Market Review

The month of August continued to witness evolving trade dynamics where the US maintained its assertive stance, implementing a new wave of tariffs effective August 7. While trade deals with the EU, Japan, and Indonesia were finalized, tariff-related uncertainty remained elevated with India being subject to much higher tariffs than other countries. Although US GDP growth for Q2 was revised upwards according to second revised estimates, underlying momentum has weakened as frontloaded exports unwound, and domestic demand softened. Labour data in US surprised on the downside raising hope for a rate cut in September. In China manufacturing PMI remained in contraction mode for fifth consecutive month as export orders continued to fall. New orders for businesses in the Eurozone increased for the first time since May-2024 helping business activity expand at its quickest pace in 15 months.

Inflation remained within a narrow range and largely on expected lines across most major economies. However, the impact of tariff pass through was visible in US inflation data. While the Fed is widely expected to cut rates in September following weaker than expected jobs report, ECB is expected to hold rates.

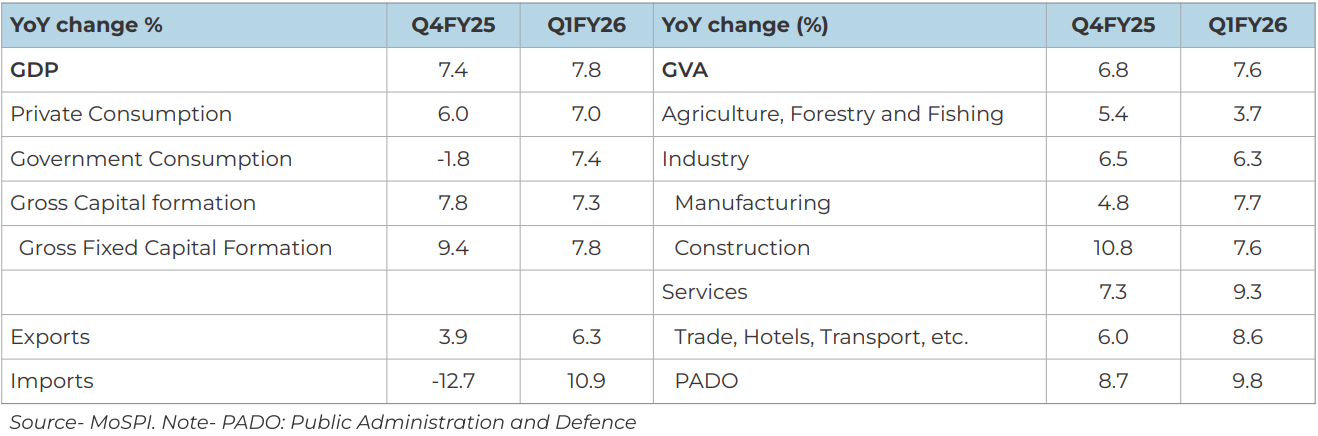

Q1FY26 GDP growth higher than expected: Q1FY26 GDP came in at 7.8% YoY which was higher than consensus expectation of 6.7% and RBI's estimate of 6.5%. On the supply side, the growth was driven by robust services and manufacturing sector activity. While growth in services sector was at a 9-quarter high, manufacturing sector clocked its best growth rate in last 5 quarters. On the demand side, growth was driven by overall consumption growth with Government consumption demand growing at 7.4% YoY in Q1 as against contraction in Q4FY25. Nominal GDP growth however decelerated to 8.8% YoY in Q1FY26 (as against 10.8% YoY in Q4FY25).

Going forward, growth is likely to face headwinds due to higher tariffs imposed by US on Indian imports. However, monetary stimulus and tax cuts (both personal income tax and GST cuts) are likely to cushion the impact on growth.

