Starting Your Retirement Planning in your 40s? It is never too late!

Last Updated On: 15 May 2026

Many people postpone retirement planning when they are young. In your 20s and 30s, it feels natural to focus on enjoying your newly earned income through purchases and experiences. By the time you reach your 40s, the reality hits: retirement could be just 15 to 20 years away.

The good news is that this timeline still gives you enough opportunity to build a meaningful retirement fund. You have likely completed major household expenses and established yourself in your career by the time you reach your 40s. This puts you in a better position to consider larger amounts regularly now. With discipline and the right strategy, starting in your 40s can lead to a comfortable retirement.

In this article, you will learn how you can start retirement planning in your 40s and get answers to the most common doubts that might be in your mind regarding the same.

Why Your 40s Are Crucial for Retirement Planning

Your 40s represent a turning point in your financial life. Unlike your younger years when you had decades ahead, time is now your limiting factor. With 15 to 20 years until retirement, you can still benefit from the power of compounding.

Consider this example: You had invested 50,000 monthly through a systematic investment plan in the HDFC Retirement Savings Fund for 20 years, the fund has given 19.95% return since its inception. After investing for 20 years your investments grew to 12.30 crores. If you can dedicate a larger portion of your income to retirement savings, then your final corpus can be much higher. A combination of time, income, and potential returns makes your 40s the right moment to act seriously about your retirement.

Assessing Your Current Financial Situation

Before you can plan for retirement, you need to understand where you stand financially today. To understand your current financial situation, you need to take these four steps:

Create a Detailed Budget: Track all your monthly income and expenses. This will show you exactly where your money is going and help you identify unnecessary spending that can be redirected to your retirement savings.

Review Your Debts: Make a list of all outstanding loans and credit card balances. Focus on paying these down, especially high-interest ones, as they drain your income and hinder your ability to save.

Assess Your Current Savings: Tally up any retirement funds, mutual funds, or other investments you already have. This gives you a clear baseline and helps you set realistic goals for the future.

Evaluate Your Income: Look at your current salary, job stability, and potential for growth. Consider if you can increase your earnings through a promotion, a better job, or even a side income.

A clear picture of your current financial health forms the foundation for effective retirement planning.

Setting Realistic Retirement Goals

Once you understand your current situation, define what retirement looks like for you. To set realistic retirement goals, follow these key steps:

Define Your Retirement Vision: Start by imagining what you want your retirement to look like. Consider your desired lifestyle, potential healthcare needs, travel plans, and any personal hobbies or goals you want to pursue.

Estimate Your Future Expenses: Calculate how much you'll likely spend each month in retirement. A good starting point is your current expenses, but be sure to account for inflation, which reduces the purchasing power of money over time. A realistic estimate is to assume an annual inflation rate of 6% to 7%.

Set a Target Retirement Corpus: Based on your estimated monthly expenses and an assumed lifespan in retirement (e.g., 25 years), calculate the total amount of money you'll need. This is your retirement corpus goal.

Make Your Goal Specific and Reviewable: Your goal should be a clear, achievable number based on your income. Write it down and review it annually to adjust for any changes in your life or financial situation. This keeps you motivated and on track.

Clear goals provide direction and motivation for your retirement planning journey.

Strategies to Accelerate Retirement Savings

Starting in your 40s means you need to catch up on retirement savings aggressively. Here are key strategies to maximise your retirement corpus.

Increase Your Savings Rate: Go through your budget to find non-essential (discretionary) spending you can cut. Immediately redirect that money into your retirement investments.

Use Tax-Efficient Investments: Choose investment options that help you save on tax. Retirement-focused mutual funds are a great example. You can claim deductions up to ₹1,50,000 per year under Section 80C of the Income Tax Act under the old regime with eligible schemes.

Invest According to Your Risk Profile: Select investments that match your comfort level with risk. For a 40-year-old, a balanced portfolio that mixes equities (for growth) and debt (for stability) is often suitable. As you get closer to retirement, you can consider gradually moving your money into safer, more conservative options.

