Fiscal Consolidation on track with Union Budget around the corner!

Last Updated On: 13 Jan 2026

5 min read

What’s the Point?

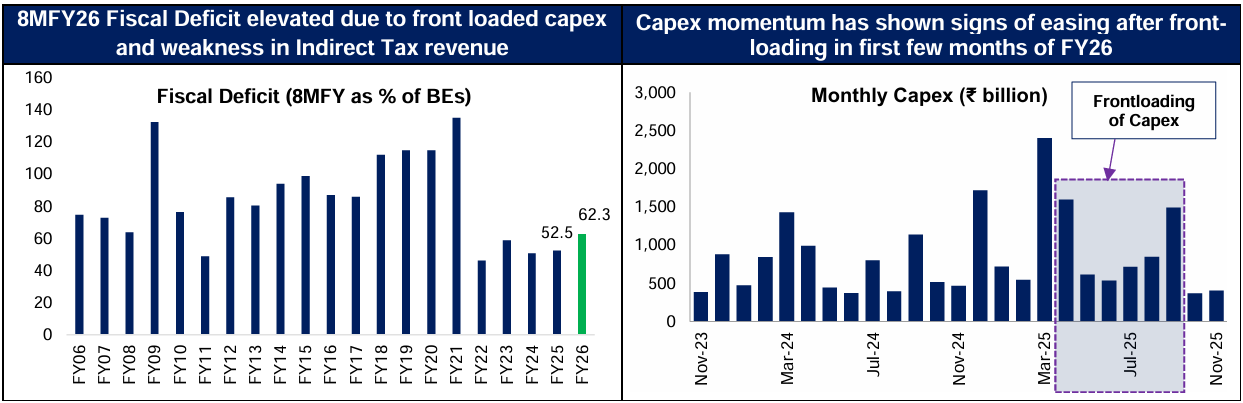

Fiscal Deficit at a higher pace, yet fiscal discipline intact: At 62.3% of FY26 Budgeted Estimate during April November’25, deficit looks high due to front‑loaded capex and weakness in indirect taxes, but underlying fiscal consolidation remains intact.

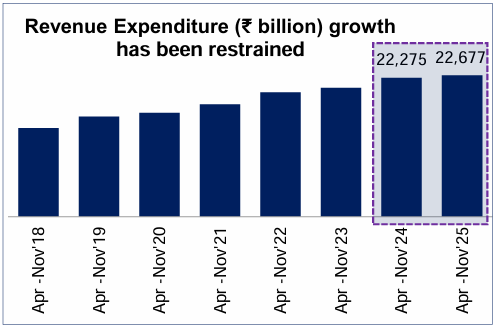

Fiscal Consolidation on track: Revenue spending restraint, easing capex pace and strong non‑tax revenues significantly limit risks of fiscal slippage for FY26.

Policy Space Intact: Controlled finances preserve policy flexibility, enabling the upcoming Budget to prioritise growth and reforms without compromising fiscal consolidation.

As the Union Budget approaches, the state of the government’s finances assumes heightened importance for markets and policymakers alike. The fiscal position for this year effectively defines the starting point from which Budget choices are made for next year with reference to growth impetus, welfare spending, tax rationalisation, Government borrowing and medium-term consolidation. In view of this, India’s fiscal dynamics are being keenly monitored by market participants. While fiscal deficit clocking 62.3% of the FY26 Budget Estimate (BE) by November 2025 may appear elevated, a closer look at the underlying numbers shows that fiscal consolidation is on track.

Why the Fiscal Deficit looks elevated Mid-year

Softening of Indirect Tax collections: Gross tax revenue growth slowed materially during the first eight months of FY26. While direct taxes held up relatively better (+7% YoY, FYTD), indirect tax performance weakened (-1.2% YoY, FYTD) reflecting GST rate rationalisation, lower customs duties and timing mismatches in IGST settlements to State Governments. Subsequently though, GST collections have shown signs of stabilization in December 2025. GST collections (excluding cess) grew 6.1% YoY to Rs1.75tn in December 2025, a sharp rebound from the almost flat November 2025 print. Also, shortfall in collections due to broader rate cuts could be offset to an extent by the new cess on Pan Masala and higher excise duties on tobacco and related-products (effective 1st Feb 2026)

Front-loaded Government Capex: Capital expenditure surged early in the fiscal year (up 28% YoY, FYTD) owing to front-loading of capex by the Government. This is in line with the Finance Ministry’s guidance to various ministries in Apr’25 to front load capex spending in order to ensure timely project-execution and avoid year-end backlog amid subdued private capex and global headwinds. With FYTD Capex (till Nov’25) at 59% of FY26BE (vs ~46% last year), one could expect Government Capex to moderate during the remainder of the year.

Why Fiscal Slippage risk looks limited

Pace of Capex to ease: With a significant share of the annual capex budget already utilised, the spending requirement for the remainder of the year is lower. In fact, after front loading of capex in first few months of FY26, the pace of capex has eased out in recent months. Capex growth in Defence (FYTD, +50% YoY) and Roads (FYTD, +20% YoY) has led the Govt. capex surge in FY26.

Non-tax revenues provide a strong buffer: A substantial dividend transfer of Rs 2.7 Trillion from the Reserve Bank of India, along with higher PSU dividends, has lifted non-tax revenues well above budgeted assumptions. This has offset a meaningful portion of the tax shortfall, easing pressure on borrowing requirements. Non-Tax revenue for 8mFY26 is at 89% of FY26BE.

Consumption push to help maintain fiscal consolidation: Targeted measures to support consumption, through GST rate cuts, Income tax relief, focused welfare transfers can help boost demand in the economy. Consumption stimulus can strengthen the revenue base and limit fiscal pressure, reinforcing consolidation rather than diluting it.

Controlled Fiscal situation lends policy flexibility ahead of the upcoming Union Budget

While the mid-year fiscal deficit appears elevated due to softer tax buoyancy and front-loaded capital expenditure, the underlying fiscal position remains well managed. Strong non-tax revenues, disciplined revenue spending and a normalising capex trajectory have helped maintain the consolidation path. Importantly, this degree of fiscal control ahead of the Union Budget provides valuable policy flexibility. With borrowing requirements largely manageable and expenditure quality intact, the forthcoming Budget could focus on incremental growth support and medium-term reforms rather than corrective tightening. In that sense, we believe, the current fiscal situation retains the government’s room to focus on economic priorities in the Budget without compromising its commitment to fiscal consolidation.

Sources: CMIE, Kotak Institutional Equities, Avendus Spark and other publicly available information, BE: Budgeted Estimate, 8M: 8 months from April to November, FYTD: Up to Nov’25

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.