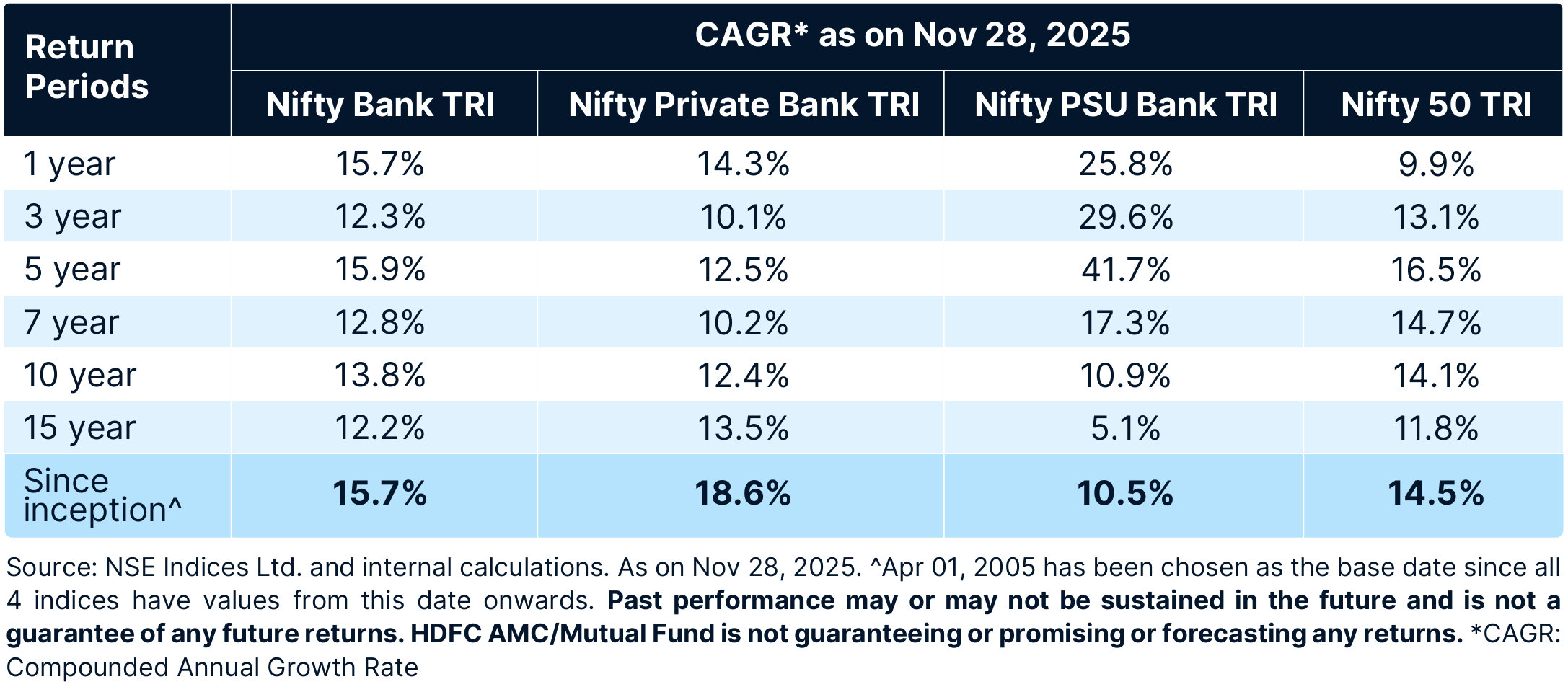

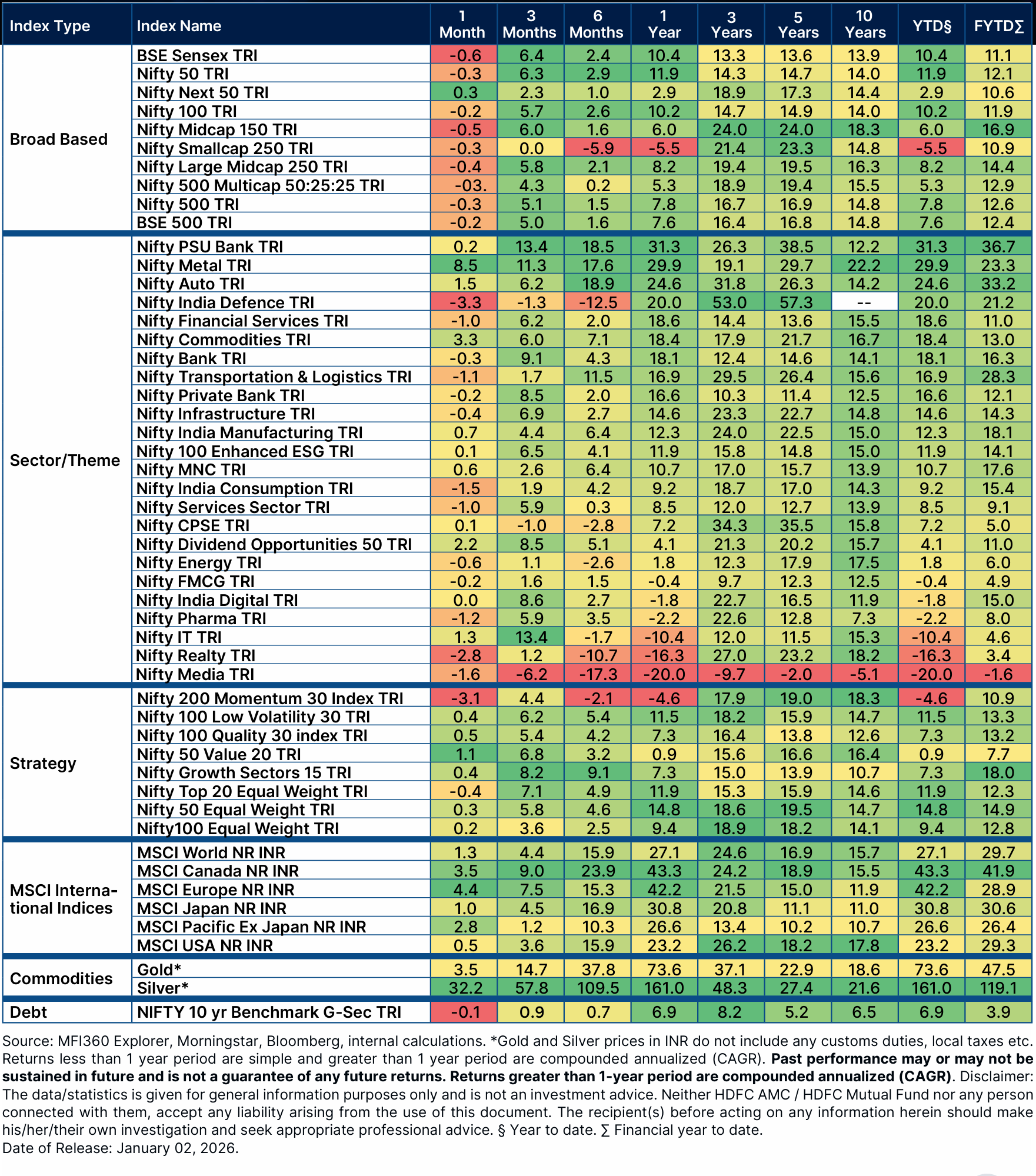

CAGR of Banking sector indices and Nifty 50

Over the 5-year ending November 2025, the CAGR was 41.8% for Nifty PSU Bank TRI, 15.9% for Nifty Bank TRI, 12.5% for Nifty Private Bank TRI and 16.5% for Nifty 50 TRI.

