INR crosses USD 90 – Potential India-US trade deal could hold the key

Last Updated On: 9 Dec 2025

5 min read

What’s the Point?

- INR has depreciated by ~5-6% against the USD over the past few months.

- Persistent FII outflows, U.S. tariff-related trade uncertainty and RBI’s calibrated, non-defensive intervention strategy has led to the depreciation.

- While a weaker rupee is negative for imports and inflation, it is positive for exporters as it could help boost exports, shield local manufacturers, offset higher tariffs on India and protect from China’s dumping.

- Strong forex reserves and a possible India-US trade deal ahead could offer support to the INR over time.

INR crosses the USD 90 mark

The Indian Rupee (INR) has faced sustained depreciation over the past few months, crossing the psychological 90 per USD threshold in early December 2025, a sharp 5-6% decline from levels around 85 in late 2024. This weakening stems from a mix of domestic and global factors amplifying USD strength amid evolving trade dynamics.

Key Reasons for INR Depreciation

Foreign Institutional Investor (FII) outflows - has been another reason for INR depreciation. FIIs have withdrawn over Rs 13k cr from equity markets in the first week of Dec’25 alone. For the CY 2025, total FII net selling in equities has reached nearly ₹1.50 lakh crore, underscoring sustained foreign capital flight from Indian equities. Investors are redirecting capital toward US assets yielding higher returns and other emerging markets.

Pressure on External Balance – India’s trade and current account deficit has also worsened in the past 6 months, putting pressure on the INR.

Geopolitical trade uncertainties - Ongoing U.S. trade tensions and high tariffs on Indian exports have further pressured the rupee. Since the imposition of tariffs (since Apr’25), INR has depreciated over 6% against the USD.

Impacts of INR Weakness

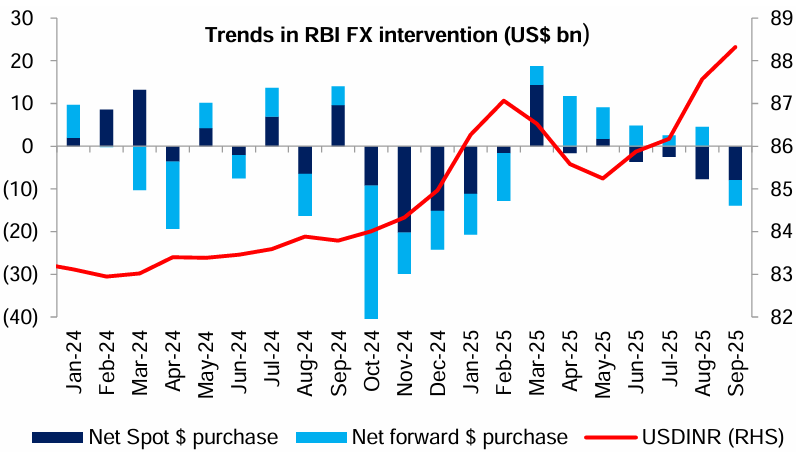

Impact on Liquidity - Depreciation of INR vs USD has led to some intervention in forex market by the Reserve Bank of India (RBI), wherein the central bank sells USD and buys INR. This trade of buying INR and selling USD can impact durable liquidity in the system. RBI’s Rs1.5 tn worth of durable liquidity easing measures is expected to help offset the likely tightness from higher currency leakage and FX intervention.

Risk of imported inflation - A weaker rupee raises the rupee price of imports. Higher import bills lead to a widening of the trade deficit and, in turn, keep the currency under pressure. This imported inflation, could further lead to rise in CPI.

Positive for Exporters - Conversely, exporters reap substantial benefits. A weaker rupee could boost exports, shields local manufacturers, offsets higher tariffs on India and protect from China’s dumping. IT services companies could see some revenue uplift in INR terms, improving Q3FY26 outlook, while companies in other industries like textiles, gems, etc could gain pricing power in competitive global markets.

Strong Forex Reserves and Potential India-US Trade Deal could provide some comfort

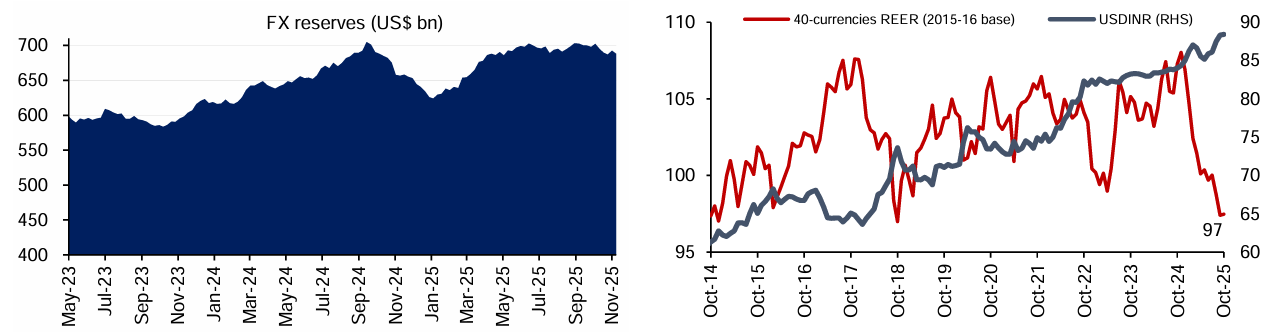

Strong Forex Reserves - India’s sizeable forex reserves provide comfort during periods of rupee weakness. With ~ $693 bn in reserves, the RBI has ample capacity to smooth excessive volatility by supplying dollars when market liquidity tightens. These reserves also reassure investors and rating agencies that India can comfortably meet its external obligations, even amid FII outflows or global risk aversion.

India-US Trade deal - Once the India-US trade deal is announced (in the near future), capital inflows can come back to India which may lead to Balance of Payment (BOP) surplus, providing room for some appreciation in the INR.

INR undervalued on REER basis - While INR has depreciated against the USD, it continues to remain undervalued on REER* basis, aided by declining inflation. Therefore, there could be some appreciation in USD-INR once the uncertainty subsides.

*The Real Effective Exchange Rate (REER) is a measure that adjusts the nominal Effective Exchange Rate (NEER) for inflation differences between a country's economy and its trading partners.

Why the current situation is NOT similar to 2013?

We saw a similar pressure on the INR in the year 2013.However, the current INR depreciation differs markedly from the 2013 crisis, as India now boasts stronger GDP growth, a much narrower current account deficit (CAD), lower inflation, higher forex reserves and a healthier fiscal position.

| Indicator | CY2013 | Latest* |

| GDP Growth (%) | 6.15 | 8.2 |

| CAD (% of GDP) | 4.8 | 1.3 |

| CAD (% of GDP) | 4.8 | 1.3 |

| CPI Inflation (annual avg %) | 9.85 | 0.25 |

| Forex Reserves (USD Bn) | ~290 | ~693 |

| *Latest released data | ||

Key Takeaway: The INR depreciation is driven by a wider current account deficit, persistent FII outflows, U.S. tariff related trade uncertainty and RBI’s calibrated, non-defensive intervention strategy. Unwinding of RBI’s NDF positions has added to near-term pressure. However, the situation is far more stable than in 2013. India now has stronger growth, lower inflation, a healthier fiscal position and robust forex reserves of about $693 billion, providing ample capacity to smooth volatility. A weaker rupee could boost export as it shields local manufacturers, offsets higher tariffs on India and protects from China’s dumping. With the rupee undervalued on a REER basis and a possible India-US trade deal ahead, capital inflows could revive, offering support to the INR over time.

Sources: RBI, Bloomberg, Kotak Institutional equities and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.