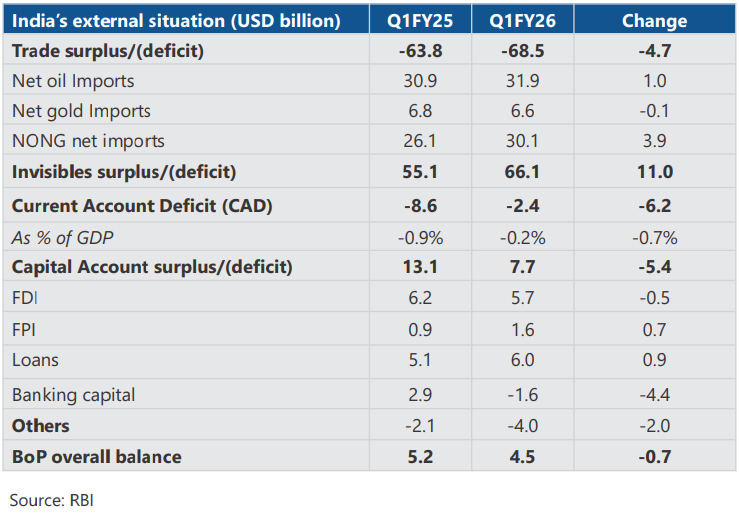

Current account deficit (CAD) remains benign: Q1FY26 CAD was recorded at 0.2% of GDP compared to a surplus of 1.3% of GDP in Q4FY25 as trade deficit in Q1 widened compared to Q4FY25. However, the CAD was lower when compared to Q1FY25. On the other hand, Capital account surplus declined from a year ago period but was higher than Q4FY25 on account of higher foreign investments (both FDI and FPI).

Going forward, current account is likely to face headwinds from higher tariff imposition by US on Indian imports but is likely to remain within manageable levels due to higher services exports and remittances.

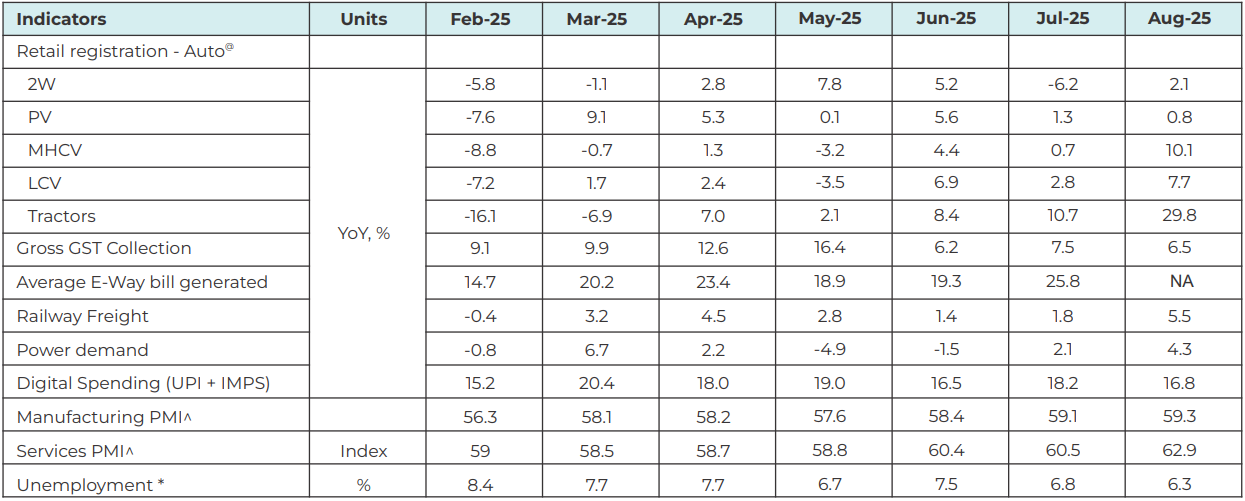

High frequency indicators suggest uptick in economic activity in Aug: Pace of vehicle registrations except PVs witnessed improvement in August with tractors registrations growth touching multi-year high. Moreover, both manufacturing and services PMI showed robust business activity in the month of August and power demand showed improvement for second month in a row. However, gross GST collections moderated, and growth has been sub-par for third month in a row.

