India’s External Balance Strengthens as Gold Imports Normalize and Services Cushion Deficit

Last Updated On: 30 Dec 2025

5 min read

What’s the Point?

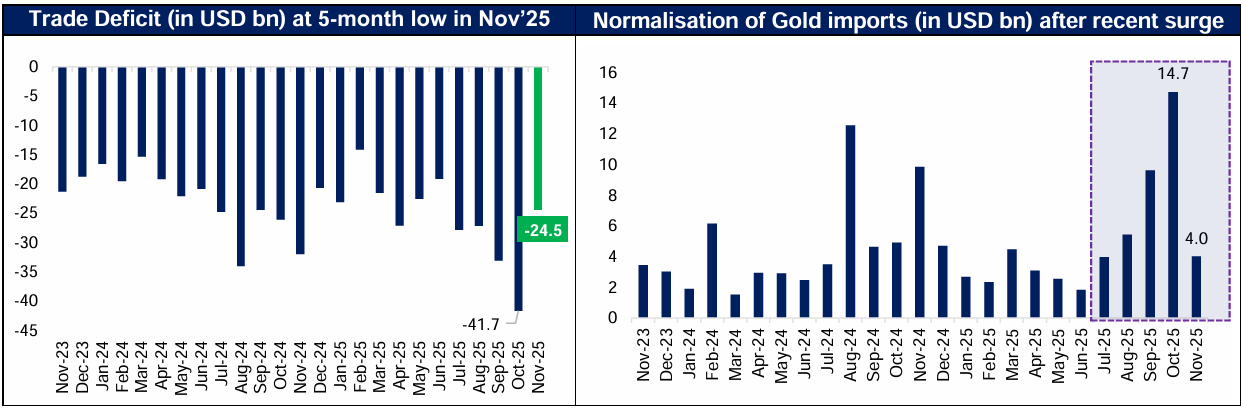

- Sharp Trade Deficit Correction: Goods deficit compressed to $24.5bn in Nov’25 from $41.7bn in Oct’25, led by $12bn+ normalization in gold and silver imports.

- Exports and Services Resilience: Improved exports performance, a consistently strong services surplus and resilient remittance inflows continue to cushion the current account.

- Capital Account in Focus: A manageable current account shifts the spotlight to capital flows, where volatile FPIs remain a key variable, making stable FDI essential for balance-of-payments resilience.

Trade Deficit at a 5-month low

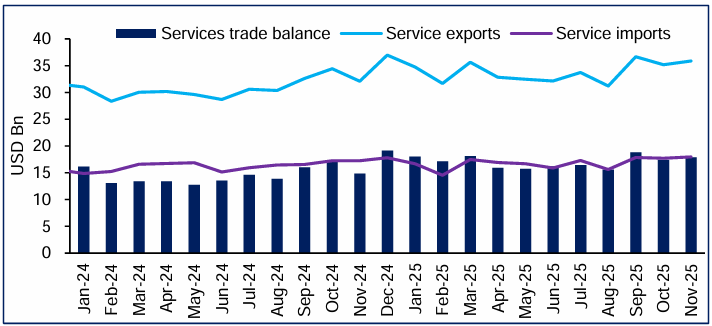

India’s external metrics improved meaningfully in November 2025 as Merchandise exports increased 19.4% year-on year to $38.1bn, while imports contracted 1.9% to $62.7bn, compressing the goods trade deficit to $24.5bn, the lowest since Jun-25 and far below record $41.7bn gap of Oct-25. The correction was driven by normalization in gold and silver imports following festive-season front‑loading, alongside stable oil imports. On the invisibles side, the services surplus was steady around $17.9bn, helping cushion the current account.

Why November’s Current Account Position improved?

Lower gold imports post festive normalization: After October’s spike, gold imports fell by $10.7bn (from $14.7bn in Oct’ 25 to $4.0bn in Nov’25) with Silver imports also dropping by ~$1.6bn (vs Oct’25). The normalisation of festive demand sharply reduced non-oil import pressure. Simply put, out of the total Trade Deficit reduction of $17.2bn (vs October), ~$12.3bn could be attributable to Gold and Silver imports alone.

Improved exports, especially to the US and China, led by non-tariffed segments

Merchandise exports rose to $38.1bn (+19.4% YoY), driven by engineering goods ($11.0bn, +24% YoY), electronics ($4.8bn, +39% YoY), and pharma ($2.6bn, +21% YoY). Country-wise, exports to the US jumped ~23% YoY to $7.0bn, with strength in segments not directly impacted by high/differential India tariff. Exports to China surged ~90% YoY as China looks to diversify its export focus away from US.

Higher remittances, an added layer of cushion

Remittances remain another key support, with receipts expected to be ~$135Bn for FY26, which would be almost twice the pre-Covid level of $70bn.

Currency weakness aiding export competitiveness

Weaker rupee over the last few quarters has also aided export competitiveness at the margin by partially offsetting tariff‑related pressures and making Indian goods/services relatively cheaper in dollar terms.

Current Account Manageable, focus to shift to capital side

While the near-term current account dynamics look manageable, the focus increasingly shifts to the capital account as the key factor for overall Balance of Payments stability. A more fragmented global environment, persistent geopolitical risks and episodes of risk-off sentiment can amplify volatility in portfolio flows, particularly in emerging markets. In addition, a weaker Rupee and the recent relative outperformance of global equity markets may intermittently divert flows away from India. In fact, net FPI flows have been negative in 3 out of last 4 CYs (including CY25). Against this backdrop, attracting stable and durable capital in the form of FDI becomes more critical to finance the current account deficit.

Conclusion: Looking ahead, the durability of the narrower trade deficit will largely depend on whether recent export momentum can be sustained amid a still uneven global growth environment and ongoing tariff-related uncertainties. Merchandise exports may face intermittent headwinds, but structural tailwinds from services exports and steady remittance inflows provide a strong counterbalance. Assuming no major external shock, such as a sharp spike in oil prices or a severe global slowdown, the current account deficit is likely to remain within a manageable range.

Sources: Bloomberg, CMIE and other publicly available information

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.