Market Review - June 2025

Last Updated On: 18 Aug 2025

Macroeconomic Update

Macroeconomic Update Equity Market Update

Equity Market Update Debt Market Update

Debt Market Update

Macroeconomic Update

The month of June saw geo-political tensions flare up as conflict between Israel and Iran escalated, drawing in US as well. However, a ceasefire was reached after 12 days without disrupting the crucial trade routes which was a relief. In US, retail sales fell more than expected led by decline in auto sales as rush to beat tariff related price hike subsided and consumer confidence deteriorated as well. On the positive front, the labour markets in the US remain solid with decent wage growth and declining unemployment rate. Eurozone's manufacturing PMI in June was recorded at its highest level since August 2022 though it still remains in contraction zone. China's manufacturing PMI returned to expansion zone, but new export orders continue to contract due to tariff related uncertainty.

Inflation moved within a narrow range and largely on expected lines across most major economies. The Fed kept policy rates unchanged in its meeting in June and projected that growth could be lower while inflation higher due to tariffs. As inflation returned to target, the ECB cut interest rate by 25bps but signalled a pause thereafter. Bank of England, on the other hand kept the interest rate unchanged but signalled possibility of a cut in near future.

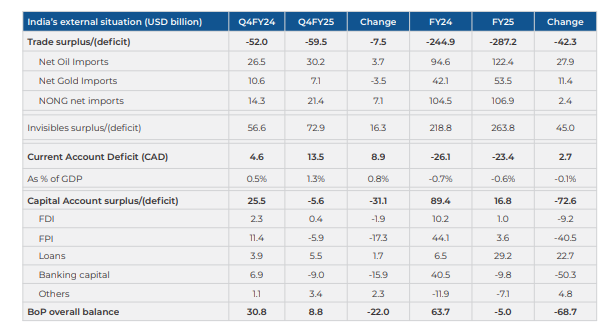

Q4FY25 Current Account recorded a surplus: India's Current Account recorded a surplus of 1.3% of GDP in Q4FY25 led by higher invisibles surplus driven by non-software services and higher remittances. On an annual basis, the Current Account Deficit (CAD) was recorded at 0.6% of GDP. This was second year in a row when CAD was under 1% of GDP. On the other hand, India's capital account in Q4FY25 recorded a deficit for second quarter in a row led by lower net FDI and higher portfolio outflows from equities. On an annual basis, capital account surplus at 0.4% of GDP was at a multiyear low.

Source:- CMIE

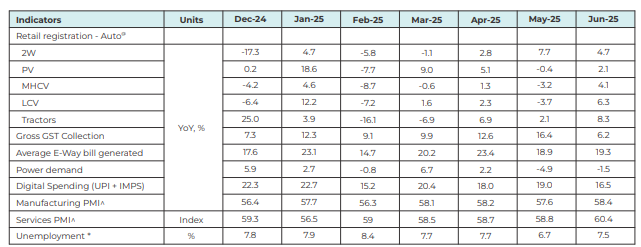

Indian economic activity mixed in June: While the pace of 2W registrations moderated in June, that of PVs and CVs picked up. The uptick in economic activities was also visible in the in the PMI readings. While manufacturing PMI hit 14 month high in June on higher export orders, services PMI was recorded at 10 months high led by international sales. However, power demand remains in contraction mode and GST collections moderated compared to last month.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, www.vaahan.parivahan.gov.in, www.posoco.in ^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. * based on CMIE survey

Going forward, urban demand is likely to get a boost from income tax relief and easing monetary conditions while rural demand too is likely to remain steady on back of strong rabi output and prospects of above normal monsoon. However, global trade uncertainties may dampen sentiment and could weigh on India's growth.

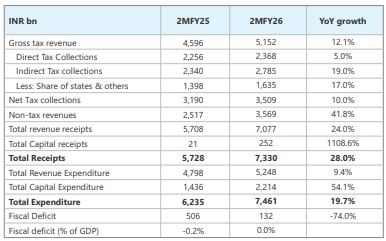

Government finance in comfortable position aided by RBI dividend: Gross tax revenue has grown at a healthy pace in the first two months led by indirect tax collections even as direct tax collection growth has been sluggish. The Government has maintained pace of capex growth since March well into this financial year. Despite higher expenditure, higher than budgeted RBI dividend helped contain fiscal deficit in the first two months.

Source: CMIE

Trade deficit narrowed in May: Merchandise trade deficit fell in May'25 compared to the previous month led by decline in net oil imports. The non-oil non-gold (NONG) imports were largely stable compared to the previous month.

Source: CMIE, Ministry of Commerce; *Net Gold includes gold, silver and pearls precious & semiprecious stones adjusted for gems and jewellery exports. ^NONG refers to Non-Oil Non-Gold (as defined above) imports/exports

The trade deficit is likely to remain range-bound going forward. Further, healthy growth in services exports is likely to keep current account within manageable range. Trade deal negotiations with US will remain a key monitorable in the coming months.

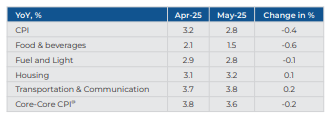

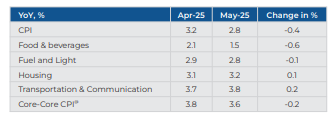

Retail inflation moderates further in May, likely to remain benign: India's CPI inflation in May was recorded at its lowest level since Mar'19 driven by further moderation in food prices. Core-Core (which excludes food, fuel, petrol, diesel, gold, silver and housing) also declined by 20bps to 3.6% suggesting benign momentum in core prices.

Source: CMIE; @-CPI excluding food, fuel, petrol, diesel, gold, silver and housing

CPI inflation is likely to remain below 4% in the coming months due to favourable outlook on food inflation and favourable base effect.

Commodity prices: Flare up in geopolitical tensions in the middle east during the month led to rise in crude oil and other commodity prices in fear of disruption of trade routes. The prices cooled off subsequently as the conflict ended. Prices of industrial metals like copper and aluminium rose during the month.

Source: Bloomberg; *Market prices as on May 31, 2025. ^Y-o-Y change. & - Change in FY26YTD

Summary and Conclusion:

Global growth prospects today face unprecedented uncertainty due to US' tariff policy and risk of geopolitical flare up. US growth is exhibiting early signs of cooling off but is still resilient especially its labour market. However, this is likely to deteriorate going forward as effects of tariffs and uncertainty weigh on prospects. Domestic demand in China remains subdued and deflationary forces have gathered steam. The global growth prospects hinges on the outcome of US trade policy and in this regard trade negotiations with different countries remain a key monitorable going forward.

India's growth momentum is exhibiting resilience. The high frequency indicators for June suggests that the growth momentum from last year has sustained in this fiscal as well. Going forward even if growth in FY26 is expected to remain at similar levels as compared to FY25, it will still be better than most global peers. Urban consumption is likely to get a boost going forward due to income tax relief announced by the Government and monetary easing by the RBI. Rural consumption too is likely to remain steady on the back of bumper rabi harvest, prospects of above normal monsoon, falling inflation and higher real rural wage growth. India's external sector also remains comfortable on the back of low current account deficit (due to better-than-expected services export) and adequate forex reserves. Rise in geopolitical tensions and a tariff related uncertainty are key near-term risks.

Looking ahead, the medium-term outlook for India's economy seems optimistic, in our view. This optimism is driven by opportunities arising from shift in the global supply chain, bi-lateral trade deal with various countries, enhanced infrastructure investments, the potential of resurgence in private sector capex, and the likely boost to private consumption.

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.

Recommended Posts

Market Review - February 2026

Market Review - January 2026

Market Review - December 2025