Tuesday's Talking Points

Q1FY26 - Earnings Review - Modest but Resilient

What’s the Point?

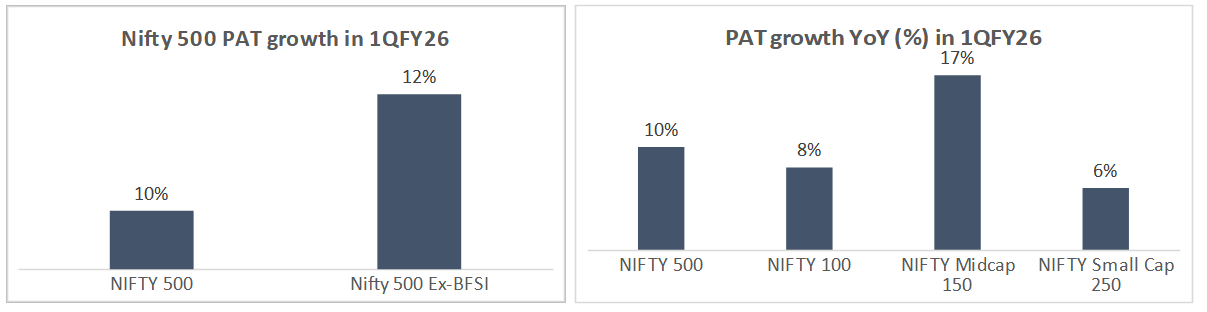

- NIFTY 500 companies saw a modest growth of 10%(YoY) in Q1FY26; much better than the last financial year.

- Within NIFTY 500, midcap companies continue to grow at faster pace, beating large caps and small caps. Earnings for NIFTY Midcap 150 index grew at 17% in the June quarter.

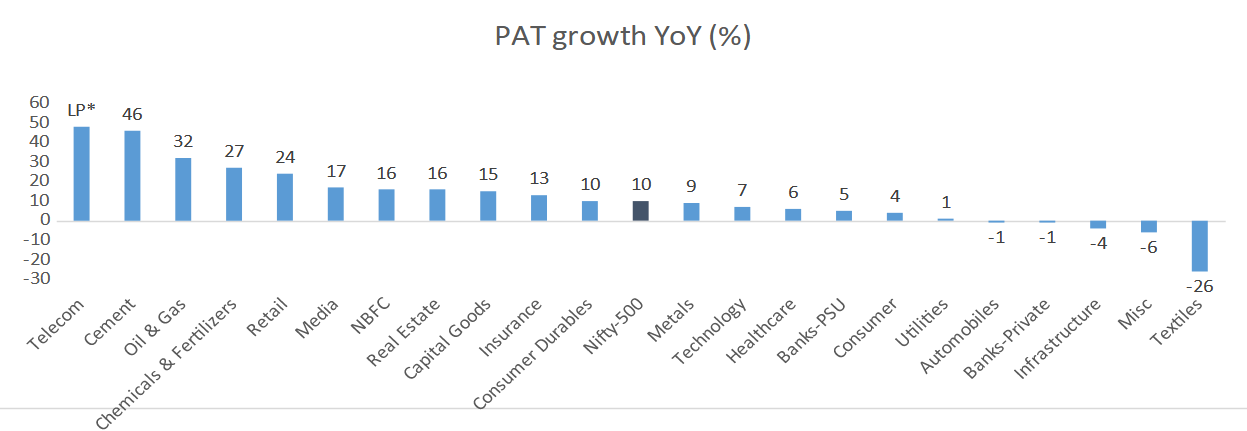

- Q1 earnings growth was broad based with 16 sectors (out of 21) reporting profit growth and 42% of the NIFTY 500 companies growing above 15%.

- Improved liquidity, rate cuts, higher government spending, lower GST and benign commodity prices create a supportive backdrop for earnings outlook for the second half of the financial year.

Nifty 500 companies delivered a healthy performance in 1QFY26 despite significant geopolitical headwinds and weak consumption trends, improving from a muted performance during FY25.

Midcaps continued to deliver robust earnings

In Q1 FY26, the Nifty 500 companies reported a year-on-year (YoY) earnings growth of 10%. Excluding the BFSI sector, earnings growth improved to 12% YoY.

The quarter’s earnings performance was driven primarily by the midcap segment. The Nifty Midcap 150 Index delivered a robust 17% YoY growth in aggregate earnings, outperforming both large caps and small caps for the fourth consecutive quarter. In comparison, the Nifty 100 and Nifty Small cap 250 Indices recorded earnings growth of 8% and 6% YoY, respectively. While large-cap earnings (Nifty 100 Index) rose 8% YoY, there has been a notable improvement on sequential and YoY basis (flat growth in Q1FY25 and 5% in Q4FY25).