Source: www.gstn.org.in, www.icegate.gov.in, CMIE, PIB, RBI, www.vaahan.parivahan.gov.in, www.posoco.in ^Number >50 reflects expansions and number <50 reflects contraction compared to previous month. @ - figures are preliminary data and are subject to revision. * based on CMIE survey

Going forward, urban demand is likely to get a boost from income and proposed GST tax relief and easing monetary conditions while rural demand too is likely to remain steady on back of strong rabi output and prospects of above normal monsoon. However, global trade uncertainties and higher US tariff on Indian imports are likely to hurt growth in the near term.

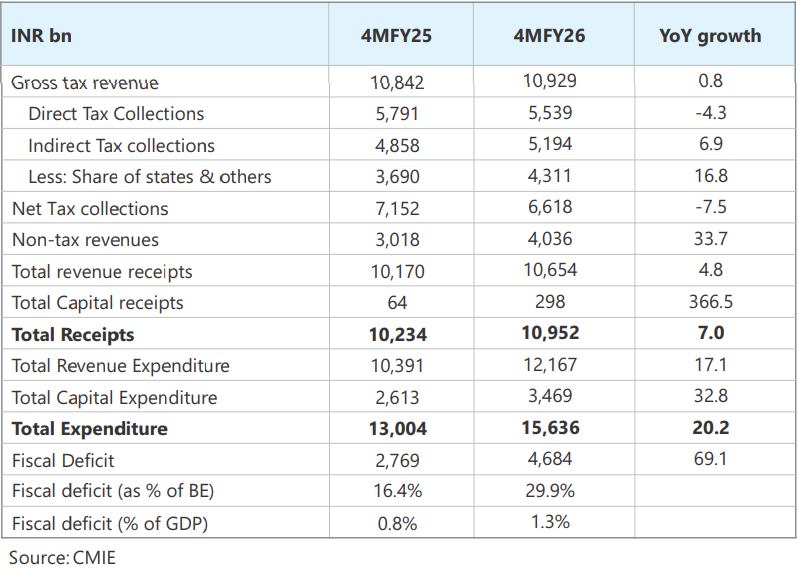

Income tax collections under pressure: Gross tax revenue growth in the first four months of this fiscal has been sluggish driven by poor growth in direct tax collections as personal income tax growth has contracted 10% YoY even as corporate tax growth has been decent. Total expenditure growth in first 4 months of this fiscal has been strong as Government front loaded expenditure in the first quarter. Consequently, fiscal deficit has widened in the first 4 months when compared to the same period last year.

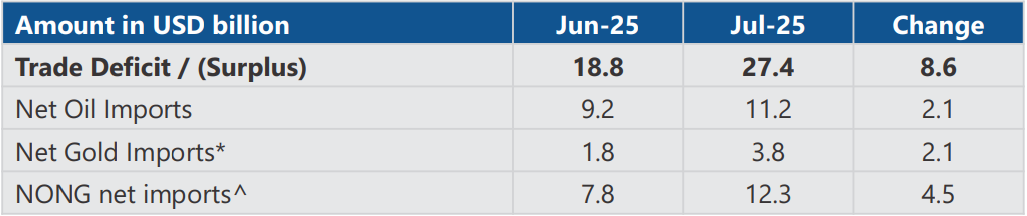

Trade deficit widened in July: Merchandise trade widened in Jul'25 compared to the previous month led mainly by widening of non-oil, non-gold (NONG). Net oil and net gold imports defict too were higher compared to the previous month.

Source: CMIE, Ministry of Commerce; *Net Gold includes gold, silver and pearls precious & semiprecious stones adjusted for gems and jewellery exports. ^NONG refers to Non-Oil NonGold (as defined above) imports/exports

The trade deficit is likely to face headwinds due to higher tariff imposition. However, healthy growth in services exports is likely to keep current account within manageable range.

