Monetary Policy Review – June 2026

Last Updated On: 5 Jun 2026

5 min read

The Monetary Policy Committee (MPC) unanimously decided to keep the policy repo rate unchanged at 5.25% and retained the ‘neutral’ policy stance.

The Governor noted that Indian economy entered this episode of global turbulence with much better fundamentals than in previous similar episodes but emphasized that a prolonged conflict and resultant disruption in energy markets and supply chains pose risks to both inflation and growth prospects. Consequently, the RBI lowered its growth forecast and upgraded its inflation forecast for FY27 compared to the previous policy. The RBI also announced a series of measures to attract capital flows which should help ease pressure on the INR and reinforce external stability. These include:

- Expanding the universe for Government securities to include all new issuances of 15, 30 and 40 years maturity under the Fully Accessible Route (FAR). Additionally, FPI limits on short term investments under the general route have been removed. This, along with tax benefits on G-Secs provided by Government should help attract foreign capital.

- Increasing limits for investment by NRIs and OCIs in equity market without SEBI registration and extending it to all individual Persons Resident Outside India (PROIs) at par with NRIs and OCIs

- Allowing concessional forex swap till 30th September 2026 to incentivize External Commercial Borrowings by Public Sector Undertakings.

- Bearing the full hedging cost till 30th September 2026 for raising fresh 3–5-year FCNR (B) deposits by Authorized Dealers.

- Restoring the time for realization of export proceeds to nine months (from 15 months earlier).

The RBI indicated that going forward, duration and intensity of the conflict pose significant risks to RBI’s baseline projection of growth and inflation. Apart from the West Asia conflict, prospects of below normal monsoon also pose risks to inflation this year.

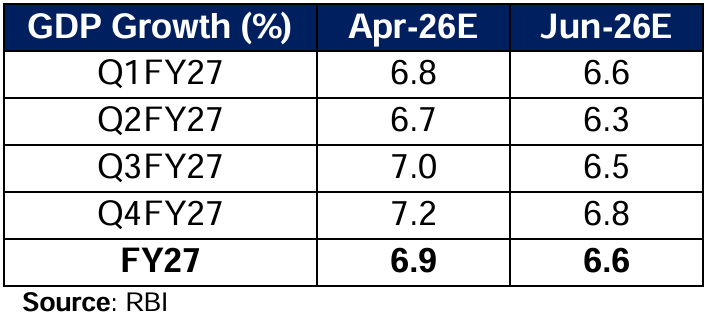

On Growth: The RBI noted that high frequency indicators for India suggests that growth has held up well since the start of the conflict with both private consumption and investment demand showing resilience. Furthermore, it highlighted that strong services momentum, continuing effect of GST rationalisation and stable employment conditions should support growth going forward. However, outlook on growth remains clouded due to elevated energy prices, supply chain disruptions and prospect of below normal monsoon which is likely to adversely affect agricultural activity and rural demand. Taking all this into consideration, GDP growth for FY27 has been revised down to 6.6% (from 6.9% in the previous policy) with downside risks.

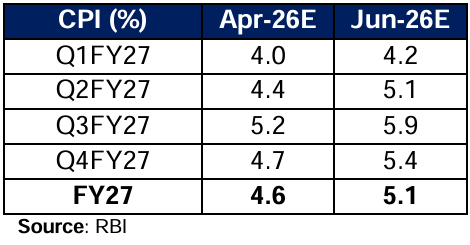

On Inflation: The RBI indicated recent uptick in headline inflation was muted and was driven largely by uptick in food inflation while core inflation remains benign. Moreover, it also stressed that core inflation excluding precious metals is much lower providing comfort. However, higher energy and several other input prices have started showing up in prices which was visible in recent WPI print. Going forward, retail inflation is expected to rise as there is partial pass through of energy prices to domestic pump prices, rise in input prices and expectation of lower-than-normal monsoon. Taking all this into consideration CPI inflation for FY27 was revised up to 5.1% (from 4.6% earlier). Core inflation (excluding food and fuel) for FY27 was also revised up to 4.7% (from 4.4% earlier).

Conclusion and Outlook

The fixed income market rallied across the curve. Going into the policy, a section in the markets expected that RBI might hike rates to defend the currency and RBI’s hold was a positive surprise. More importantly, RBI’s steps to attract capital flows should ease pressure on the currency and these measures should address multiple concerns in one go – improve capital flows, stabilize currency, shore up forex reserves, improve system liquidity, moderate credit to deposit ratio for banks, and result in money market and corporate bond yields drifting lower.

Going forward, while the uncertainty is likely to remain high due to West Asia Conflict, we believe outlook on Indian fixed income market has improved considerably due to:

- Measures to attract capital flows should help ease pressure on INR, improve liquidity and moderate credit to deposit ratio of banks.

- Risk of growth surprising to downside due to supply chain disruption along with expectation of inflation remaining within the tolerance band, reduce risk of significant rise in policy rates

- Liquidity is likely to be in surplus in the coming months in view of likely increased foreign flows due to steps taken by the RBI.

- Supply and demand dynamics for SLR is favourably placed in view of likely revival of demand from Banks (due to lower SLR holding) and Pension funds. Moreover, there is potential of OMOs purchases in H2FY27 depending upon how RBI intervenes in forex markets on receipt of capital flows under measures announced today.

Key risks to the favorable outlook

- Prolonged closure of Strait of Hormuz could lead to oil prices rising and could lead to worsening of CAD and BoP

- El Nino conditions in FY27 leading to large deficiency in southwest monsoon and reduced crop production and thus resulting in higher food prices

- Slight risk of fiscal slippage remains as geo-political disruptions can result in additional fertilizer and fuel subsidy and lower revenue due to reduction in excise duty. The possibility of expenditure rationalization and economic stabilization fund will likely cushion impact, to a large extent.

Looking ahead, despite heightened global uncertainty, in our view, the medium to term outlook for Indian fixed income remains optimistic, considering that the markets have priced in most of the negatives. Steps taken to attract foreign capital flows, ample systemic liquidity and balanced supply-demand dynamics for government securities provide meaningful support. With growth risks tilted modestly to the downside and inflation expected to remain within RBI’s tolerance band, the likelihood of aggressive rate hikes appears limited. In view of the elevated spread of money market instruments and corporate bond over G-Sec / repo rate, one may consider investment in short to medium duration (schemes with duration of up to 5 years) categories, especially corporate bonds focussed funds in line with individual risk appetite. Key risks to monitor include any elongation in conflict or adverse food price movement due to weak monsoon.

DISCLAIMER

The views of HDFC Asset Management Company Limited, Investment Manager for HDFC Mutual Fund expressed herein as of June 05, 2026 are based on internal data, publicly available information and other sources believed to be reliable. The source for this document is the Bi-monthly Monetary Policy Statement, 2026-27, dated June 05, 2026 published by the RBI. Any calculations made are approximations, meant as guidelines only, which you must confirm before relying on them. The information contained in this document is for general purposes only and is not investment advice. The document is given in summary form and does not purport to be complete. The document does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. The information/ data herein alone are not sufficient and should not be used for the development or implementation of an investment strategy. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Past performance may or may not be sustained in future. HDFC Mutual Fund/HDFC AMC is not guaranteeing/ offering/communicating any indicative yields or guaranteed returns on investments made in the scheme(s). Neither HDFC AMC and HDFC Mutual Fund (the Fund) nor any person connected with them, accept any liability arising from the use of this document. The recipient(s) before acting on any information herein should make his/her/their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.