Sectoral Earnings - Broad-based

Q1 earnings growth was broad-based, with notable contributions from key sectors such as Oil & Gas (+32% YoY), Metals (+9% YoY), NBFCs (+16% YoY), Capital Goods (+15% YoY), Cement (+46% YoY), Telecom (from loss to profit), Retail (+24% YoY), and Real Estate (+16% YoY).

Out of 21 key sectors, 16 reported year-on-year profit growth in Q1. Additionally, around 42% of Nifty 500 companies (212 out of 500) reported Profit after Tax (PAT) growth of over 15% YoY during the quarter.

* LP – Loss to Profit

Telecom - sector reported a profit of INR12b in 1QFY26 compared to a loss of INR5b in 1QFY25.

Cement - sector saw a strong rebound after a weak year, with earnings up 46% YoY. Sales rose 14% and EBITDA jumped 39%, reflecting better demand and improved pricing.

Oil and Gas - sector contributed significantly during the quarter, with PAT growth of 32% YoY, mainly led by OMCs.

Metals - sector contributed positively to the quarter’s earnings, with PAT growth of 9% YoY over a soft base of 1QFY25. Growth was also boosted by a strong performance of ferrous companies, driven by a healthy operating performance.

BFSI - The banking sector posted a muted 1Q performance with business momentum moderating. Net interest margins (NIMs) contracted for both private and public banks. Contrarily, NBFCs posted healthy earnings growth of 16% YoY, driving the overall earnings growth in 1Q.

Capital Goods - companies reported a healthy quarter with PAT growth of 15%YoY, led by healthy order momentum and execution.

Healthcare - sector reported a muted quarter with only 6% YoY earnings growth. While sales growth was stable for the domestic formulation segment, US sales performance was muted. Hospital companies within Nifty-500 reported robust earnings growth of 30% YoY.

Technology - IT services companies reported a challenging quarter, with PAT growth of 7% YoY. Tier-1 companies remained weak due to lower-than-expected growth and subdued demand.

Automobile - Auto sector earnings declined 1% YoY amid weak demand. However, policy support like tax cuts, better liquidity, and lower interest rates may boost future growth.

Consumer - sector reported a sequentially stable quarter, with volume growth across most companies limited to low- to mid-single digits. Rural demand continues to outpace urban demand, though encouraging trends are also emerging in urban markets.

Margin Expansion

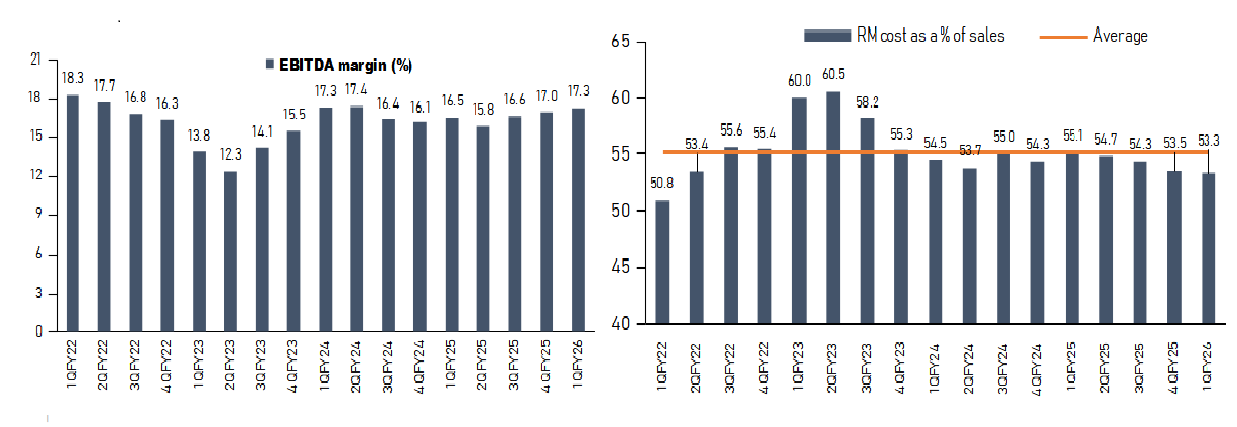

Another takeaway from the Q1 earnings was margin expansion. Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margin for NIFTY 500 companies expanded by 75 bps YoY and 30 bps QoQ in 1QFY26. A key driver for margin expansion was decline in raw material cost. Raw material cost as a % of sales reduced from 55.1% in Q1FY25 to 53.3% in Q1FY26. Lower oil prices and benign commodity prices aided in lower raw material cost for corporates.

Conclusion

While earnings growth in the June quarter has been modest, several positive factors—such as improved liquidity, the impact of interest rate cuts, increased government spending, lower GST rates, and favourable commodity prices—provide a supportive environment for earnings in the second half of the financial year. Given that the markets have gone through a time correction over the past year due to various factors, and with the outlook improving for the second half of the year, this could be an opportune time for investors with a medium- to long-term horizon to consider increasing their allocation to equities.

Sources: MOSL, KIE, and other publicly available information

About Tuesday’s Talking Points (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.