India’s Economic Growth – Powered by Structural Drivers, Shielded by Resilience

Last Updated On: 4 Jun 2025

5 min read

What’s the Point?

- India’s Q4FY25 Real GDP growth stood at 7.4% – higher than the Bloomberg Consensus Estimate of 6.8% and higher than the Q3FY25 estimate of 6.2%. This placed the provisional estimates of Real GDP growth for the full fiscal year at 6.5%, which is in line with the estimates provided in February 2025 by MoSPI. In addition to this positive development, Gross Value Added (GVA = GDP – Net Taxes on Products) for Q4FY25 stood at 6.8% – slightly higher than the Bloomberg Consensus Estimate of 6.4%.

- While growth in Private Final Consumption Expenditure – a component that accounts for over 58% of India’s GDP – has been muted, India’s structural growth drivers remain intact, led by demographic dividend, growth in investments, robust services exports, improving manufacturing potential, and increasing digital adoption. Such strong drivers of economic growth, supporting sustained structural growth, could bode well for corporate profitability going into FY26.

Numbers in Perspective

Source: Ministry of Statistics and Program Implementation (MoSPI), International Monetary Fund (IMF World Economic Outlook – April 2025); *PFCE: Private Final Consumption Expenditure, **GFCE: Government Final Consumption Expenditure, $Gross Fixed Capital Formation; India’s data: FY-basis and 2025 data as updated by MoSPI in May 2025, Other countries’ data: CY-basis

What has led to the pick-up in India’s GVA in FY2025?

1) Supply Side

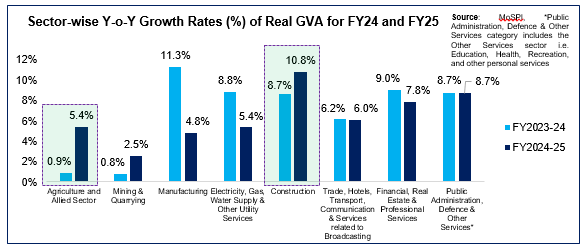

a. Agriculture and Allied Sector: During the past few quarters, rural economy has outperformed the urban sector due to an improvement in rural wages, faster growth in tractor sales, farm exports and fertilizers contributed to an acceleration in rural economy. While analysts are questioning the longevity of this strong growth, an expectation of an above-normal level of rainfall could act as a tailwind for this sector a boost.

b. Industrial Sector: This sector saw a strong sequential pickup (6.8% Y-o-Y in Q4FY25 versus 5.1% Y-o-Y in Q3FY25), mainly driven by a sharp rise in construction (10.8% Y-o-Y in Q4FY25 versus 7.9% Y-o-Y in Q3FY25). As per the RBI Bulletin published in May 2025, this rise has happened on account of double digit Y-o-Y growth rates in steel consumption and cement production for 3 consecutive months – January to March 2025.

2) Demand Side

a. Gross Fixed Capital Formation: This rise was noted mainly due to an increase in capex initiatives. As per data published by CGA in March 2025, the Provisional Estimates of capex for FY25 (FY25PE) stood at 103.3% (₹10.18 lakh crore) versus the 99.9% for the same period last year. There was strong pickup – 29.6% M-o-M – in capital expenditure between February and March 2025. The Government, which has budgeted capital expenditure of ₹11.21 lakh crore in the Union Budget FY2025-26, has already witnessed a 61% Y-o-Y increase in capex to ₹1.59 lakh crore in April 2025 vs April 2024.

b. Decline in Imports: Q4FY25 saw a 12.7% Y-o-Y decline in imports due to a decline in import of crude oil, which accounts for ~20% of India’s import bill for FY25. This decline is being attributed to the softening in Brent Crude Oil Prices. From its peak level of US$87.4 per barrel touched on July 07, 2024, prices have cooled by 15% as on March 31, 2025, with prices additionally cooling by 14% between March 31, 2025 and June 02, 2025.

Looking Forward…

The global macroeconomic outlook for FY26 has been uncertain as a result of the US trade policy. While fears have abated due to a 90-day pause put by the US Government, the lack of clarity on their subsequent steps deepen the uncertainty. Amidst this environment, a key risk that remains is risks to global growth and trade, but India’s relatively low exposure to trade, along with high potential to grow share in global trade allows some comfort on that risk.

On the domestic front, the Reserve Bank of India – encouraged by the lower inflation print – has conducted a 50 bps cut in Cash Reserve Ratio from 4.5% to 4% and 2 Repo Rate cuts of 25 bps each from 6.5% to 6% in its last 3 Monetary Policy Reviews. It has carried out multiple Open Market Operations and USD/INR swaps to supply higher liquidity into the system. All these measures have been taken to boost consumption from the demand side, and push higher manufacturing and infrastructural growth from the supply side. This has especially been made possible due to India’s comfortable fiscal deficit position (robust revenue growth, high RBI dividend) allowing space for the private sector to invest and grow. With India set to emerge as the 4th largest economy in 2025 and being the fastest growing major economy, its macroeconomic resilience and positive fundamentals support a strong long-term investment case.

Sources: Bloomberg, CMIE, MoSPI, IMF, RBI, and other publicly available information

About Tuesday’s Talking Points (TTP): TTP is an effort by HDFC AMC to guide key conversations in the Indian financial markets and investing ecosystem. We aspire to do this by providing relevant facts, along with our perspective on the issue at hand. Please provide your feedback at this link: https://forms.office.com/r/Cr8JNjMGWk

Disclaimer: Views expressed herein are based on information available in publicly accessible media, involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. The information herein is for general purposes only. Stocks/Sectors/Views referred are illustrative and should not be construed as an investment advice or a research report or a recommendation by HDFC Mutual Fund (“the Fund”) / HDFC Asset Management Company Limited (HDFC AMC) to buy or sell the stock or any other security. The Fund/ HDFC AMC is not indicating or guaranteeing returns on any investments. Past performance may or may not be sustained in the future and is not a guarantee of any future returns. The recipient(s), before taking any decision, should make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Did you find this interesting?

Your opinion matters - share your thoughts and help us improve.