Underlying Resilience in India’s Current Account Despite a Challenging Macro Backdrop

Last Updated On: 18 Jun 2026

5 min read

What’s the Point?

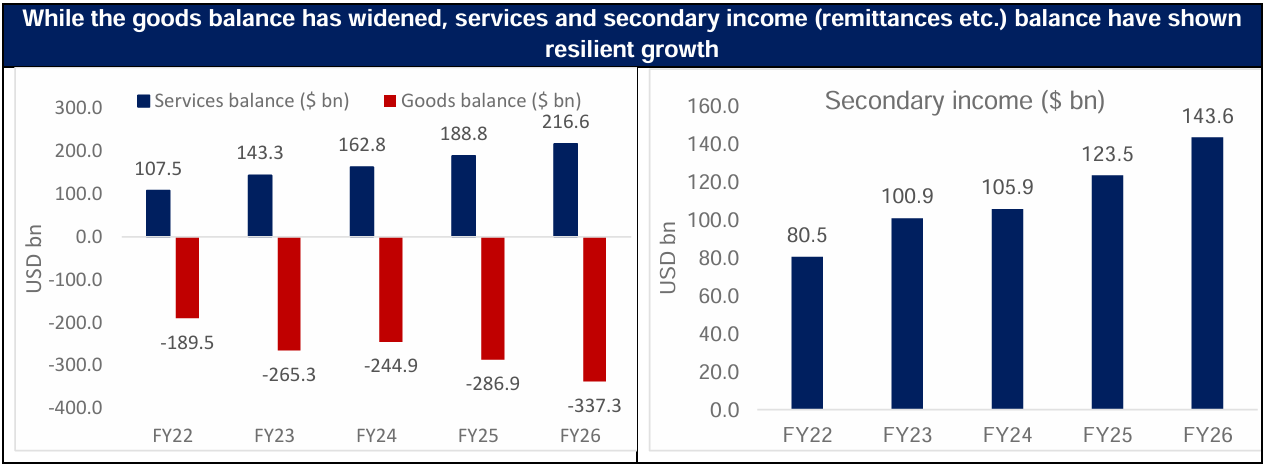

- A rising services surplus $216.6bn in FY26 and steady remittance inflows ($143.6bn) continue to anchor the current account despite a widening goods deficit

- While the current account remains manageable, weaker capital inflows—particularly volatile portfolio flows—have emerged as the primary source of pressure

- Recent RBI and Government measures aimed at attracting inflows from a variety of sources could help stabilise the rupee and improve overall Balance of Payments (BoP) dynamics in the near term

India’s latest Balance of Payments (BoP) data present a picture of underlying resilience in the current account despite high commodity prices and the impact of higher tariffs on exports. While the goods trade deficit widened in FY26 largely due to higher oil, gold and capital goods imports, a large part of the increased trade deficit was offset by steadily improving services surplus and secondary income (includes remittances etc.) balances. More specifically:

i) India recorded a robust services surplus of $216.6 billion in FY26, almost doubling from the $107.5bn level in FY22. This reflects the strength of India’s IT and business services exports, which have evolved into the primary stabilising force in the BoP.

In fact, the services surplus is large enough to offset a significant portion of the goods deficit—highlighting a structural shift in India’s external sector from goods dependence to services-led support.

ii) Secondary income, driven largely by remittances, continues to provide an important buffer. Net inflows under this head reached $143.6 billion in FY26, up from $80.5bn in FY22, maintaining a consistent upward trajectory.

Unlike portfolio flows, remittances are relatively stable and less sensitive to global financial conditions, making them a critical anchor for the current account.

Source: CMIE, internal calculations

The growth witnessed in the services surplus and secondary income segment is important for India’s long-term macro stability because these components have shown far less volatility than the goods trade deficit. Resilience in these components can cushion the effect of volatile commodity prices on India’s current account balance, as we are currently witnessing.

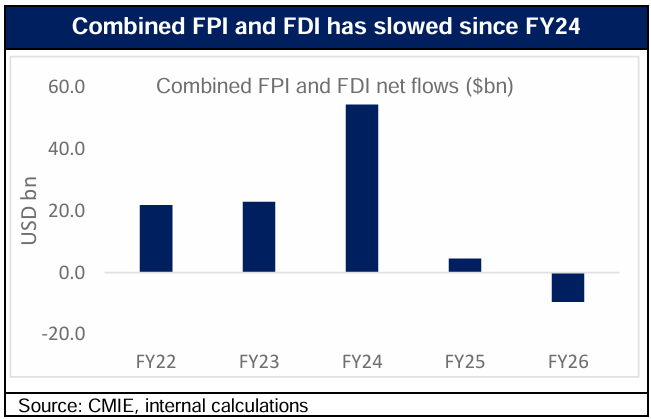

While the current account was resilient in FY26, net foreign flows were weak in the capital account

Financing the current account deficit was challenging, with lower FDI and FPI flows recorded in FY26 compared to previous years. FPI net outflows stood at $16bn in FY26, significantly lower than the $3.5bn net inflows in FY25. FDI net inflows recovered somewhat in FY26, rising to $7bn from $1bn in FY25. However, net FDI inflows in FY26 are markedly lower than earlier in the decade, especially when contrasted with the strong inflows of around $30bn recorded as recently as FY23.

Accordingly, the RBI and Government have taken steps to attract inflows and stabilize the rupee

In light of the weak investment inflows, the RBI and Government have announced a raft of policy measures to stabilize the rupee in recent weeks. Some of the key measures announced by the RBI include:

- Expanding the universe for Government securities under the Fully Accessible Route (FAR). This, along with tax benefits on G-Secs provided by Government could help attract foreign capital.

- Allowing concessional forex swap till 30th September 2026 to incentivize External Commercial Borrowings (ECB) by Public Sector Undertakings.

- Bearing the full hedging cost till 30th September 2026 for raising fresh 3–5-year Foreign Currency Non-Resident Bank [FCNR (B)] deposits by Authorized Dealers. FCNR (B) are bank deposits held in a foreign currency and secure the holder of the deposit from currency fluctuations.

This latest set of measures to stabilize the rupee is broader in scope than those announced in 2013, as it diversifies the potential sources of inflows across NRI deposits, government bond investments and ECBs. These measures could draw $40-50bn inflows to India (Source: Reuters) and could help alleviate the downward pressure on the rupee. In comparison, the FCNR(B) measures announced in 2013 were estimated to have drawn $26bn in inflows.

Conclusion

The steady expansion of services exports and remittances has fundamentally strengthened the resilience of the current account, helping offset higher tariff and cyclical pressures from higher commodity prices. However, the moderation in foreign inflows—particularly portfolio flows—highlights a shift in the nature of external vulnerability. The recent policy measures aimed at enhancing foreign currency inflows and deepening capital markets are therefore timely, and if realised, could provide an important buffer to the balance of payments.

Source: CMIE, Bloomberg, Reuters, publicly available information

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.