Domestic flows counter FPI woes and tariff blows!!

Last Updated On: 20 Aug 2025

5 min read

- DIIs Take the Lead: DIIs now own almost 20% of the Nifty 500 (more than FPIs), with holdings rising for five straight quarters. Strong SIP inflows, having tripled in five years, provide stable, long-term capital that cushions markets against short-term volatility.

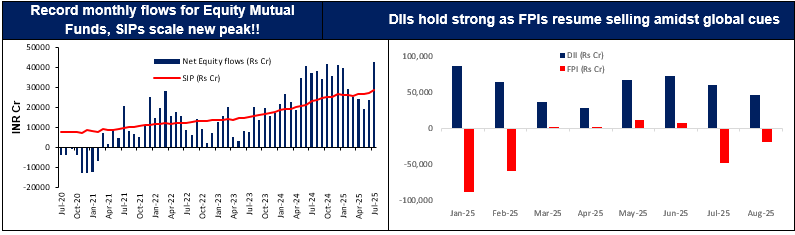

- Foreign Outflows triggered by Global Cues: Tariff uncertainties, expensive valuations, and rupee depreciation have prompted FPIs to pare exposure (Net Outflows of ~70,000Cr in July & Aug’25). Trade tensions have weighed on near-term sentiment but not on long-term fundamentals.

- First Sovereign Rating upgrade in 18 years: Underscores policy stability, fiscal prudence, and growth prospects. These fundamentals make India a core investment destination despite temporary global headwinds.

Recently Equity mutual funds registered their highest-ever monthly inflows of ₹42,702 crore, with monthly SIP contributions rising to a new record of ₹28,464 crore. While, Mutual Funds have been registering strong flows for some time now, the latest surge comes against the backdrop of sharp sell-off by Foreign Portfolio Investors (FPIs) amidst tariff uncertainty. Interestingly, the recent sell-off by FPIs comes after a quarter(Q2CY25) of positive net flows.

Domestic Investors continue to anchor Indian equities

DII holdings in NIFTY 500 surpassed FPIs for the first time in Mar’25. This trend has continued in Q2CY25 as DII ownership in Nifty-500 rose 170bps YoY to 19.4%, whereas FPI ownership was 18.8%. This was the fifth consecutive quarter where DIIs raised their stake, with promoters and FPIs reducing their ownership. Within the Nifty-500, FPIs reduced their holdings in 53% of the companies YoY, while DIIs increased their stake in 74% of the companies. Worth noting that DII holding has almost doubled from 11.4% in Jun’15 to 19.4% in Jun’25.

Strong DII flows are being driven largely by steady, disciplined investments into equity mutual funds through SIPs. These monthly contributions provide a predictable stream of money into the market, regardless of short-term volatility. SIP book has grown more than 3 times over the last 5 years indicating growing popularity of SIPs.

In spite of this, Mutual Fund penetration is still relatively low in India. Globally, households shift from physical assets to financial assets with a rise in per capita income. While India is still lagging its peers, we are seeing a structural shift to financial assets aided by gradual increase in disposable income and improved access to financial services. In view of this, DII flows could have ample support from the financialization of savings in the years to come.

Global cues trigger FPI Outflows

Uncertainty around imposition of tariffs and their implications on emerging economies has led to outflows from Emerging Markets. Escalating US-India trade tensions have triggered a sharp sell-off in India equities over the past few weeks as foreign investors reassess exposure to India.

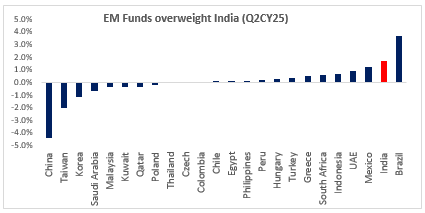

Within the EM space, India trades at a premium to peers. While width (varied businesses) and depth (number of sizeable companies), along with strong economic growth prospects help India justify a premium over other EMs, relatively expensive valuations has also been a factor for reallocation of capital by FPIs.

Further, depreciation of Rupee against the dollar erodes USD-denominated returns for FPIs, adding another disincentive to hold Indian assets during global risk-off phases.

Indian Equities vs other Emerging Markets

As of June-end, India was the second largest active weight for EM Funds, in spite of a sharp increase in Benchmark weight (18.1% in Jun’25 vs 8.8% in Jun’17).

While subsequent uncertainty around tariffs has impacted the short-run attractiveness of ‘Destination India’, structural tailwinds and economic growth faster than peers means that India will continue to remain a key destination within EM for foreign investors.

First Sovereign Rating upgrade in 18 years – A Vote of Confidence for India

Amid all other developments, credit rating agency S&P upgraded India’s Sovereign Credit Rating from BBB- to BBB on the eve of India’s 79th Independence Day. While the immediate impact on yields may be limited, what’s important is that the upgrade reflects Government’s commitment to fiscal consolidation, policy stability, improved quality of public spending, strong external balance sheets, sound inflation management and sustained economic growth.

At a broader level, this vote of confidence by a global credit rating agency couldn’t have come at a better time, against the backdrop of geopolitical headwinds. This could certainly boost confidence of foreign investors (FDIs and FPIs alike) in ‘Destination India’, the benefits of which could be more pronounced once trade tantrums dissipate in future.

Key Takeaway: The record surge in Equity Mutual Fund inflows and SIP contributions highlights the growing power of India’s domestic investors, who are counter-balancing foreign outflows during uncertain times. With DIIs now owning more of the Nifty 500 than FPIs, markets are better anchored by steady, long-term flows. While trade tensions may influence foreign investors in the short run, India’s growth story, driven by democracy, demographics, and digitization remains strong. Counter-balancing stability of domestic investors adds another positive dimension for investors looking to invest in India. As ‘Smart Money’ of FPIs goes slow on Indian equities, domestic investors can continue doing the ‘smarter’ thing by focusing on consistent, long-term investing without reacting to short-term market moves.

^Sources: Kotak Institutional Equities, Motilal Oswal, UBS and other publicly available information

DII: Domestic Institutional Investors, FPI: Foreign Portfolio Investment, EM: Emerging Markets

About Tuesday’s Talking Point (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.