Maintain Investment Discipline: The best way to stay consistent is through a Systematic Investment Plan (SIP), which automates your investments. Crucially, avoid withdrawing money from your retirement fund before you actually retire.

Overcoming Common Retirement Planning Challenges

Here are the common obstacles you might face when planning for retirement in your 40s and how to overcome them:

Guilt of Starting Late: Many feel they should have started earlier. The solution is to ignore past regrets and focus on the productive saving years you have ahead of you.

Uncertainty About the Target Amount: It's hard to know exactly how much you'll need. To solve this, use online retirement calculators and seek professional financial advice to set a clear, realistic savings goal.

Balancing Present Needs vs. Future Security: You might feel torn between enjoying life now and saving for later. The key is to create a realistic budget that allocates specific funds for both your current lifestyle and your future retirement.

Market Uncertainty: Stock market fluctuations can be stressful. Remember that with a 15-20 year timeframe, markets have historically recovered from downturns. Manage this risk through diversification and maintaining a long-term perspective.

Fear of Making Decisions: The fear of making a wrong financial move can be paralysing. Overcome this by educating yourself on basic investment principles and seeking professional guidance to make informed choices.

Seeking Professional Financial Advice

Retirement planning involves multiple variables and personal circumstances that benefit from professional guidance. A qualified financial adviser can help you assess your situation objectively and create a personalised plan.

They can recommend appropriate investment products based on your risk tolerance, income, and goals.

They also monitor your portfolio performance and make adjustments as needed to keep you on track. When selecting an adviser, look for qualifications, experience with retirement planning, and a transparent fee structure. Professional advice is a smart approach to achieving your retirement goals.

How HDFC Mutual Fund/AMC Can Help You?

HDFC AMC offers a diverse range of investment schemes designed to help you systematically build wealth for retirement and other long-term goals. Here’s how we can assist you:

Diverse Options: You can choose from a wide variety of mutual funds that match your personal risk tolerance and investment timeline, from equity funds for growth to debt funds for stability.

Professional Management: Your money is handled by experienced fund managers who make informed investment decisions, saving you the effort of tracking the market daily.

Disciplined Investing: You can use tools like a Systematic Investment Plan (SIP) to invest a fixed amount regularly, which helps build discipline and average out your purchase cost over time.