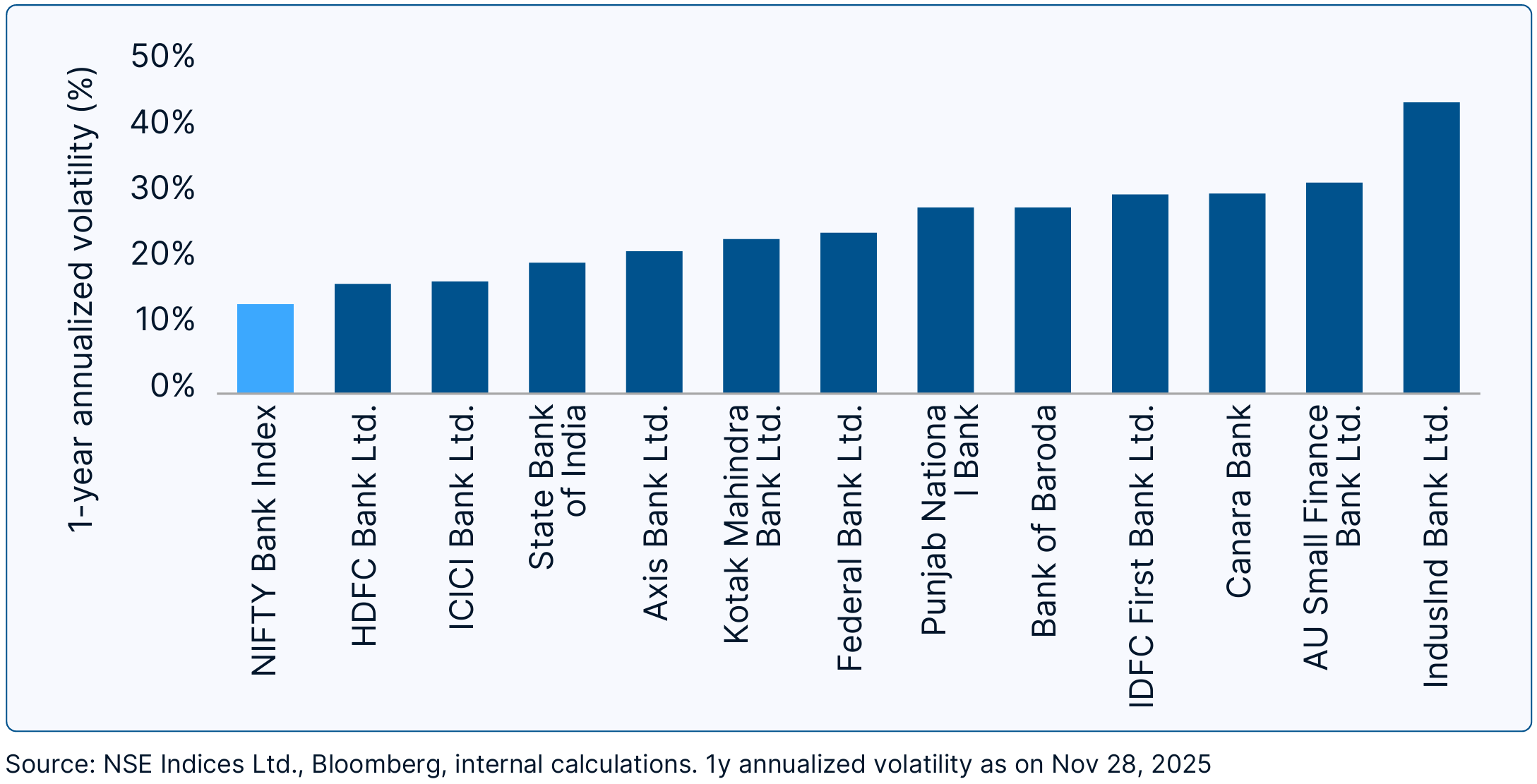

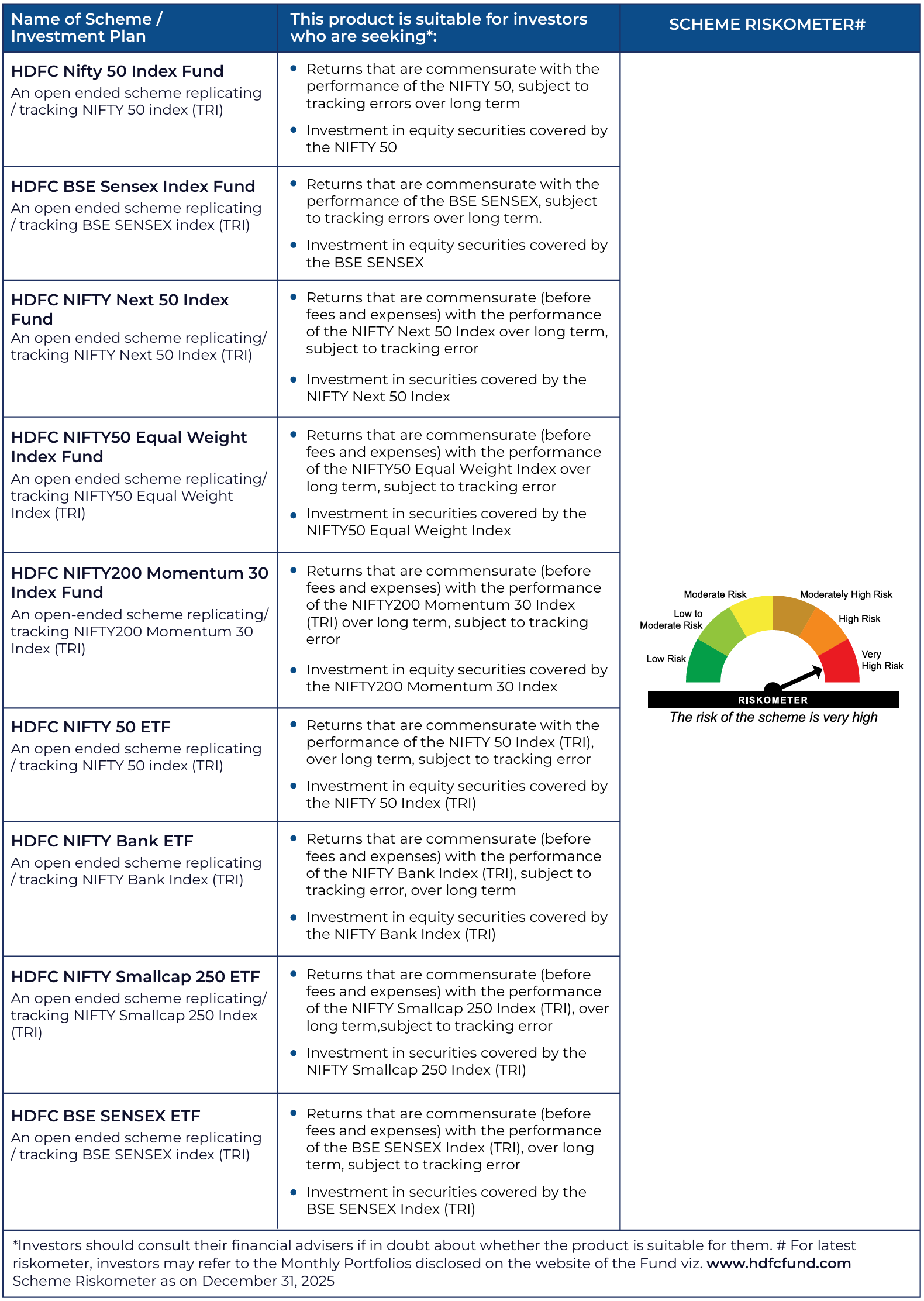

1-year annualized volatility of NIFTY Bank Index is less than its constituents

NSE Disclaimer: The above mentioned Schemes offered by HDFC Asset Management Company Limited (HDFC AMC) having benchmark as NSE Indices are not sponsored, endorsed, sold or promoted by NSE INDICES LIMITED (formerly known as India Index Services & Products Limited (IISL)). NSE INDICES LIMITED does not make any representation or warranty, express or implied (including warranties of merchantability or fitness for particular purpose or use) and disclaims all liability to the owners of the Products or any member of the public regarding the advisability of investing in securities generally or in the Products linked to the respective underlying indices of NSE to track general stock market performance in India. Please read the full Disclaimers in the Offer Document of the Products.

BSE Disclaimer: The above mentioned schemes of HDFC AMC having benchmark as BSE Indices are based on the underlying indices of BSE. BSE® and SENSEX® are registered trademarks of BSE Limited. The Schemes is not sponsored, endorsed marketed or promoted by BSE or their respective affiliates. Please refer to the Scheme Information Document for disclaimers.

MSCI Disclaimer: HDFC Developed World Overseas Equity Passive FOF is not sponsored, endorsed, sold or promoted by MSCI. All MSCI indexes are owned by MSCI and provided as-is without any warranties. MSCI assumes no liability for or in connection with the MSCI indexes. Please refer the Scheme Information Document for complete disclaimer.

