Monetary Easing and other signals pointing to potential Growth in Banking

Last Updated On: 23 Apr 2025

5 min read

What’s the Point?

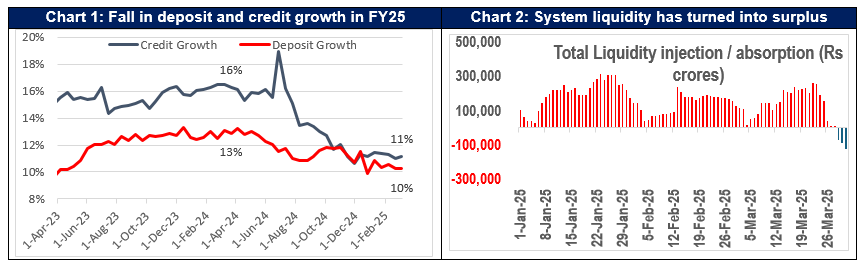

Banking sector growth in FY25 was weak, with credit growth for March 2025 being ~11% YoY vs ~16% as of March 2024. Factors such as slower economic growth, liquidity tightness, slower lending on account of risk weight increases and rising delinquencies led to lower growth. However, changes in the macro environment and regulatory actions suggest that deposit and credit growth could be well placed in the medium term. New norms issued by the RBI on Priority Sector Lending, Liquidity Coverage Ratio could ease operational cash flows for banks. Change in Liquidity guidance, liquidity measures of Rs8.8 Lakh crores and the accommodative monetary policy stance could provide a near term boost to the money creation cycle, thereby giving a boost to growth. With the banking sector reducing its cost of deposits, margins could be relatively less impacted from falling rates. Structural growth drivers for banking remain intact, viz. robust economic growth, rising penetration, use of technology & digitisation, proactive regulations that act as risk interventions, strong bank balance sheets and low NPAs. Valuations for the sector are below historical averages, and could be considered an investment opportunity.

Numbers in Perspective

Source: Investec, RBI

What are the factors pointing aiding credit growth in the medium term?

1. Boost to liquidity: Average net liquidity deficit increased to ~Rs 70,000 crore in FY25, from ~Rs 55,000 crore in FY24 on account of various factors such as increased forex interventions to stabilise the Rupee. The deficit had widened to ~Rs2.8 lakh crore in January 2025 but improved thereafter, and today stands in surplus liquidity. RBI further announced OMO purchases (Open Market Operations) worth INR 800bn to be conducted in four tranches of INR 200bn each in April. Measures to improve liquidity include durable actions such as the CRR Cut, OMO purchases, Fx Swaps for 3 years, along with short term measures such as the 6 month forex swaps and term repo auctions. The total quantum of these liquidity measures stand at Rs8.8 Lakh crores.

2. Potential change in forex policy reduces scope of liquidity squeeze from forex operations: There has been a marked shift in RBI’s forex operations in the recent months. While RBI has had a strong presence in forex markets to stabilise the rupee in forex markets, RBI commentary now indicates that forex interventions going forward could be lower.

3. Changes in other regulations could also improve growth: RBI has made changes in the Priority sector lending norms (PSL), that allow home loans of upto Rs 50 Lakhs in its PSL book, up from Rs25 Lakhs. Changes in the Liquidity Coverage Ratio (LCR) norms announced by the RBI this week also improve the current LCR of banks as per an RBI impact analysis, freeing up some capital for deployment as loans.

What are the key risks to higher growth?

Key risks to the sanguine outlook for banking sector growth includes the Second order impact of global macro environment, with uncertainty on the business outlook having the potential to reduce demand for credit growth. This is partially offset by the positive outlook for domestic consumption, which could continue to raise demand for growth in infrastructure and manufacturing investments. While increased delinquencies in the unsecured lending space could also hurt growth, their overall share in the lending books is low at 7%, and delinquency rates are showing signs of having peaked around September 2024 across personal loans, credit cards and consumer loans.

At what cost? (Margins)

Lower rates present the risk of lower margins for banks, as a large portion of banking sector loans today are based on external benchmark rates. Therefore, the 50bps cut in repo rate by RBI in 2025 have led to lower gross lending rates. However, banks have been able to raise funds on the deposit side at lower costs across products, including savings accounts. This showcases the strength in the ability to raise deposits even at lower rates. Margins have therefore stayed robust so far. Risks emanate from further rate cuts, and one will need to monitor for significant reduction in banks’ ability to reduce their deposits costs in line with rate cuts.

Structural drivers for growth remain strong

Structural growth drivers for banking remain intact, viz.

1. Robust economic growth, with India’s real GDP growth projected to grow at >6% for the next few years

2. Rising penetration, with increase in access to credit by Retail products, such as personal loans

3. Use of technology & digitisation, such as use of online banking and mobile apps, digital payments infrastructure, smarter underwriting using digital tools, all leading to faster and sustainable growth

4. Proactive regulations that act as risk interventions, such as increasing risk weights on unsecured lending that were introduced in November 2023, improve the risk perception for banks, as the regulator ensures risks are monitored and better accounted for.

5. Strong bank balance sheets: According to the latest Financial Stability Report, Bank Balance Sheets remain well capitalised, with average capital adequacy standing at 17%, significantly higher than the regulatory minimum. In fact, results of macro stress tests remain satisfactory even under adverse stress scenarios.

6. Low NPAs: Net NPAs for the banking system stood at 0.6% in September 2024, compared to ~6% in FY18. Improved NPA outlook reduces the credit cost that banks need to account for, and aid growth.

Conclusion - Banking system is well placed and could be an investment opportunity

India’s Banking Sector has a long history of operations in India. It has strong foundations for growth in terms of fundamentals, regulatory environment and economic growth. Strong structural drivers, positive medium term growth drivers, and a comfortable valuation position makes the sector potentially investible. Investors looking to invest in India’s banking and financial sector companies could consider investing in the HDFC Banking and Financial Services Fund, which was launched in December 2021. The Fund provides an opportunity to benefit from robust GDP growth, rising penetration, the sector’s recovery after a decade of challenges, and a favourable portfolio positioning aligned with macro trends. It aims to invest in companies that are leaders or gaining market shares through superior execution, scalability, adoption of technology, etc., and seeks to achieve diversification and management of risks by investing across sub-segments of financial services sector.

Sources: Investec, RBI, Bloomberg, and other publicly available information

About Tuesday’s Talking Points (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Product Labelling and Riskometer of HDFC Banking & Financial Services Fund

|

HDFC Banking & Financial Services Fund (An open ended equity scheme investing in Banking and Financial Services Sector) is suitable for investors who are seeking*: |

Scheme Riskometer#

|

|

*Investors should consult their financial advisers, if in doubt about whether the product is suitable for them. #For latest riskometer, investors may refer to the Monthly Portfolios disclosed on the website of the Fund viz. www.hdfcfund.com

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.