Market Review- January 2025

Last Updated On: 4 Apr 2025

5 min read

Macroeconomic Update

Macroeconomic Update Equity Market Update

Equity Market Update Debt Market Update

Debt Market Update

Macroeconomic Update

Divergent growth trend was witnessed across different regions of the world with economic activity in US remaining resilient while that in EU and China subdued. Wages in US continue to rise as labor markets remain resilient on account of strong non-farm job creation and consumer spending remaining upbeat. However, US house construction pace is moderating while credit card delinquencies suggest stress amongst consumers has also started to rise. While Eurozone reported better than expected growth in business activities, manufacturing sector continues to contract. On the other hand, trade uncertainties led to moderation in Chinese manufacturing activities as export orders declined while staffing levels fell at the quickest in last 5 years. The new adminstraion in the White House has led to rise in global uncertainties and his economic policies will be a key monitorable going forward.

Inflation has moved within a narrow range and largely on expected lines across most major economies. Consequently, most major central banks continue to remain in easing mode. However, the US Fed decided to take a pause in the last policy meeting as it waits to see the impact of new administrations' policies on growth and inflation.

Consumption boost at the core of Union Budget FY26: The Union Budget for FY26 was presented against the backdrop of slowing economic growth and rising demand for tax relief, particularly from the middle class, in view of decelerating urban consumption. In this context, the budget seems to successfully balance the imperative of providing relief to taxpayers while maintaining fiscal discipline. The Government will forgo revenue of INR 1 lakh crore due to income tax relief which will aid higher growth through a multiplier effect. While capital expenditure is budgeted to grow at 10.1% YoY in FY26, allocation to core infrastructure segment like roads and railways have remained flat compared to last year. Despite forgone revenue due to income tax relief, the Government stuck to fiscal consolidation path and has targeted a fiscal deficit of 4.4% of GDP in FY26 (vs 4.8% of GDP in FY25RE).

The Government also announced that beyond FY26, the choice of fiscal anchor will be debt-to-GDP and the Government will set fiscal deficit each year such that the overall debt-to-GDP is on a declining path. This is in line with global best practices and will give Government flexibility to implement counter-cyclical fiscal policies.

Source: CMIE, Budget documents, RE – Revised estimates, BE – Budgeted Estimates

Overall, we believe, the FY26 budget strikes a pragmatic balance between immediate economic support and long-term fiscal sustainability, positioning India on a steady path toward growth and resilience.

Indian economic activity mixed: The high frequency indicators point at conflicting trends. While auto registrations witnessed an overall improvement in Jan'25, the rural demand indicators such as 2W and tractor registrations remain subdued. Manufacturing PMI was recorded at 6 month high in Jan'25 on the back of strong sales growth and positive demand outlook. However, services PMI softened compared to last month as new businesses rose at a slower pace.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, www.vaahan.parivahan.gov.in, www.posoco.in ^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. * based on CMIE survey

India's economic indicators in January point towards a mixed picture. Going forward, urban demand is likely to get a boost from income tax relief from a medium-term perspective while rural demand too is likely to rebound on the back of strong kharif output. However, global uncertainties due to restrictive trade policies may dampen sentiment and could affect India's growth too.

Central government finances in a comfortable position: While the fiscal deficit has been low, recent month data indicates that government is stepping up capex and may sustain it for rest of the FY25. The Government has targeted a lower fiscal deficit for FY25 at 4.8% of GDP (vs 4.9% of GDP initially) and is likely to meet that target.

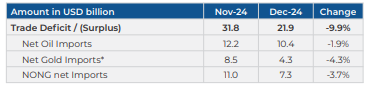

Trade deficit narrows, likely to remain rangebound: Trade deficit in Dec'24 narrowed to 3 month low driven by a combination of low imports and higher exports. Fall in imports was primarily due to Oil & gold imports while India's petroleum, agricultural & engineering sector led the sequential rise in exports.

Source: CMIE

The trade deficit is likely to remain rangebound as exports will fare better than exports. . Further, healthy growth in services exports is likely to keep current account within manageable range. However, restrictive trade policies and a risk of trade war will decide future course of India's trade dynamics in the medium term.

Retail inflation moderates in Dec, will ease further going forward India's CPI eased further in December 2024 on back of cooling food prices especially that of pulses and vegetables. However, price growth in vegetables, cereals and edible oil continue to remain elevated. Core CPI also moderated marginally driven by fall in 'personal care and effects' segment.

Source: CMIE, Ministry of Commerce; *Net Gold includes gold, silver and pearls precious & semiprecious stones adjusted for gems and jewellery exports. ^NONG refers to Non-Oil Non-Gold (as defined above) imports/exports

CPI inflation is likely to ease further on back of falling food prices given new arrival of kharif crops and benign core inflation momentum. However, any inflationary effect of recent INR depreciation and difficult global trade environment will have to be monitored closely.

Source: CMIE; @-CPI excluding food, fuel, transportation & housing

Commodity prices: Brent crude prices surged during the first fortnight of January but has eased since then. Steel prices moderated further due to over-supply caused by lack of demand and Chinese overcapacity. Gold prices continue to rise amidst global uncertainties.

Source: Bloomberg; *Market prices as on January 31, 2025. ^M-o-M change. & - Change in FYTD25

Summary and Conclusion:

As noted earlier, divergent growth trend across economies persists with US growth holding up quite well while that of EU and China remains subdued. While growth in US is expected to remain strong going forward, new administration's policy on trade and immigration will have bearing on growth inflation dynamics for not just US but for all major economies and needs to be monitored closely.

India's growth momentum improved sequentially driven by urban consumption which was also evident in robust GST collections growth in Jan'25. Going forward even if growth in FY25 is expected to slow down compared to FY24, it still will be better than most global peers. Private consumption is also likely to get a boost going forward due to income tax relief announced by the Government. Further, private corporate sector capital expenditure has potential to accelerate in view of low leverage, increasing capacity utilization, consistent corporate profitability, and a robust banking sector balance sheet. India's external sector also remains robust on the back of comfortable current account deficit and adequate forex reserves. Rise in geopolitical tensions and a possibility of a trade war in are key near-term risks.

Looking ahead, the medium-term outlook for India's economy seems optimistic, in our view. This optimism is driven by policy continuity, benefits from Production-Linked Incentive schemes, opportunities arising from shift in the global supply chain, enhanced infrastructure investments, the potential of resurgence in private sector capex, and the likely boost to private consumption due to income tax relief to the middle class.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.