Time to go Long on Duration?

Last Updated On: 24 Sep 2025

5 min read

What’s the Point?

- Yields at the long end have remained volatile over the last few months due to various reasons. Yield on 10-year G-sec has gone up by 24bps, while yield on 20- and 30-year G-sec has seen even sharper rise.

- Although short-term factors have caused some volatility in long-term yields, the structural drivers that typically influence the longer end remain supportive.

- Given the current volatility, it may be an opportune time for long term investors to take advantage of the current yield and potential spread compression.

Over the last few months, long end of the yield curve has risen sharply, with 10-year G-sec yield rising from ~6.26% to ~6.5%. The yields on the extreme long end have risen even sharper, with 20-year G-sec and 30-year G-sec yields increasing by 40bps and 43bps respectively.

What led to the rise in yields at the longer end of the Yield Curve?

- Change in policy stance - While MPC reduced the policy rate by 50bps in June’25 meeting, there was a change in policy stance from accommodative to neutral. Change in stance was viewed negatively by the market participants which led to bear steepening i.e. yields at the long end of the curve, rising disproportionately.

- Fears of Fiscal Slippage - GST rationalisation and lower personal tax collection has also led to rise in yields.

- Demand Supply mismatch for longer dated government bonds

| G-Sec | 17-Sep-25 | 16-May-25 | Change in Yield (%) |

|---|---|---|---|

| 10-year G-Sec | 6.50% | 6.26% | 0.24% |

| 20-year G-Sec | 6.99% | 6.59% | 0.40% |

| 30-year G-Sec | 7.19% | 6.76% | 0.43% |

Key Factors that could drive yields lower

Although short-term factors have caused some volatility in long-term yields, the structural drivers that typically influence the longer end remain supportive.

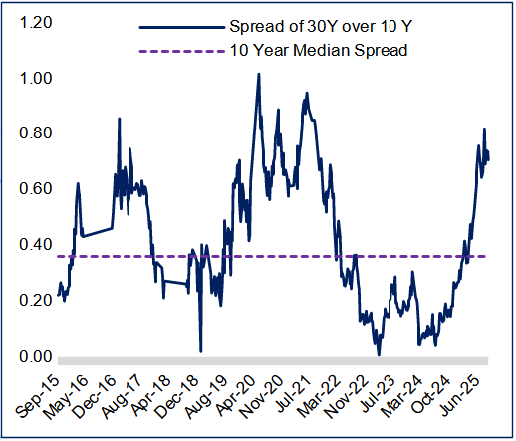

- Elevated spread between 30Y and 10Y yields - The spread between 30-year G-sec and 10-year G-sec is at 71bps vs 10-year median of 36bps providing a reasonable opportunity to capture spread compression.

- Inflation under control - Headline CPI inflation is likely to undershoot RBI target of 4% in FY26. Thereafter, the rise due to unfavourable base is likely to be contained.

- Low risk of fiscal slippage - FY26BE estimate the fiscal deficit to narrow to less than 4.5%. We believe, that risks to fiscal not meeting target appear low in view of hefty dividend from RBI and room to reduce spending. Adherence to the fiscal roadmap is likely to bode well for long term yields.

- Comfortable external sector - India’s Balance of payment is well placed in view of manageable current account and ample forex exchange reserve.

- Limited fiscal impact of GST rate cuts – GST cut likely to have a limited fiscal impact according to the Government.

- S&P’s upgrade of India’s sovereign rating - The rating upgrade is positive from the perspective of faith in India’s long-term growth trajectory and likely to increase flows into Indian debt markets.

- Fed Rate cut -US Fed rate cut by 25 basis points and signalling the possibility of two more rate cuts in the current year further creates room for Monetary Policy Committee (MPC) to consider additional easing.

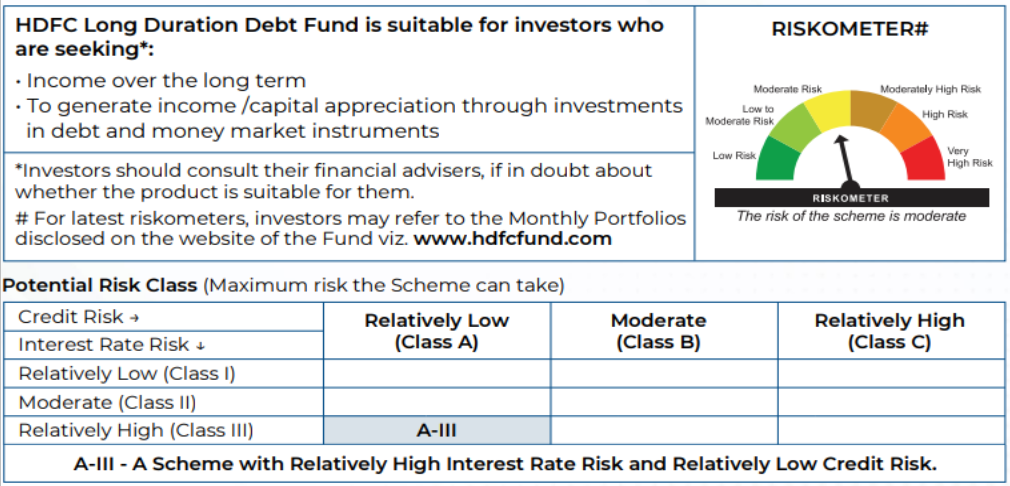

Conclusion: Given the current volatility, it may be an opportune time for a longer-term investor to take advantage of the current yield and potential spread compression. In view of the above, investors with a relatively longer investment horizon could consider allocating to HDFC Long Duration Debt Fund in line with individual risk appetite. The Scheme is an open-ended debt scheme investing in instruments such that the Macaulay Duration of the portfolio is greater than 7 years. A relatively high interest rate risk and relatively low credit risk.

The current investment strategy is to predominantly invest in long dated government securities of 25+ years maturity (papers maturing in 2050 and beyond), while retaining the flexibility to invest in the other segments of yield curve which may offer relatively better value on tactical basis.

Fund Quants as of 15th September 2025

Sources: Bloomberg and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.