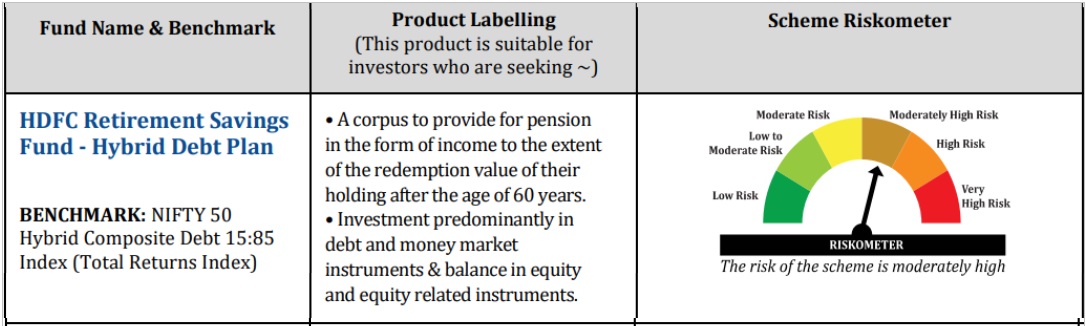

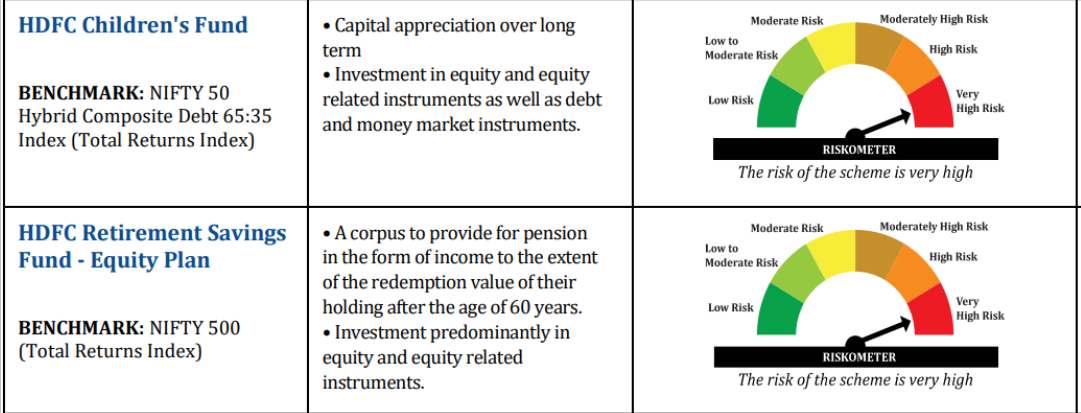

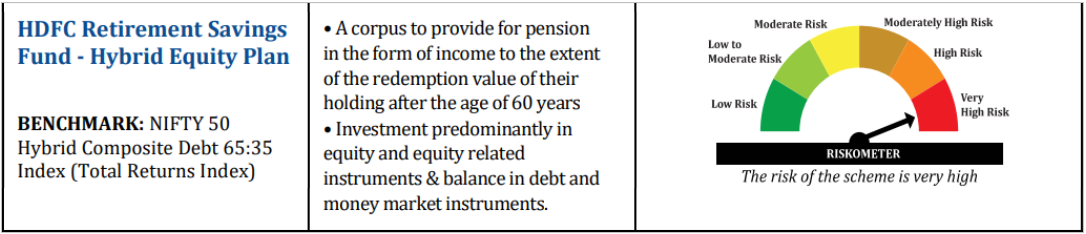

Below are some of the schemes that you can use to achieve your retirement goals

~ Investors should consult their financial advisers, if in doubt about whether the product is suitable for them

Riskometer is as on December 31, 2025

For latest riskometer, investors may refer to the Monthly Portfolios disclosed on the website of the fund viz. www.hdfcfund.com

Conclusion: Taking Action Now and aim for a Secured Future

Your 40s are not too late to start retirement planning. You have sufficient time, hopefully increasing income, and the ability to make significant progress. Success requires three things: understanding your financial situation, setting clear goals, and taking consistent action. Start now, stay committed, and you can build a retirement that provides comfort and peace of mind.

(Note: Mutual fund investments are subject to market risks, read all scheme related documents carefully. The information given here is for general purposes only. Past performance may or may not be sustained in the future. HDFC Mutual Fund/AMC does not guarantee any returns on investments made in the Scheme. The current investment strategies are subject to change depending on market conditions. The views/information provided do not have regard to specific investment objectives, financial situation, or the particular needs of any specific person who may receive this information. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. Investors should be aware that the fiscal rules/tax laws may change, and there can be no guarantee that the current tax position will continue indefinitely. In view of the individual nature of tax consequences, each investor should seek appropriate advice.)

FAQs

1. Is it too late to start saving for retirement in my 40s?

No. With 15-20 years left and typically a higher income, you can still aim to build a substantial retirement fund. The key is to start immediately and be disciplined.

2. How much should I have saved for retirement by age 40?

It depends entirely on your lifestyle and goals. A general rule of thumb is to have saved an amount equal to your annual salary, but a personalised calculation is always best.

3. What are the best investment options for someone in their 40s?

A balanced approach is usually ideal. Consider a mix of equity (for growth) and debt funds (for stability) through diversified mutual funds. Your choice should match your personal risk tolerance.

4. How can I catch up on retirement savings if I'm behind?

Increase your savings rate by cutting unnecessary expenses, using tax-efficient investment plans, and consider getting professional advice to create an aggressive but realistic strategy.

5. Should I work with a financial adviser for retirement planning?

Yes, it's highly recommended. An adviser provides a personalised strategy based on your specific goals, helps you navigate complex decisions, and keeps your plan on track.

Stay ahead with our insights

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.