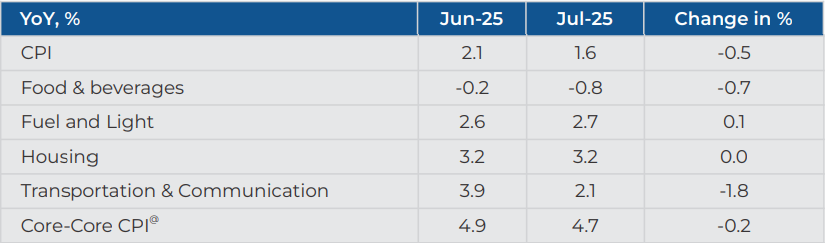

Retail inflation in Jul lowest since Jul-2017: India's CPI inflation in July was recorded at its lowest level since Jul'17 driven by further moderation in food prices and favourable base. Core-Core (which excludes food, fuel, petrol, diesel, gold, silver and housing) also declined by 20bps.

Source: CMIE; @-CPI excluding food, fuel, petrol, diesel, gold, silver and housing

CPI inflation is likely to remain below 4% in the coming months due to favourable outlook on food inflation and favourable base effect.

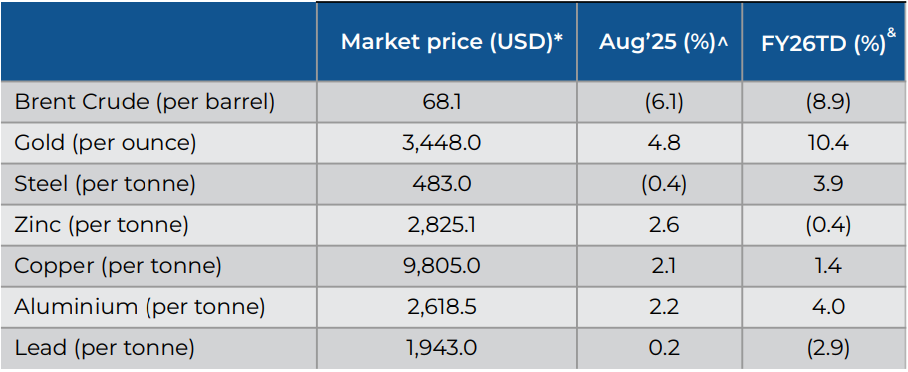

Commodity prices: Oil prices decreased during the month following OPEC announcement to increase oil supply. Industrial metals such as steel, aluminium, and copper witnessed a modest recovery in Aug '25 as Chinese restrictions on production have reduced supply.

Source: Bloomberg; *Market prices as on Aug 31, 2025. ^Y-o-Y change. & - Change in FY26YTD

Summary and Conclusion:

Global growth prospects today face unprecedented uncertainty due to US' tariff policy. US growth is exhibiting early signs of slowdown with softness in labour market now visible in data. This is likely to deteriorate going forward as effects of tariffs and uncertainty weigh on prospects. Domestic demand in China remains subdued and deflationary forces have gathered steam. Global growth prospects will depend on how imposition of higher tariffs by US plays out in the medium term.

India's growth momentum is exhibiting signs of resilience as evident from strong Q1 GDP data and recent high frequency indicators. However, as India faces one of the highest tariffs by US on its imports, growth is likely to take a hit in the second half of this fiscal. The Government has realised this and has embarked on major reform overhaul for the country starting with lowering of GST rates to boost consumption. Going forward urban consumption is likely to get a boost due to income tax relief and GST rate cuts announced by the Government and monetary easing by the RBI. Rural consumption too is likely to remain steady on the back of prospects of above normal monsoon, falling inflation and higher real rural wage growth. India's external sector also remains comfortable on the back of low current account deficit and adequate forex reserves. Rise in geopolitical tensions and a tariff related uncertainty are key near-term risks

Looking ahead, the medium-term outlook for India's economy seems optimistic, in our view. This optimism is driven by bi-lateral trade deals with various countries, Governments renewed efforts for structural reforms, enhanced infrastructure investments, and the likely boost to private consumption.