CRISIL Disclaimer and Copyright Notice: “© CRISIL Limited. All Rights Reserved Each CRISIL Index (including, for the avoidance of doubt, its values and constituents) is the sole property of CRISIL Limited (CRISIL). No CRISIL Index may be copied, retransmitted or redistributed in any manner. While CRISIL uses reasonable care in computing the CRISIL Indices and bases its calculation on data that it considers reliable, CRISIL does not warrant that any CRISIL Index is error-free, complete, adequate or without faults. Anyone accessing and/or using any part of the CRISIL Indices does so subject to the condition that: (a) CRISIL is not responsible for any errors, omissions or faults with respect to any CRISIL Index or for the results obtained from the use of any CRISIL Index; (b) CRISIL does not accept any liability (and expressly excludes all liability) arising from or relating to their use of any part of CRISIL Indices.

The views are based on internal data, publicly available information and other sources believed to be reliable. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Stocks/Sectors referred are illustrative and not recommended by HDFC Mutual Fund (“the Fund”)/ HDFC AMC. The Schemes of the Fund may or may not have any present or future positions in these sectors. It should not be construed as an investment advice or a research report or a recommendation by the Fund/HDFC AMC to buy or sell the stock or any other security covered under the respective sector/s. The Fund/ HDFCAMC is not guaranteeing any returns on investments made in the Scheme(s). Past performance may or may not be sustained in future and is not a guarantee of any future returns. HDFC Asset Management Company Limited (“HDFC AMC”) does not warrant the completeness or accuracy of the information herein. Neither HDFC AMC, nor any person connected with it, accepts any liability arising from the use of this material. The recipient(s) should before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Receive Index Insider every month for insights shaping the passive investing world

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.