2025 Round-Up: Year Gone By Reiterates Asset Allocation is Key!

Last Updated On: 30 Dec 2025

5 min read

What’s the Point?

2025 was year of consolidation for Indian equities. Valuations have moderated across market cap segments, providing reasonable entry point for investors with a medium to long term view. DIIs continued to be net buyers for the 5th consecutive year in Indian equities, providing cushion against FII outflows and reinforcing the structural support for Indian equity markets. Fixed income saw steepening of the yield curve with extreme longer end of the curve edging higher. Precious metals continued their strong run in 2025. Brent crude was down for the third year in a row, which is positive for oil importing countries like India. Looking ahead to 2026, India’s economic growth is expected to be strong, however uncertainties will persist, hence, investors should focus on balanced portfolios via asset allocation.

Global Equities – AI led rally

Global equities delivered steady returns in CY 2025. AI-led themes outperformed, with KOSPI being the best performing global index. U.S. equities remained resilient, however ex-Mag7, it underperformed MSCI All Country World Index. Magnificent 7 posted a third consecutive year of outperformance, supported by AI-driven earnings growth, though returns were more measured than in previous 2 years.

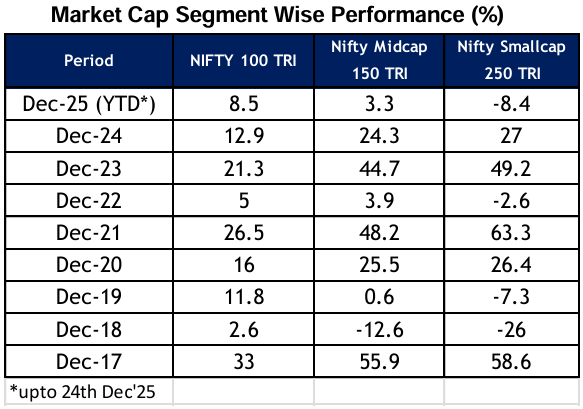

Indian Equities – Year of Consolidation

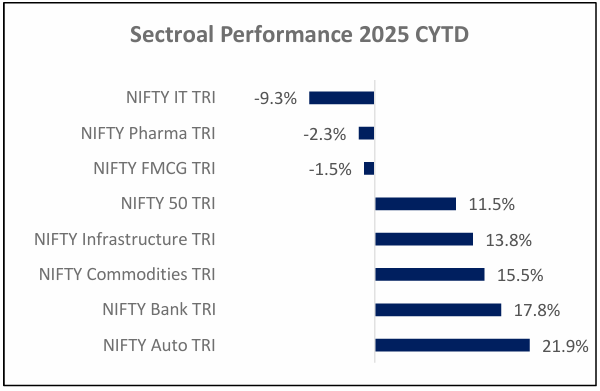

Indian equity markets (NIFTY 50 Index) delivered positive returns for the 10th consecutive year, a streak that has never been witnesses before. After 2 years of strong outperformance of mid and small cap indices, 2025 was the year for large caps. Large Caps outperformed small caps by the widest margin since 2019. There was a diverse performance in sectors as well. Consumer discretionary stocks outperformed driven by policy measures in the form of tax changes and GST cuts, while IT was the worst-performing sector due to its limited exposure to AI-driven growth.

On relative basis, India saw its worst relative underperformance vs MSCI Emerging Market Index in the last 30 years. Historically, such underperformance is followed by periods of outperformance. With markets going through a time correction over the past 15 months, valuations have now moderated, providing reasonable entry point for investors with a medium to long term view.

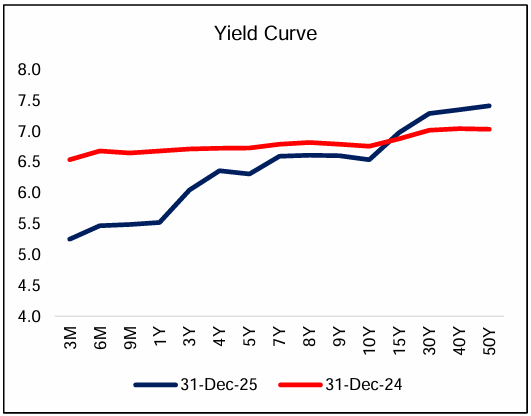

Fixed Income Markets – Yield Curve Steepens

Commodities - Safe Haven Assets continued to do well in 2025

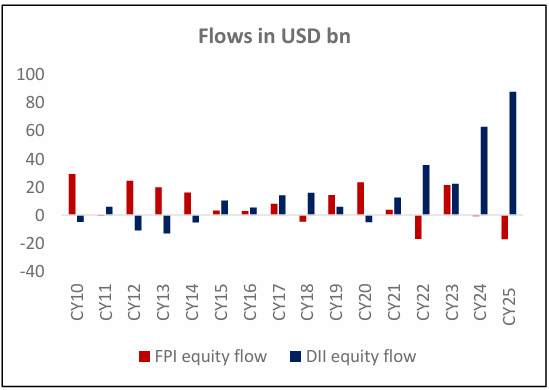

DII and FII Flows - DIIs Steady, FIIs Shaky

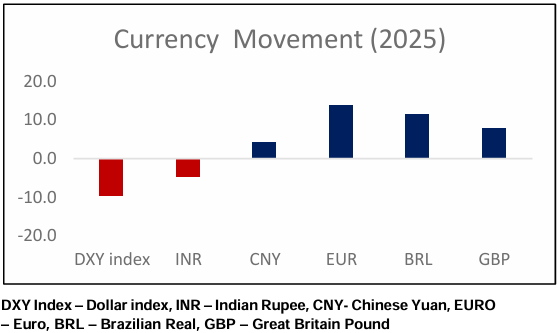

Currency – Dollar Drifts, INR Slips

Events to watch out for in 2026

- Progress on India–US Trade Deal and India-EU Free Trade Agreement

- AI spends and its Impact on economy and markets

- Will the US rate easing cycle continue?

- Impact of China’s overcapacity on other economies

- Union Budget 2026

- Will there be reversal of FPI flows into India?

- Impact of monetary & fiscal stimulus on consumption

- Private capex revival

Sources: Bloomberg, NIFTY Indices and other publicly available information.

About Tuesday’s Talking Points (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. If you have a topic that you would like to be featured here, please write to us at hello@hdfcfund.com

Disclaimer: Views expressed herein, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. Readers should seek professional advice before taking any investment related decisions.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.