Market Review - December 2024

Last Updated On: 27 Jan 2025

Macroeconomic Update

Macroeconomic Update Equity Market Update

Equity Market Update Debt Market Update

Debt Market Update

Macroeconomic Update

The global economy remained resilient in 2024 primarily driven by robust growth in the US. The strength of the U.S. economy was supported by high government fiscal deficit, a thriving services sector, a strong labor market, high real wages, and solid household finances. However, the manufacturing and real estate sectors lagged. In contrast, Europe, including the UK, faced softer growth due to the ongoing war, elevated energy prices, and widespread slowdown in manufacturing and services. Among emerging markets (EMs), China underperformed, with lowerthan-expected economic stimulus and a weakening real estate sector. Industrial activity also remained weak as domestic demand and exports declined, though growth was supported by steady investments in infrastructure and manufacturing.

Inflation in most advanced economies (AEs) fell significantly from its 2023 peak, driven by corrections in food, energy, and commodity prices. While core inflation trended downward, it remained relatively high, and progress toward central bank targets was slower than anticipated. China’s inflation also remained subdued during the entire year.

Major central banks began easing monetary policies as risks to growth and inflation became more balanced. The U.S. Federal Reserve and the European Central Bank (ECB) each cut policy rates by 100 basis points in quick succession, while the Bank of England reduced rates by 50 basis points. Although monetary policy is expected to remain accommodative, the pace of rate cuts could slow and become more data-driven in 2025. The notable exception was the Bank of Japan, where robust growth and inflation suggest a higher likelihood of rate hikes in the coming year.

India’s growth momentum softens as government spending moderates sharply: India’s GDP growth in the first nine months of CY24 slowed down, driven by multiple cyclical factors. A sharp deceleration in government spending was a key contributor, as elections delayed public expenditure. On the private sector front, corporate investments remained subdued while the real estate sector demonstrated resilience, supported by sustained demand for housing. Consumption showed signs of recovery, particularly in rural areas, benefiting from a low base. Urban demand moderated, reflecting the impact of the RBI’s macroprudential tightening and consumption fatigue stemming from a high base in previous years. On the external front, growth in exports outpaced imports, primarily due to robust performance in services exports.

On the Gross Value Added (GVA) side, agricultural output slowed in the first half but improved sequentially. Manufacturing growth witnessed a sharp plunge, as demand slowdown, constrained pricing power, and elevated input costs eroded profitability. Construction activity also moderated due to delays in government capex. The services sector, too, experienced a deceleration as weakness in urban demand weighed on segments such as retail, hospitality, and financial services.

Source: CMIE, MoSPI, Ambit Capital research. Note – PADO: Public Administration, Defence & Other Services

Looking ahead, the overall growth outlook could remain contingent on a revival in government capex and sustained rural recovery. There are reasons to be optimistic over the rural sector in view of robust growth expected in Kharif crops, progress in rabi crops and improvement in wages. However, a revival in government capex and targeted policy measures to incentivize private investment as well as consumption will be crucial for reinvigorating growth.

Economic activity shows rural and urban divergence: India's high-frequency indicators present a mixed picture, reflecting divergent trends across sectors. On the positive side, rural indicators such as two-wheeler and tractor sales are performing well, signalling a steady recovery in the rural economy. Additionally, manufacturing and services PMIs remain healthy, although they have eased from their recent peaks, and power demand has picked up, indicating resilience in economic activity. The CMIE unemployment survey suggests rangebound unemployment, providing indicating stability to the labour market.

However, several weak spots persist. GST collections have decelerated and PV sales weakened, reflecting softer consumption. Railway goods movement remains subdued, and commercial vehicle (CV) sales continue to contract year-on-year, pointing to subdued industrial activity.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, https://vahan.parivahan.gov.in, https://posoco.in ^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. &- Sum of UPI+IMPS spending

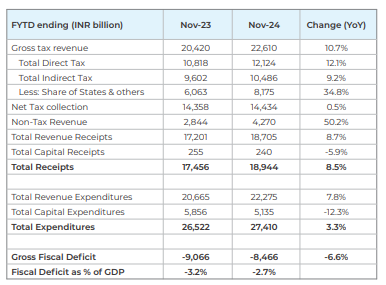

Government finances in a comfortable position: On a fiscal yearto-date (FYTD) basis, the deficit remains lower year-on-year, supported by robust personal tax collections and a substantial dividend from the RBI. Corporate tax collections grew modestly at ~1%, reflecting subdued corporate profit growth, while indirect tax collections, particularly GST, performed relatively better. On the expenditure side, both revenue and capex spending has picked up in recent months, but capital expenditure (capex) remains relatively weak and is down YoY. While the capex spending is expected to accelerate in rest of the year, it may still fall short of budgeted estimates.

Source: CMIE

While the fiscal deficit has been low, recent monthly data indicates that the government is stepping up spending and it may sustain for rest of the FY25. However, in view of the high ask rate of capex spending for the rest of the year and buoyant personal tax collections, deficit might undershoot the FY25 budgeted estimates (4.9% of GDP).

Retail inflation cools down but remains elevated: Consumer Price Index (CPI) witnessed a moderation in average inflation across most categories in the first 11 months of CY24 compared to CY23, with CPI easing from 5.7% to 4.9%, driven largely by declines in non-food components. Fuel and light inflation saw the steepest drop, from 4.1% in CY23 to -2.9% in 11MCY24, reflecting lower energy costs and cut in LPG prices. Housing inflation also moderated significantly, declining by 1.6 percentage points, while transportation and communication inflation eased marginally. Core CPI dropped sharply from 5.9% to 4.0%, signaling a broadbased reduction in underlying inflationary pressures. However, food inflation bucked the trend, driven by broad based rise in prices in key categories including vegetables, cereals and pulses.

Source: CMIE; @-CPI excluding food, fuel, transportation & housing

In recent months, vegetable prices have remained elevated, with seasonal price corrections occurring gradually. However, the anticipated arrival of new crop supplies is expected to ease food inflation. Combined with the subdued momentum in core CPI, this is likely to bring overall CPI closer to the RBI’s target of 4% in 2025.

Current account deficit narrows significantly, likely to remain in manageable range: India’s current account remained in a comfortable position during the first nine months of 2024 (9MCY24). The increase in gold and silver prices, along with reduction in import duties and weak jewellery exports, led to a sharp rise in net gold imports. Additionally, the net oil deficit widened due to a decline in oil exports, partially offset by lower oil prices. The non-oil, non-gold (NONG) trade deficit narrowed slightly, supported by strong exports of electronics, automobiles, machinery, and chemicals, though this was largely counterbalanced by higher imports of electronic components and engineering goods. The overall increase in the merchandise trade deficit was more than offset by a sustained rise in services exports, driven by higher IT services exports, a growing number of global capability centres, and robust remittances from non-resident Indians (NRIs).

Source: CMIE, Ministry of Commerce; NM – Not meaningful. ^ Net Gold includes gold, silver and pearls precious & semiprecious stones adjusted for gems and jewellery exports. NONG refers to Non-Oil Non Gold (as defined above) imports/exports

Capital flows remained strong, driven by an increase in foreign portfolio investment (FPI) inflows, both in debt (boosted by inclusion in the JP Morgan Emerging Market Bond Index) and equity. Furthermore, NRI deposits and external borrowings saw a sharp rise. However, foreign direct investment (FDI) flows were weak, as a record number of IPOs in 2024 led many foreign investors and promoters to withdraw their funds from India.

Overall, the balance of payments remained healthy, with a manageable current account deficit (CAD) and strong foreign exchange reserves. Looking ahead, the current account is expected to remain within manageable levels, supported by the resilience of services exports and a stable merchandise trade deficit. The capital account is likely to stabilize, with potential improvements in FDI flows.

Source: Bloomberg; *Market prices as on December 31, 2024

Commodity prices mixed trend: 2024 witnessed a strong performance in precious metals, subdued energy prices, and mixed momentum in industrial commodities. Brent crude prices declined modestly, indicating softer global energy demand. Gold emerged as a standout performer with significant gains, driven by safe-haven demand and economic uncertainties, surging 27.2% in CY24 after a strong 13.1% increase in CY23. Industrial metals showed mixed performance—while copper, zinc and aluminium posted moderate gains in CY24, steel and lead prices experienced steep declines.

Summary and Conclusion:

In 2024, global economic growth moderated but still surpassed expectations, primarily driven by the United States. However, China’s growth fell short of expectations, hindered by structural issues in its real estate sector. While inflation retreated from its peak, it remained stickier than anticipated, and central banks globally reduced policy rates in response to easing inflation and moderating growth. Despite this, it appears that the first phase of monetary easing has concluded, with central banks now likely to adopt a more data-dependent approach going forward. The outlook for 2025 has become increasingly uncertain, with factors such as changes in the U.S. government, rising policy uncertainty, and unclear inflation trajectories contributing to the unpredictability. However, fundamental growth drivers remain resilient, and growth is expected to remain relatively steady.

In India, growth momentum remained robust in the first half of 2024, buoyed by strong economic activity. However, the pace slowed sequentially due to a reduction in government spending and subdued corporate profitability. On the positive side, a pick-up in consumption and household real estate activity helped offset some of the negative impact. The external sector remained resilient, supported by robust growth in services exports, remittances, and foreign portfolio investment (FPI) inflows, along with healthy foreign exchange reserves. Persistent inflation, mainly driven by rising food prices, kept the Reserve Bank of India (RBI) on hold throughout the year, although it reduced the cash reserve ratio (CRR) to ease liquidity and revised its policy stance to neutral.

Looking ahead, India's economic growth is expected to stabilize, supported by a recovery in consumption, increased government spending, and continued strength in household real estate activity. However, several risks could affect the outlook, including the escalation of geopolitical tensions, a resurgence in inflation, potential policy changes that could negatively impact global trade, a return to tightening measures by major central banks, and a sharp rise in energy prices.

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.

Recommended Posts

Market Review - February 2026

Market Review - January 2026

Market Review - December 2025